Additional content provided by Brian Booe, Associate Analyst, Research.

In the mid-to-late 1630s, the beauty of tulip bulbs captivated European elites after arriving in the region from the Ottoman Empire. The cost for this symbol of wealth and status? Your house, or even around 12 acres of land. ‘Tulip mania’ is regarded as the first bubble in financial markets on record, making more recent bubbles seem much less radical in comparison, right? ‘Bubbles’ are characterized by a rapid escalation of market value of an asset which grows to greatly exceed the intrinsic value justified by fundamental methods. The genesis of the artificial intelligence (AI) rally in 2022 was the release of ChatGPT, which captured investor attention as the latest technology that will not only revolutionize everyday life, but also corporate America’s business models, workforce, and even supply chains. Even from the early innings, speculation resembling the dotcom bubble was apparent.

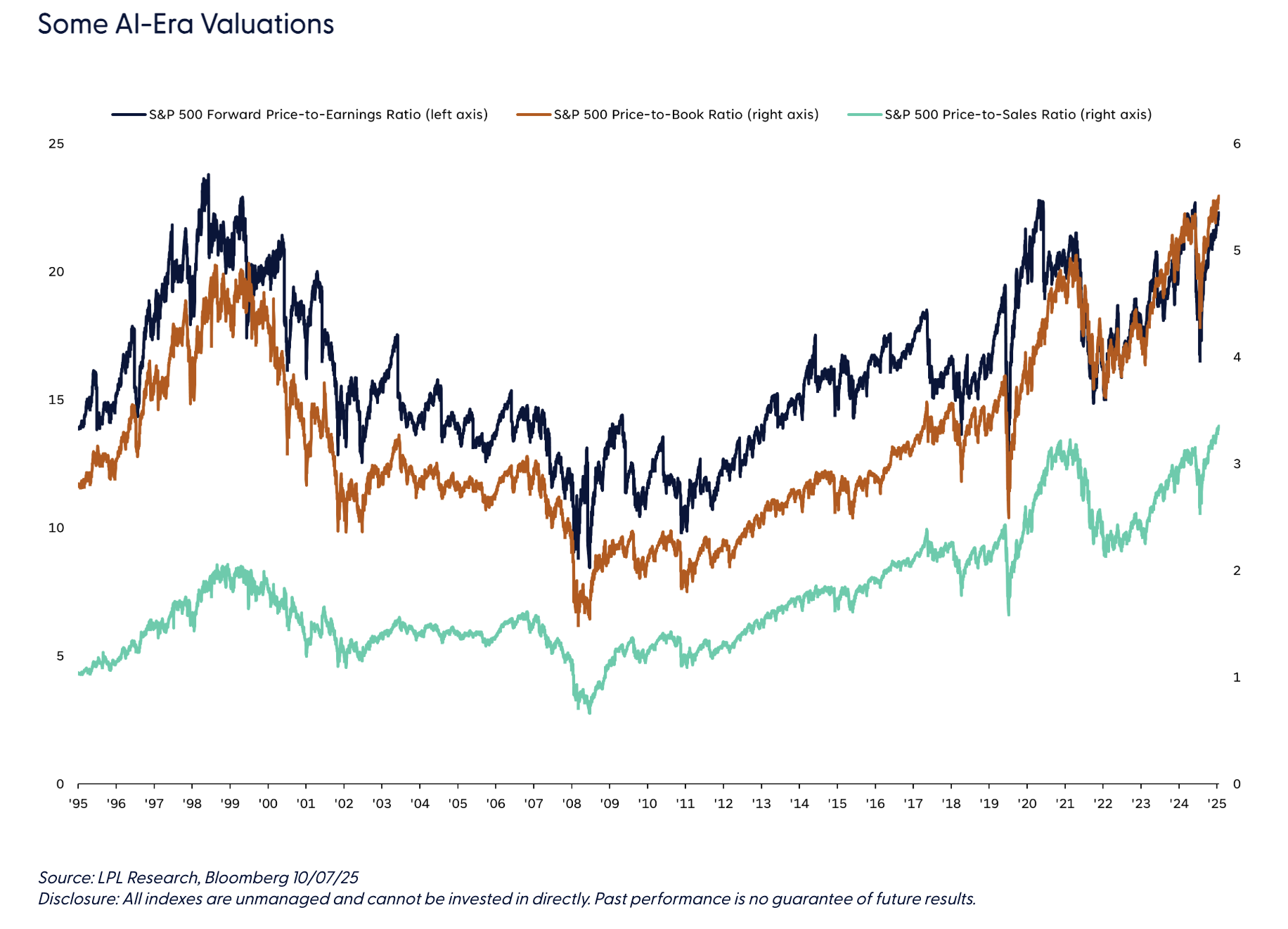

Valuations Send Mixed Signals

It is virtually impossible — for all intents and purposes — to call the top of the secular AI growth theme, and it is equally as hard to state with 100% certainty if we are in a bubble right now. But, given that the history of the dotcom era rhymes with the secular AI growth theme, how do they compare?

For starters, much has been said about equity valuations, and stocks are definitely trading at elevated multiples. However, the forward price-to-earnings ratio (P/E) of the S&P 500 has yet to reach dotcom era levels, and in fact remains below December 2020 levels because earnings were depressed coming out of the COVID-19 pandemic. The forward P/E for the equity benchmark is currently 22.2, after reaching 23.8 in late February 1999 before peaking at around 25 in March 2000 when the stock market peaked. So large caps stocks are expensive, lifted by AI-driven technology stocks, but not quite to the extremes of 25 years ago.

On the other hand, a lack of assets supporting valuations was a problem during the dotcom era, and the S&P 500 price-to-book ratio (P/B) is actually above late-1990s through early 2000s highs, while the price-to-sales ratio (P/S) for the index is well above late-1990s levels and at all-time highs. The superior profitability and asset-light business models of corporate America today warrant higher valuations on sales and book value.

But Internals Lean Brighter

Heavily concentrated markets are another lingering concern amongst market participants who draw parallels to the dotcom era. The tech sector made up roughly 33% of the S&P 500 at the end of February 2000, which is just below the sector’s 35% weight today. While market concentration is a real risk — index heavyweights have dragged down major averages in multiple sessions over the last year despite most individual names rising — valuations of top tech names seem more reasonable in comparison to the late-1990s. According to our friends at Evercore ISI Research, the median forward P/E for the current top 10 tech companies is at a ~45% premium to the S&P 500, compared to nearly double that of the index during the dotcom era.

Perhaps the key difference between the broader secular AI growth theme and the dotcom era is that large, AI hyperscalers have mostly funded capital expenditures (capex) with strong internal cash flows, not through AI revenue in singularity or by issuing debt or equity. In comparison, dotcom era spending was broadly funded through massive amounts of ‘vendor financing,’ which ultimately led to the circular flow of capital that fueled the bubble burst. The recent surge in bubble-related headlines was inspired by Oracle’s (ORCL) $300 billion data center deal with ChatGPT-parent OpenAI. The privately owned startup promised ORCL billions of dollars which OpenAI has yet to earn for computing facilities Oracle hasn’t built yet, sparking circular spending concerns.

Other Considerations

Other key differences between the 1990s telecom buildout and today’s AI cycle include a fed funds rate that is likely headed lower, not higher as they were at the turn of the century, more muted consumer sentiment, more moderate (but still strong) gains for the Nasdaq and S&P 500, and that the AI buildout is more constrained by physical resources. The fact is that AI will, and to an extent already has, change society. But the question is whether current valuations and investments will be justified by near-term returns, or if AI’s bright future is overpriced with an unclear arrival date.

Conclusion

The odds of an AI bubble that bursts are not zero, but today’s AI cycle is better capitalized than the 1990s telecom buildout and appears more durable and profitable in comparison. (One could also argue, from a contrarian perspective, that a bubble is less likely given all of the market chatter surrounding the phenomenon.) Nonetheless, the AI buildout’s durability will likely hinge on AI-generated earnings growth and cash flows, sustained utilization, and relief from power grid restraints, while circular spending would pose a risk. The amount of investment may end up falling short of optimistic expectations. And the returns on AI investment could eventually disappoint even if the AI revolution does not. The internet didn’t disappoint – it just took some creative destruction over many years to get there. AI is coming faster and probably will leave far less destruction in its wake.

LPL Research holds a neutral stance toward the technology sector and U.S. equities broadly, and will continue to monitor corporate developments, valuations, and fundamental metrics around AI spending, such as capex and cash flows.

Jeff Buchbinder, CFA, provides the top-down view of the stock market for LPL Financial Research. He has over 25 years of experience in equities.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #808398

A message from Advisor Perspectives and VettaFi: Transitioning your financial advisory business? Read our latest articles for guidance on launching an RIA, switching firms, or specializing.

Read more commentaries by LPL Financial