In our experience, “owning the index” in commodities may deliver results that fall short of what investors might expect. We think it’s important to understand that this is a feature of how commodity indexes are built, not an inherent characteristic of the asset class itself. We’ve found that most of the gap between expectations and reality boils down to one thing: weighting methodology.

Every fall, commodity index providers ritually announce their index’s target weights for the upcoming calendar year, which typically go into effect in early January. As we approach the 2026 announcements, let’s revisit why weighting methodology matters. This may help investors make better choices, without undermining their goals—like inflation mitigation and portfolio-level diversification—for investing in commodities.

Looking under the hood of popular commodity indexes

As commodity allocations migrate from “nice to have” to “need to have” for inflation hedging and diversification, three benchmarks have attracted the most passive assets:

- Bloomberg Commodity Index (BCOM)

- S&P GSCI1

- Dow Jones Commodity Index (DJCI)

What do these indexes measure? To clarify a common misconception, they don’t represent the returns of either equities or physical commodities. Mining, energy and agriculture stocks certainly have a commodity component to their returns, yet broader swings in the stock market can overwhelm their underlying commodity exposures. Physical commodity holdings can also prove problematic for most investors because of the need to transport and store the raw materials. Most of us don’t have the space to stash 100 barrels of oil or the land to raise a herd of cattle.

For those reasons, index providers have decided to base their exposures on fully collateralized commodity futures positions. The price of a futures contract is derived from the underlying commodity. Given that all three indexes are put forward as describing the broader commodity asset class, some odd facts surface when we dig a little deeper into their risk and return characteristics.

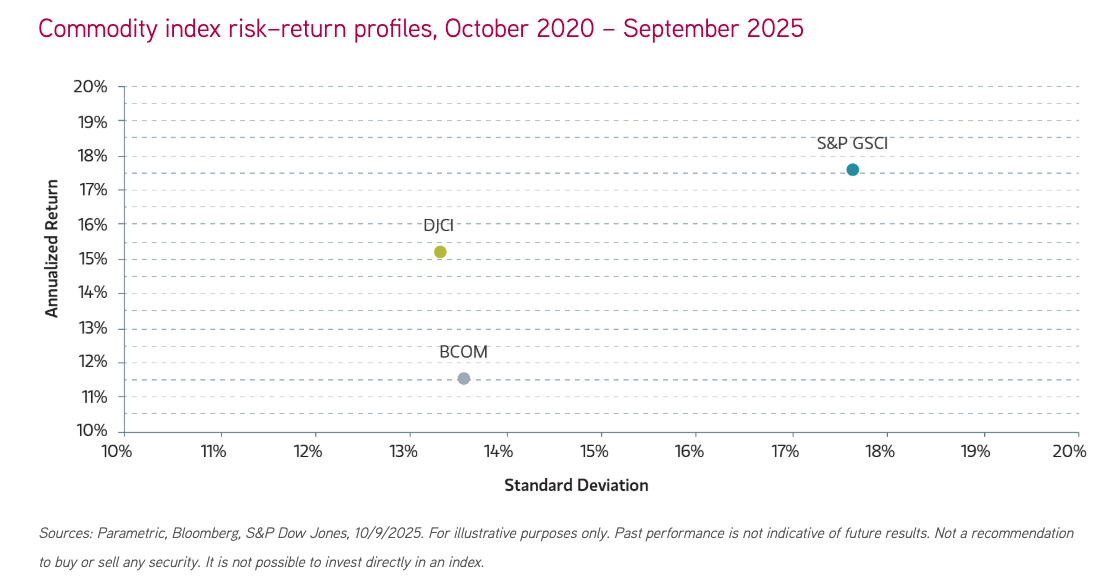

Over the past five years, we’ve seen dramatically different values for these metrics—ranging from an annualized return of 11.5% for BCOM to 17.6% for S&P GSCI, while volatility (measured by the annualized standard deviation) swings from 13.3% for DJCI to nearly 18% for S&P GSCI.

For comparison, if we plot the five-year annualized returns and standard deviations for two common US large-cap equity indexes, S&P 500® and Russell 1000, we find very little deviation in their performance or risk. The annualized five-year return was 16.5% for S&P 500® versus 16.0% for Russell 1000. Likewise, volatility was 15.8% for S&P 500® versus 16.1% for Russell 1000.

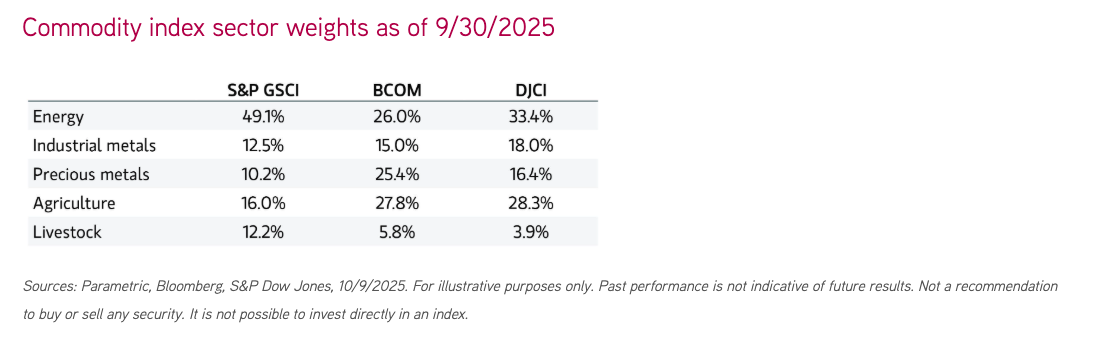

To understand why their risk-return profiles vary so much, let’s take a quick look under the hood at each commodity index’s sector exposures. We find noticeably different weights for each major grouping.

Whenever an investor buys a futures contract, another market participant simultaneously sells an equal and offsetting position. This construction feature allows the establishment of a futures market in a commodity to balance supply and demand, without having a major impact on prices in the spot market for that commodity. Due to this structure, all contracts have zero market capitalization.

That’s where the uniqueness of commodity indexes being based on futures contracts, and not physical commodities, comes to bear: The concept of market capitalization breaks down. So in a sense, there are no natural market weights for the constituents in a commodity index.

Needing a consistent weighting mechanism, index providers developed a variety of supposed proxies to play a similar role in their indexes—including global production for S&P GSCI, blending liquidity and production for BCOM and equally weighting sectors for DJCI.

Ultimately, we can find no clear argument why any one of these proxies is better than the others. What becomes apparent, though, is that these indexes function more as commodity-trading strategies than as passive slices of the market. Of even greater concern, their weighting schemes tend to create sizable concentrations in certain sectors or in a small number of commodities, which can create more volatile investment outcomes.

Index concentration means more risk, less reward

The commodity asset class exemplifies the significant benefits of diversification in investing. Commodity prices are subject to substantial volatility—frequently fluctuating by several percentage points daily—yet these movements typically occur in varying directions across different commodities. Incorporating a broader range of commodities into a portfolio can help to mitigate risk and potentially enhance returns.

For instance, rather than experiencing pronounced swings such as a 6% rise one day, followed by a 4% increase the next, only to drop over 12% within a week—as observed with oil prices in June—a diversified portfolio may exhibit considerably less dramatic fluctuations.

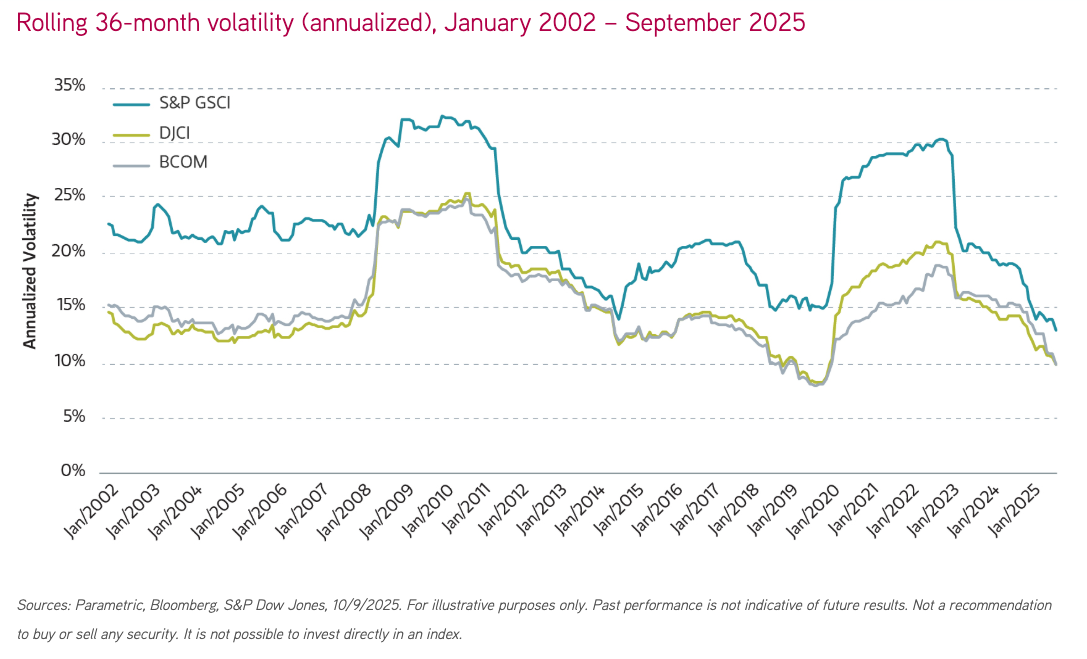

While diversification is likely a familiar concept to most investors, its importance is particularly pronounced in commodity investing, where performance tends to be unpredictable. Historical data indicates that indexes with greater concentration have experienced greater risk.

Our index sector exposure analysis reveals that S&P GSCI is notably more concentrated in energy products relative to other indexes, while exhibiting substantially higher volatility. Even though the energy sector has often been the most volatile, we suspect mismatches in sector volatility are unlikely to be the sole cause of this result.

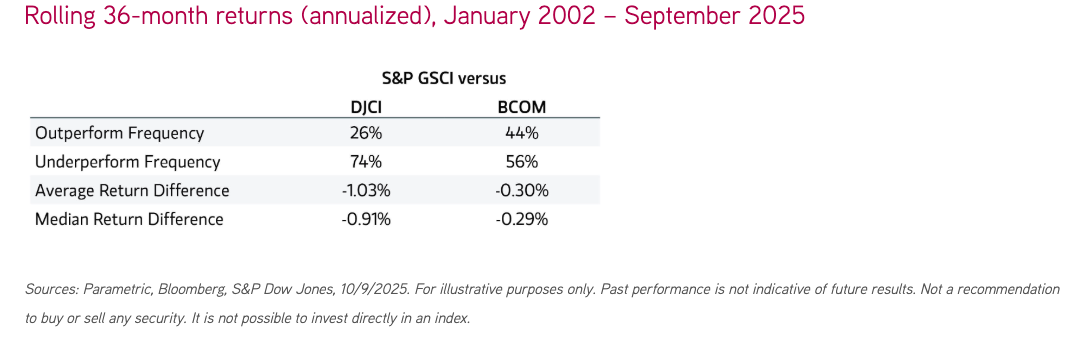

Unfortunately for investors, bearing the added risk has not been compensated with higher returns. Over most rolling 36-month periods, S&P GSCI lags both BCOM and DJCI.

During approximately 75% of our rolling 36-month periods, DJCI outperformed S&P GSCI, while BCOM demonstrated superior performance in 56% of instances. On average, S&P GSCI lagged DJCI and BCOM by -1.03% and -0.30%, respectively. These results suggest that diversification within commodities may be associated with reduced risk and higher average returns.

Investors hoping to put these findings into action may want to consider looking beyond the traditional index offerings within the asset class and seeking out strategies that offer even greater levels of diversification. Our analysis indicates that further risk reduction and return enhancements may be possible with better diversification.

The bottom line

Owning the index in commodities can deliver very different—and sometimes disappointing—outcomes because each index uses its own weighting proxy, producing diverging sector and commodity tilts that often lead to varying risk and return outcomes. Since commodity indexes are built on futures contracts rather than market cap weights, they tend to behave more like trading strategies and often concentrate in certain sectors or commodities, which can undermine the goals of inflation mitigation and portfolio-level diversification. For investors, seeking out a well-diversified* commodity exposure, rather than defaulting to a headline index, may be better aligned with these objectives. Better yet, it may even come with improved performance.

1 Formerly the Goldman Sachs Commodity Index.

* Diversification does not eliminate the risk of loss.

The views expressed in these posts are those of the authors and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and Parametric and its affiliates disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Parametric are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Parametric strategy. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results. All investments are subject to the risk of loss. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the Disclosure page on our website for important information about investments and risks.

10.24.2026 | RO 4922890

Investment advisory services offered through Parametric Portfolio Associates LLC ("Parametric"), an investment advisor registered with the US Securities and Exchange Commission (CRD #114310). Parametric is also registered as a portfolio manager with the securities regulatory authorities in certain provinces of Canada (National Registration Database No. 42850) with regard to specific products and strategies. Parametric provides advisory services directly to institutional investors and indirectly to individual investors through financial intermediaries. The information on this website does not constitute an offer to sell, or a solicitation of an offer to purchase, securities in any jurisdiction to any person to whom it is not lawful to make such an offer. Investing entails risks, and there can be no assurance that Parametric (and its affiliates) will achieve profits or avoid incurring losses. All investments are subject to potential loss of principal. Parametric does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the disclosure page for important information about investments and risks.

S&P Dow Jones Indices are a product of S&P Dow Jones Indices LLC (“S&P DJI”) and have been licensed for use. S&P® indexes are registered trademarks of S&P DJI; Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); S&P DJI, Dow Jones, and their respective affiliates do not sponsor, endorse, sell, or promote Parametric and its strategies, will not have any liability with respect thereto, and do not have any liability for any errors, omissions, or interruptions of the S&P Dow Jones Indices.

©2025 Parametric Portfolio Associates LLC. All rights reserved. 800 Fifth Avenue, Suite 2800, Seattle, WA 98104.

NOT FDIC INSURED. OFFER NOT A BANK GUARANTEE. MAY LOSE VALUE. NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY. NOT A DEPOSIT.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Parametric

Read more commentaries by Parametric