The recent fun and games involving the NBA and the gambling indictments are certainly amusing on their own merits, but do they say something else?

Perhaps it’s a recognition that many humans have a viscerally innate attraction to large flows of money—and the easier it appears, the deeper its lure. Along the route to the personal bank, a lot of what most people would consider normalized fail-safes tend to drop by the wayside over time.

Now, insert the words “investing world” into these paragraphs. So we will boldly say—after having said it for four years—we are here. The massive dollars flowing into private assets, much of which is private debt, have simply overwhelmed both the capability and the interest in proper credit analysis across who knows how many funds, packaged securities, loans, and regulated or unregulated financial entities. Despite some recent debacles beginning to ripple through credit markets—First Brands, Tricolor, and the first wave of a few banks reporting “oops” (Zions and First Alliance)—the investment world is not a fraudulent stew of rapacious thieving (ignoring swaths of AI, crypto, meme stocks, SPACs, and Chinese Nasdaq listings for the moment). We are simply the humans who compose global financial markets and have thousands of years of practice being, frankly, lazy, greedy, and reptilian in nature. With trillions in capital flowing, being prudent in the cycle we’ve witnessed for most of the last decade has become a worn-out shell of its Ben Graham self.

We can go back to the well and trot out Minsky cycles—chains of financial crises with intermittent periods of stability. Or we can dimly recall that the 90% of an English major sacrificed for an economics degree yielded this truth: “Stupidity is an enduring feature of human existence but inherently not modelable.” – Flaubert.

On a practical basis, every day someone paid to invest on behalf of someone else lives in a rat’s nest of professional jealousy, no matter how tight the professed discipline. Each week that some piece of nonsense goes up 32% on the most glaringly near-fraudulent press release referencing the hot themes du jour—and you aren’t there—it begins to wear on the soul. Each credit deal or VC opportunity that is passed on becomes a recrimination opportunity at the weekly meeting. And thus, each day, some diligence slips. And slips. But don’t the 20 analysts at Egan-Jones Rating Company who rated over 3,000 private debt deals in 2024 use AI for this passé white-collar work?

We take the side of Jamie Dimon: “I probably shouldn’t say this, but when you see one cockroach, there are probably more,” Dimon said on an earnings call a few weeks ago. Marc Lipschultz, Co-CEO of Blue Owl Capital, responded a day later with, “Banks might want to look at their own books for any cockroaches,” implying that the 40%-ish growth in AUM for Blue Owl—mostly in private debt over the past five years—is, of course, not a problem for “them,” just everyone else (which is standard talk for any CEO in any industry). “It’s not a private credit issue. It’s a liquid credit market.” To their credit, Blue Owl does have among the lowest percentages of PIK income in their publicly traded Business Development funds versus peers, though as a group, PIK-related income is up about 30% year-to-date per Pitchbook data.

There’s no doubt mistakes have been made worth “at least tens and tens of billions of dollars” (CSC’s carefully calculated estimate)—whether in credit or the mad rush for something labeled AI. “Time and tide wait for no man or credit cycle,” but apparently, they can be suspended by accommodating government officials who have enabled stupendous risk-taking that few have the permanent capital to resist, while the rest of the crowd continues to hear danceable music.

And to the credit of the Aspen/Amagansett crowd, the creation of massively funded capital food chains that fund, lend, repurchase, and trade said mistakes is simply an Olympus-sized pool of fees and jealousy. To wit, the simply named “Continuation Fund” explosion enables PE firms to roll assets between early and new funds, allowing clients to keep the best and last investments in the fund even longer—or, more cynically, to account for “exit constipation” on the last unsaleable and/or over-levered fund garbage. The client tab is now running north of $50 billion in deals year-to-date.

The one newish twist this cycle, compared to previous ones, is that after the GFC, regulations were routinely trotted out to fight the last war. And thus, we have the giant private credit scrabble of interlinking firms and structures. So what does the enterprising regulated banker do? He lends to the companies that make the loans rather than going direct. Ingenious “risk transfer” that, of course, is no such thing. The official term is Nondepository Financial Institutions (NDFIs)—broker-dealers, hedge funds, private equity/credit funds, securitization vehicles, and subprime auto lenders.

We argue this will be an ongoing problem. On the margin, more thoughtful allocation—what to buy and at what valuation—will weigh on future returns given the elevated starting point at which many assets trade. In other words, there will again come a period when people mistrust counterparties, mock the pitchbook in front of them, and laugh at the Excel spreadsheet with ten years of projections that suddenly look quaint. Extending credit or liquidity to strangers has a funny history of disappearing in a hurry—like grasping at clouds. But in the meantime, who seems to care? The stock market is up, and obviously that means we’re on the right macro course. The fact that what I own is up makes me smarter than you. (October 19th, 2025—Dan the Bartender at the new tiki restaurant frighteningly close to our office.)

Yes, we always worry and fret when things are going absurdly right. “I’ve been in the investment business for 35 years, and I can tell you that corrections are healthy. They’re normal. What’s not healthy is straight up,” Treasury Secretary Bessent said during an interview on NBC’s Meet the Press in March. He followed that last week in the Financial Times with, “Where the hell is the market risk? They’ve just been wrong.”

As much as I enjoy his eye-rolling and banter with elected numbnuts, if you understand his career and his “lean,” you understand he should talk less—and we should be more careful. The question is, what does it mean for the rest of us in the non-zero probability of lots of billions of dollars of capital actually being erased from the nonsense side of the world? If you use leverage, you don’t need a big problem to have a problem—you’ll have the first problem. Some argue that when equity capital goes to zero, it has less economic impact on life as we know it than chains of leveraged transactions. Well, we sort of have both, if you count AI spend in the former and the rest of the yack in the latter.

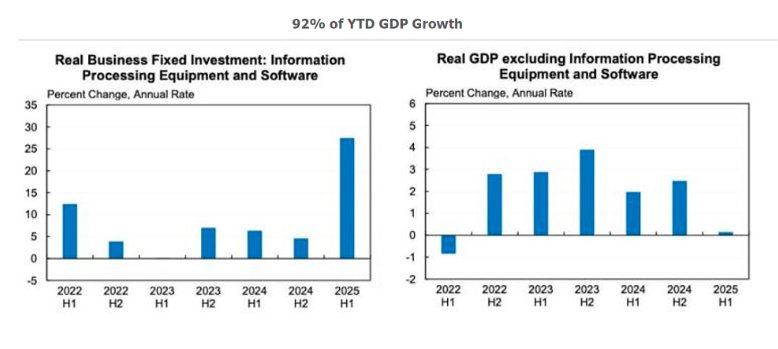

Copied and pasted from somewhere formerly unknown to me, Harvard economist Jason Furman recently noted that investment in information processing equipment and software is four percent of GDP—but responsible for ninety-two percent of GDP growth in the first half of this year. GDP excluding those categories grew at a 0.1 percent annual rate in the first half.

Which would be the obvious comeback from Jerome Powell if I asked him what the hell he’s doing orchestrating Fed rate cuts while gold, crypto, and a few trillion dollars’ worth of “high-valuation equities” hit new weekly highs. A good chunk of the rest of the economy is laboring under questionable demand and consumer hesitation—except, of course, for the boxes or loge seats at Dodger Stadium.

I’ve learned the hard way that even if one thinks they’re not doing the dumb thing of the day that goes to zero—or doesn’t reach its 2025 high until 2032—there’s always risk you don’t see on the screen in front of you. Maybe it’s a “relative value” mistake. Maybe it takes six years to resolve in your favor instead of three. Maybe it’s lax confidence in diversification, which can hide the true risk characteristics of a portfolio that’s a group of business models worse than you think. And we all should remember that special magic never on my CFA exam: when the mess hits, all “perceived poor-quality” assets trade as one in a glorious mess-athon.

All that said, we are having a good year performance-wise because we compile “big-picture thoughts” at night watching the Yankees lose or the LA Kings give it up in the third period, and come into the office for our day job—finding very cheap stocks that over-discount a present problem, or solid business models at reasonable prices that can compound.

As the ever-so-good Robert Armstrong of the Financial Times writes:

We’ve had an interesting year whereby our separate account effort in small and micro—25 to 30 stocks—is “super,” while our LP rounding up to six stocks as we speak is punking along in the single digits. Having more oars in the water in an up market helped the former, while the LP is treading more water in the absence of an event or compounding recognition—the exact opposite of last year. But all in all, good clean fun, and we invite a chat to discuss the longer term, since the CSC principal has improbably managed to put together a 30-year double-digit track record in the not-so-exciting world of value and smaller caps.

Now, when are we getting to Taylor and Travis, you ask? For those 7% who open our Strategy Letter emails and actually read them (and we know who you are: https://covestreetcapital.com/six-flags-see-you-at-the-christmas-party-taylor/), you know where we’re going here. The rest can go back to weekend reading school and catch up on our recent investment in Six Flags. As much as we like to be right quickly—for reasons we didn’t think of—the next phase is crucial if we’re going to make solid, longer-term money: a CEO choice. TBD.

Some other ideas have surfaced in unusual places. From time to time, companies have problems assembling financial statements or flipping the switch on new ERP systems. Problems ensue, the SEC, NYSE, or Nasdaq take issue, and the stock gets temporarily delisted to the “Pink Sheets”—which are not all Chinese or Nigerian AI scams. Schwab and Merrill Lynch like this even less and often restrict trading—sometimes allowing only sells, not buys. Predictably, no one likes any of the above. We’ve bought two companies that are profitable and poised to relist. Oh right, the SEC has been effectively closed for 30 days and is not acting upon petitions. Interesting opportunities.

To paraphrase strategy guru Michael Porter, the essence of portfolio management is often choosing what not to do. We are not doing $20 billion market caps that are not even EBITDA breakeven. We are not betting on the world being irreversibly different or irreversibly doomed. All “performance”—whether by stock, manager, or index—is usually the result of a narrow focus of blooming success, but never in my career have I seen more investors hold more assets referencing a single theme than today. It’s reminiscent of 1999/2000, when we ended up with fast food and the “hopeless idiot” at Berkshire while the party raged in Dot-com. Investing in the hottest concept the world’s smartest men can offer in size is not easy to ignore, but I can assure you it’s often worth the effort.

We are doing smaller-cap healthcare. We own three billboard companies. Ag-chem, to which we’ve added today in FMC—one of those sublime moments where we stare lazily at a screen watching a trade confirm at one-third the price at which we sold it. Smaller-cap defense and aerospace. Management change and capital allocation improvement—because the greatest opportunities always occur around change. The valuation of a company will not change unless something changes intrinsically about the company (financially, operationally, or strategically), and “people change” is the hardest thing for others—or for AI—to evaluate. Clients know our names—come be educated!

Speaking of which, a number of readers might be aware that we’ve shrunk assets and people—some out of the blue, some not of our own doing, and some by design. The Lead Principal and Portfolio Manager still loves every day of investing; he’s just had enough of the “stuff” of industry practice. Fortunately, technology and modern structure allow much of the “doing” to be outsourced, and we’ve done it. An LP really makes life easier.

Three brief reference points for context: While looking at preschool options for my twins 21 years ago, we had a choice between the “new, spiffy, anyone-who’s-anyone-goes-here” school and the older rabbit warren of a Montessori site within walking distance. The head of the latter told us, “We are perfect for any child; we are not perfect for every parent.” Boom.

Architect and designer Juan Montoya said this year in the Wall Street Journal that he’s “only taking projects I absolutely want to do with people I really like. I don’t want to need to have a client who is a nightmare but pays very well just so I can pay the rent—I’m not going to be happy.”

Lastly, Graham Weaver, the absurdly successful founder of Alpine Investors (who’s admittedly become a bit tiresome on the speaking circuit), once said: “We wouldn’t get there by doing what everyone else did. The crowded, clearly marked path is rarely where you’ll find your winnable game. The people we admire most—the authors, musicians, poets, entrepreneurs—all found a game no one else was playing. They lived into who they were and played their own game.”

I don’t like to stand in front of anyone with a pitch I’m not 120% confident in. So no, there’s not a perfect correlation between performance improvement and fewer people, fewer meetings, and fewer 13 versions of the same report no one reads—but maybe it’s 80% facing the right direction.

And it’s a joy to have an office “driver, driver, five-iron” from home, with an ocean view and a world-class taco across the street.

But the bigger things haven’t changed: work to understand business models, people, and valuation. Don’t be afraid to act when the combination lines up—which, as many will recall again in the future, is the hardest part.

We are open to new partners.

Jeffrey Bronchick, CFA

Principal, Portfolio Manager

Cove Street Capital, LLC

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

*The opinions expressed herein are those of Cove Street Capital, LLC (CSC) and are subject to change without notice. Past performance is not a guarantee or indicator of future results. Consider the investment objectives, risks and expenses before investing.

You should not consider the information in this letter as a recommendation to buy or sell any particular security and should not be considered as investment advice of any kind. You should not assume that any of the securities discussed in this report are or will be profitable, or that recommendations we make in the future will be profitable or equal the performance of the securities listed in this newsletter. Recommendations made for the past year are available upon request. These securities may not be in an account’s portfolio by the time this report is received, or may have been repurchased for an account’s portfolio. These securities do not represent an entire account’s portfolio and may represent only a small percentage of the account’s portfolio. Partners, employees or their family members may have a position in securities mentioned herein.

CSC was established in 2011 and is registered under the Investment Advisors Act of 1940. Additional information about CSC can be found in our Form ADV Part 2a,

© Cove Street Capital

Read more commentaries by Cove Street Capital