Fourth Quarter 2025 Asset Allocation Outlook

- We expect no recession over our three-year forecast period, with GDP growth near trend, driven increasingly by business investment.

- Anticipated fed funds rate cuts will stimulate the economy and address weakening labor markets.

- Inflation is likely to remain around 3%, above the Fed’s long-term target.

- Passive flows continue to support domestic equities, primarily benefiting large cap stocks, which we add to this quarter.

- International developed equities are expected to benefit from government fiscal spending, attractive valuations, and a weakening dollar.

- Gold and Treasury positions remain in the portfolios as a hedge against geopolitical risk.

Economic Viewpoints (Charts 1&2)

We expect economic growth to remain near its long-term trend, neither booming nor stalling. The underlying drivers of growth, however, are shifting. Business investment has become the engine of expansion, driven by tax-incentivized capital expenditures, resilient corporate balance sheets, and ongoing reshoring and automation efforts. Technology investments have been especially strong as the AI boom continues, providing a steady base for GDP growth. Additionally, both fiscal and monetary policy are expected to bolster the domestic economy over the forecast period. Fiscal policy continues to be supportive through deregulation, tax policies, and industrial initiatives. At the same time, the Federal Reserve has signaled its intention for further easing. Together, these dynamics create a constructive backdrop for continued expansion and renewed business investment.

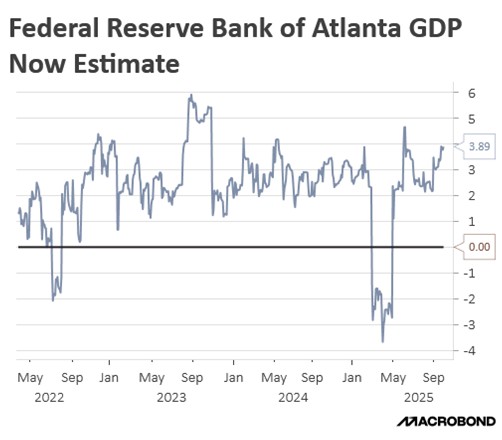

The Atlanta Fed’s GDPNow model currently estimates real GDP growth at 3.9% for the third quarter, reinforcing the view that the US economy remains resilient. The GDPNow model provides a real-time estimate of quarterly GDP growth, continuously updated as new reports are released. This often provides an early read on the economy.

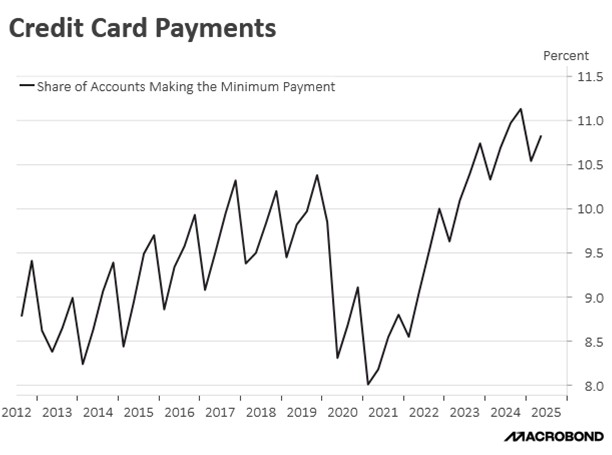

Overall, consumer data has remained stable, but we are starting to see weakness at the margin, particularly in discretionary spending. Credit card balances are rising while savings rates decline, suggesting that households are maintaining spending through leverage rather than income growth. Projections are for consumer spending to decelerate as income growth and savings buffers weaken. The current savings rate at 4.6% is below the 20-year moving average but above the post-pandemic low. This second chart indicates that an elevated level of credit card holders are making only the minimum payment on their balances, even as the current level is off its recent historic high. If credit stress intensifies, consumer confidence and spending may further deteriorate. Households are clearly facing stress, although it should be noted that most of the concerns reside with the bottom 60% of households in terms of income distribution. Higher income households continue to consume, buoyed by strong asset markets.

Household consumption depends heavily on the strength of the job market. Real wage gains have flattened, and the labor market, though still tight by historical standards, shows signs of stagnation. Many firms are opting to pause hiring, reduce hours, or allow natural attrition, in marked contrast to the labor hoarding of the past several years. Demographic shifts, particularly among foreign-born workers, and waning labor participation rates, especially among the younger cohort, are also weighing on labor supply.

Inflation is likely to settle closer to 3%, reflecting structural pressures of deglobalization, demographic constraints, and sustained fiscal support. The policy mix remains expansionary as fiscal policy continues to bolster business investment, while monetary policy, though restrictive in nominal terms, has turned neutral in real terms as inflation stabilizes. With the Fed on a path of easing and political incentives aligned for continued spending, both pillars of policy are working to uphold nominal growth.

Stock Market Outlook

Against this backdrop, market dynamics are being increasingly shaped by flows rather than fundamentals. The dominance of passive investment vehicles continues to benefit large cap equities and momentum-driven sectors, compressing dispersion and concentrating US market leadership. We expect this dynamic to continue in the short to medium term. Decreased recession risk and the continued capex boost within the technology sector prompted us to shift our growth/value tilt modestly toward growth to capture upside while managing valuation risk. At the same time, we reduced mid-cap exposure in favor of what we view to be more compelling opportunities in large caps. We continue to hold dividend-oriented ETFs across large and mid-cap allocations as dividends tend to provide meaningful support in the higher-volatility environment we expect. Within sector positioning, we maintain exposure to advanced military technologies amid ongoing geopolitical tensions. While we recognize that US small cap stocks should benefit from anticipated lower rates, we remain void this sector as we see more opportunities from the larger capitalization stocks. Small caps are still likely to face greater headwinds from tariff-related pressures, higher financing costs, and limited pricing power that could compress margins.

A combination of policy changes and macroeconomic trends is likely to weaken the US dollar, enhancing the return potential of international assets for US-based investors. We maintain our allocation to foreign developed markets, with selective increases this quarter in certain portfolios. Europe, in particular, is likely to experience growth on the back of increased investment in defense and infrastructure. As such, within international developed equities, we maintain a broad-based index and a Europe-focused allocation. We also maintain our international developed small cap value equity position, which could outperform amid global trade realignment as they’re less exposed to cross-border disruptions and benefit directly from regional fiscal stimulus. With significant exposure to industrials and materials, these holdings are well positioned to benefit from the aforementioned fiscal spending. Strong valuation and profitability characteristics further support the return potential within this segment.

Bond Market Outlook

Monetary policy is likely to be accommodative over the coming year. With inflation stabilizing near 3% and growth normalizing, the Federal Reserve has signaled a willingness to ease monetary conditions. A leadership transition expected next spring is likely to reflect a more dovish posture. The next Fed chair is widely anticipated to prioritize employment resilience and debt sustainability over attempting to corral inflation to the Fed’s target level of 2%. Consequently, the new chair will likely advocate for a continued reduction in the fed funds rate following several years of tight monetary policies that elevated real rates. In addition, an end to the Fed’s quantitative tightening program will probably be part of this more dovish stance. As policy recalibrates, we expect a decline in short-term rates and a modest steepening of the yield curve.

Within fixed income, we moved more into the intermediate-maturity section of the curve. Credit markets are currently well supported by ample liquidity, reflecting low default rates, steady growth, and a manageable inflation backdrop. However, credit spreads hold the potential to widen moderately from tight levels due to heavy refinancing needs, though not to distressed levels. With spreads now below their long-term averages and little room for further tightening relative to Treasurys, we expect relatively limited return potential and recommend maintaining an underweight allocation to corporate credit.

We continue to emphasize US Treasurys and seasoned mortgage-backed securities (MBS) for stability and income, while maintaining selective exposure to high-quality speculative-grade bonds. These allocations position portfolios to benefit from the policy pivot toward easier conditions and a more balanced growth-inflation environment.

Other Markets

We continue to hold gold across all strategies, viewing it as a strategic asset. Central banks remain steady buyers, underscoring gold’s role as both a store of value and an inflation hedge. Ongoing geopolitical tensions and the global shift to diversify away from US dollar dependence are likely to keep demand firm, reinforcing the importance of gold within a diversified, risk-aware allocation. Although gold has proven to be a beneficial holding in the strategies, as it continues to mark historic highs, we are continuing to monitor its ongoing appeal.

Originally published by Confluence Investment Management

For more news, information, and strategy, visit the ETF Strategist Content Hub.

A message from Advisor Perspectives and VettaFi: Stay ahead of market changes with our daily updates on key market and economic indicators. Visit the AP Charts and Analysis site for our expert insights.

© Confluence Investment Management

Read more commentaries by Confluence Investment Management