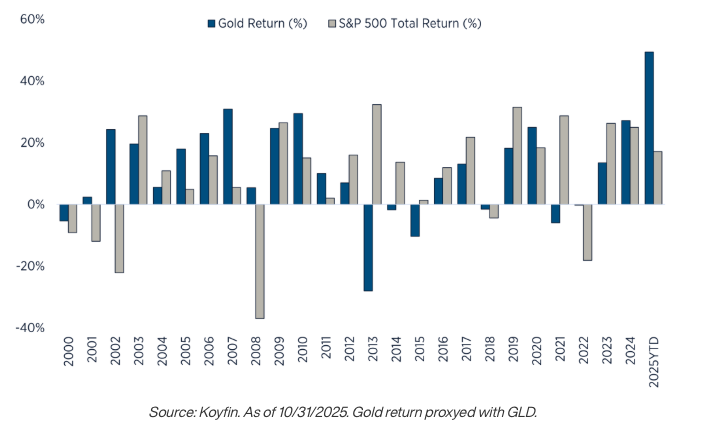

Following this year’s impressive rally in gold (the best year for the metal since 1972) investor attention has once again turned toward its role as a long-term portfolio component.

As a tactical trade, timing gold can be challenging (See our previous post on timing gold). Its movements often reflect macroeconomic uncertainty, inflation expectations, and shifts in real yields, making entry points unpredictable. Yet, viewed through a longer lens, gold’s resilience has been notable: since 2000, gold has outperformed the S&P 500 in more than half of all calendar years (53%).

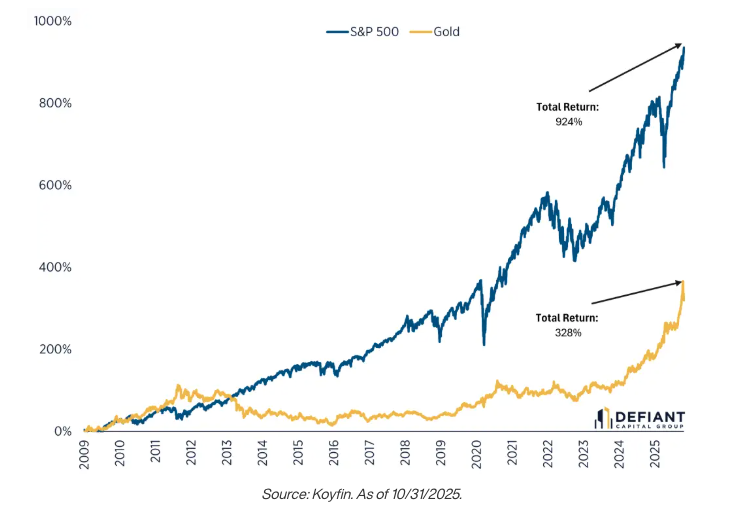

While Gold has outperformed the S&P 500 annually, an investment in the S&P500 still outperformed gold due to outsized return years, dividends, and compounding effects. However, gold’s consistently strong performance begs the question – should Gold be considered as a “core” portfolio allocation.

Rethinking Gold in a Diversified 60/40 Portfolio

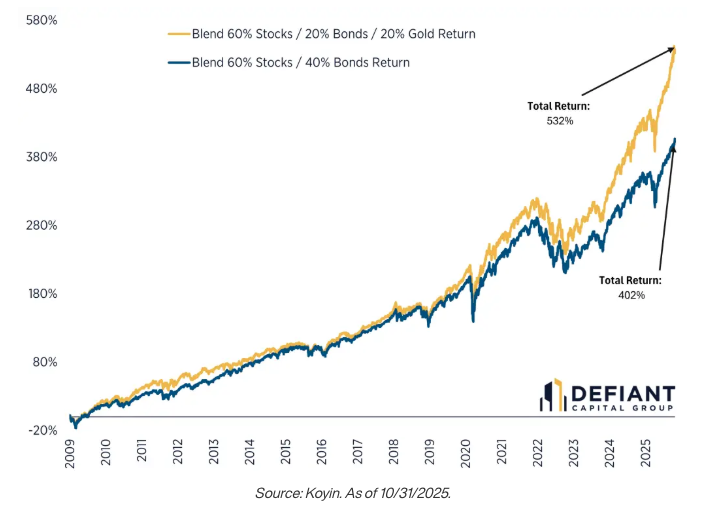

However, the recent rally had us questioning how gold would have performed within a more diversified portfolio. So we went back and analyzed how a 60/40 portfolio would have performed if the fixed income allocation was split between bonds and gold.

Now, to be clear, we aren’t advocating that investors abandon equities or traditional fixed income. However, gold’s performance over multiple cycles highlights its potential role as a strategic diversifier, particularly in an environment marked by elevated inflation, rising debt levels, and shifting monetary policy.

To test this, we compared two traditional allocations: a 60/40 (equity/bonds) and a 60/20/20 (equity/bonds/gold).

The results were striking. Even with a modest allocation, portfolios that included gold delivered stronger long-term risk-adjusted returns and reduced drawdowns during periods of market stress.

That said, there are some important caveats that investors should keep in mind:

-

Short-term underperformance: In strong equity years, portfolios with gold may lag traditional benchmarks.

-

Diversification, not replacement: Gold’s role is to complement equities and bonds, not replace them.

-

Long-term orientation: The benefit of gold emerges most clearly over full market cycles, not months or quarters.

Gold’s Bottom Line

Portfolio construction is both an art and a science. The best portfolios are designed not for the last crisis, but for the next one.

While a 20% allocation to gold may not be suitable for every investor, maintaining a core allocation to real assets, which may include gold, can strengthen portfolio resilience, especially when inflation or interest rate regimes shift unexpectedly.

Gold’s lesson isn’t about chasing performance. It’s about designing portfolios that endure across market cycles.

Please read important disclosures here.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group