Asset allocation: Moving to overweight equities as economy stabilises

Global economic prospects are improving as a record four out of five major central banks are cutting interest rates and global business confidence is recovering from the negative impact of higher US tariffs. While the US government shutdown may provide fresh uncertainty, corporate profit and revenue growth remain healthy. All this suggests to us that there is upside in riskier asset classes in the medium term.

In contrast, government bonds look vulnerable. In the US, the asset class is not sufficiently discounting the risk of inflation given there is growing evidence of a tariff-induced spike in consumer price growth. At the same time, we are concerned that the Trump administration’s interference in the US Federal Reserve’s policymaking and governance could undermine the central bank’s independence and lead to a higher risk premium and steeper yield curves in US government bond markets. What is more, after falling to near 4% , 10-year US bond yields are now below our estimate of the long-term neutral levels.

In the rest of developed markets, while central banks are still easing, we estimate that on average policy rates are approaching a floor. This, in turn, should limit upside potential for fixed income.

Taking this into account, we upgrade equities to overweight, and downgrade bonds to underweight. Cash remains neutral.

Fig. 1 - Monthly asset allocation grid

October 2025

Source: Pictet Asset Management

Our business cycle analysis shows US economic growth has been resilient after a weak start to 2025, with second-quarter GDP growth rising by an annualised 3.8%. Inflation, meanwhile, is threatening to break higher with goods and services prices both running above their 25-year average. For these reasons, we think market expectations for Fed interest rate cuts are too aggressive.

We think the Fed will cut interest rates only twice more against market expectations of closer to four times by the end of next year. Our view is that the central bank will opt to act early, support the labour market and avoid overstimulating the economy.

The euro zone remains a bright spot, with resilient domestic demand offering support. Germany’s EUR1 trillion fiscal package is a key swing factor in the region's economic outlook: if implemented quickly, it could lift growth and inflation.

Emerging markets should also boost global growth as they benefit from improving industrial production, rising commodity prices and broad-based monetary and fiscal stimulus. The growth gap between emerging and developed economies stands at 7-8% on an annual basis, the widest since the early-2000s, which tends to foreshadow a gain in emerging market currencies and assets.

The economic picture in China is mixed. Retail sales remain weak and “Beijing’s anti-involution” policies aimed at curbing excessive competition are weighing on growth. The impact of US tariffs on Chinese exports, meanwhile, has been milder than expected, with export volumes declining only 2% since the new trade regime came into effect. Further coordinated monetary and fiscal stimulus should underpin growth in the world’s second biggest economy.

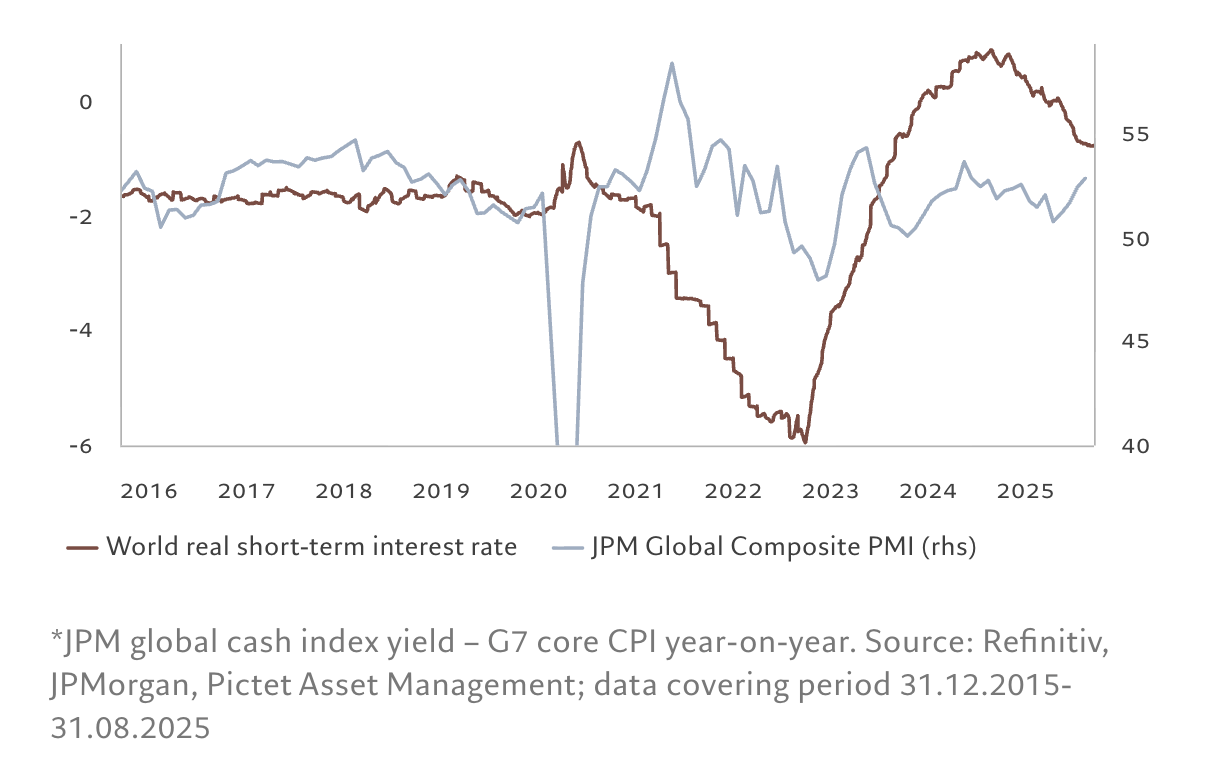

Our liquidity analysis shows 25 out of 30 major central banks are cutting interest rates, and that global excess liquidity is running at 4% on a six-month annualised basis.

Easier monetary conditions should go a long way towards shoring up economic activity (Fig. 2).

Also boosting liquidity is the fact that central banks appear willing to ease pressure on the bond market by scaling back the pace of quantitative tightening, as occurred in September in the UK.

Fig. 2 - Falling rates should support growth

World real interest rate* and JPM Global composite PMI

Europe’s liquidity conditions are positive for risky assets thanks

to a total of eight consecutive interest rate cuts. Japan is the only major economy with restrictive monetary policies in place.

In China, weak domestic demand should encourage authorities there to ease both monetary and fiscal policy. However, the pace of stimulus is likely to be gradual to prevent bubbles in risk assets as households rotate assets into equities.

Our valuation model shows that renewed optimism in earnings growth has led to an expansion in stocks’ price-earnings multiples that has pushed US stocks deeper into overvalued territory. In US equity markets, price-to-sales multiples now exceed dot.com and pandemic-era peaks, while earnings multiples of 23 times leave no buffer against the possibility of stagflation.

However, a further overshoot in 12-month price/earnings multiple, to above 27 times, is needed for the S&P 500 index to move into bubble territory, based on our analysis. US Treasuries are also expensive as inflation break-even rates remain too low given that price pressures appear to be building.

Finally, our technical indicators show a positive environment for equities. Investor flows into equities rebounded strongly, thanks to US investors buying domestic stocks beyond tech mega-caps. M&A activity is picking up and the next few months should prove supportive for risky assets. What is more, our sentiment indicators are still consistent with further gains.

Equities regions and sectors: warming to tech stocks

There is an increasing sense that equity markets are frothy. But while we recognise that stocks look expensive on valuation metrics and in some instances are looking ebullient, we don’t think the market is in bubble territory yet. That is because earnings have continued to grow at a steady pace. In fact, the latest results outstripped consensus expectations in a way that tends only to happen when markets are pulling out of recession. Nowhere is this more apparent than in IT.

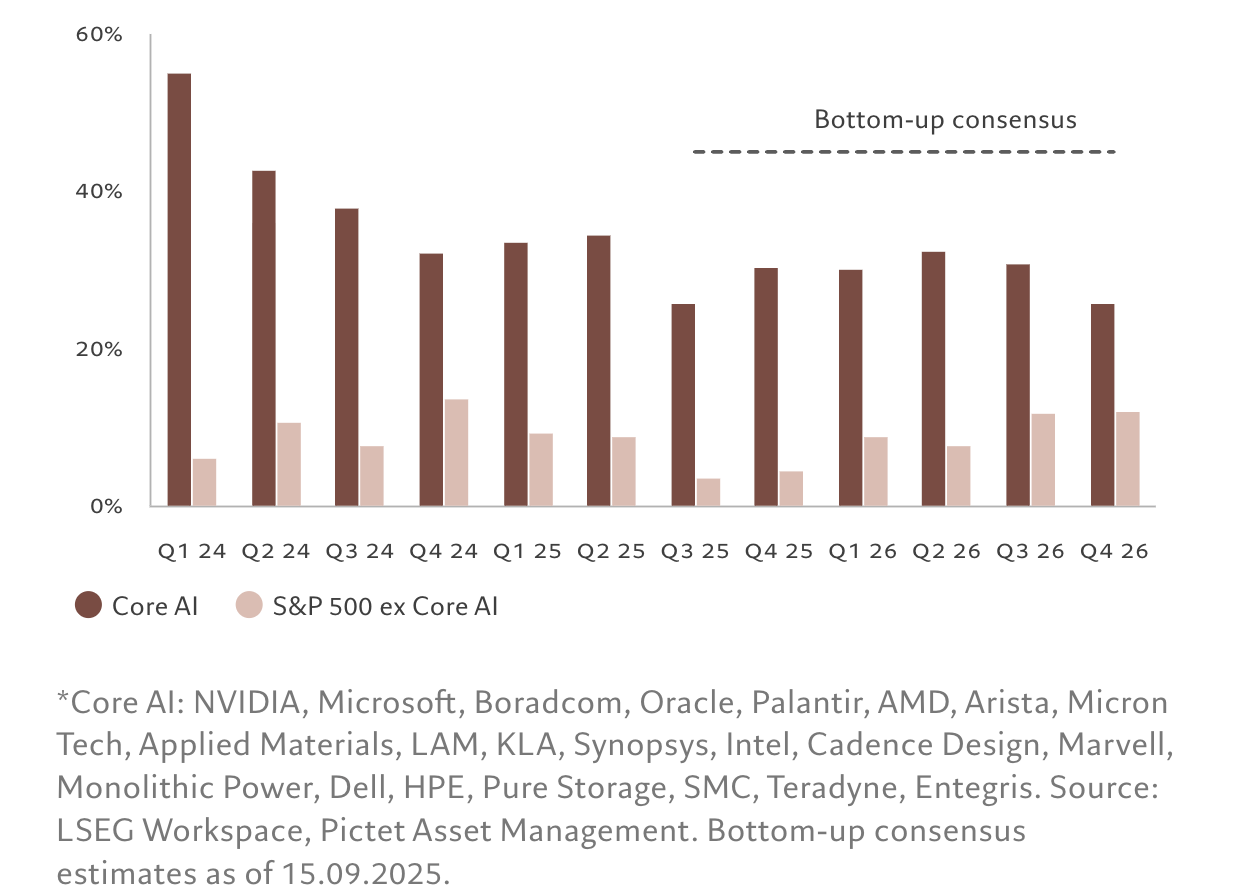

As a result, we upgrade IT to overweight. We’re cognisant that the sector is expensive on traditional valuation metrics, but we think that fundamental factors justify its premium. Earnings are growing at around 20% year-on-year with multiples below 30-times forward earnings. That compares to nearly 50-times at the peak of the dotcom bubble. We’re optimistic about earnings prospects, particularly in companies that have a strong artificial intelligence (AI) footprint – in fact AI is already making an increasingly positive impact on their revenues (see Fig. 3). Given that some 60% of the IT sector is already part of the AI ecosystem according to our calculations, that bodes well for its continued strong performance.

Fig. 3 - AI knocking it out of the park

Core AI* vs S&P 500 (ex-Core AI) quarterly earnings per share growth. Actual results to Q2 2025, bottom-up consensus forecast from Q3 2025.

We remain overweight communication services stocks. Here too, valuations are a little stretched, but corporate earnings are stable and the sector should continue to benefit from several tailwinds – not least those related to AI’s development and expansion.

We also remain overweight financials, which are poised to benefit from a steepening of yield curves as expected US rate cuts lower yields at the front end of the curve.

Banks typically benefit from the differential between deposit rates, which tend to be tied to official rates, and lending long, such as mortgages which are linked to long-dated bonds. Financials should further benefit from President Trump’s campaign to deregulate the sector. By contrast, we downgrade utilities to neutral – the sector has bond-like characteristics and we are on balance negative fixed income (see the Asset Allocation section).

The strong earnings season makes us optimistic about equities during the second half of the year. But by the same token, equity valuations are such that there’s little buffer against negative growth and policy shocks.

While we have shifted our sector allocations, we have not seen any justification for changing our regional exposure.

We remain overweight emerging markets as they offer attractive valuations and have benefited from the dollar’s drop this year. Emerging market stocks overall have strong momentum and inflows into asset class are accelerating too. We are also overweight Chinese stocks as they benefit from attractive valuations and the headroom authorities have for implementing further self-help measures.

The momentum in China’s tech sector has been spectacular thanks to strong AI-related investment spending. In Swiss-based portfolios we remain overweight Swiss equities which offer very attractive valuation relative to domestic bonds.

Fixed income and currencies: golden defences

Some economic clouds may have lifted but as many remain, we believe it is prudent to balance our overweight stance on equities with an overweight in gold.

The precious metal is up some 40% since the start of the year. That, of course, means stretched valuations, with gold ranking as the most expensive asset class in our model. Over the long run, however, the case for gold remains strong. Our Secular Outlook – our five-year view – projects that it will reach some USD4,500 an ounce by 2030 (compared to USD3,800 today), with possible overshoots along the way.

Looking at gold versus equities, money supply, and official reserves, the valuation is high but not extreme. The market value of outstanding gold now equals 20% of the market capitalisation of all stocks in the MSCI World – that may be approaching 21st century highs, but is well below the 370% level scaled in the 1980s. Similarly, while gold's share in official foreign exchange reserves is the highest in 30 years at 15%, it remains way off the 37% peak of 1980.

Technical signals are also supportive: gold is not obviously overbought, speculative future positions in the precious metal have decreased while trend signals are positive. Central bank holdings of gold are rising as they seek alternatives to adding to their dollar exposure. Retail investors have also recently joined the rush into gold, adding to their ETF holdings.

Also hedging our overweight stance in equities is our overweight in the Swiss franc, a traditionally defensive investment. We expect the currency’s strength to persist, even amid negative rates in Switzerland. We believe that the dollar is set for both a cyclical and structural depreciation, with the latest pause in the decline of the US currency likely to be short-lived.

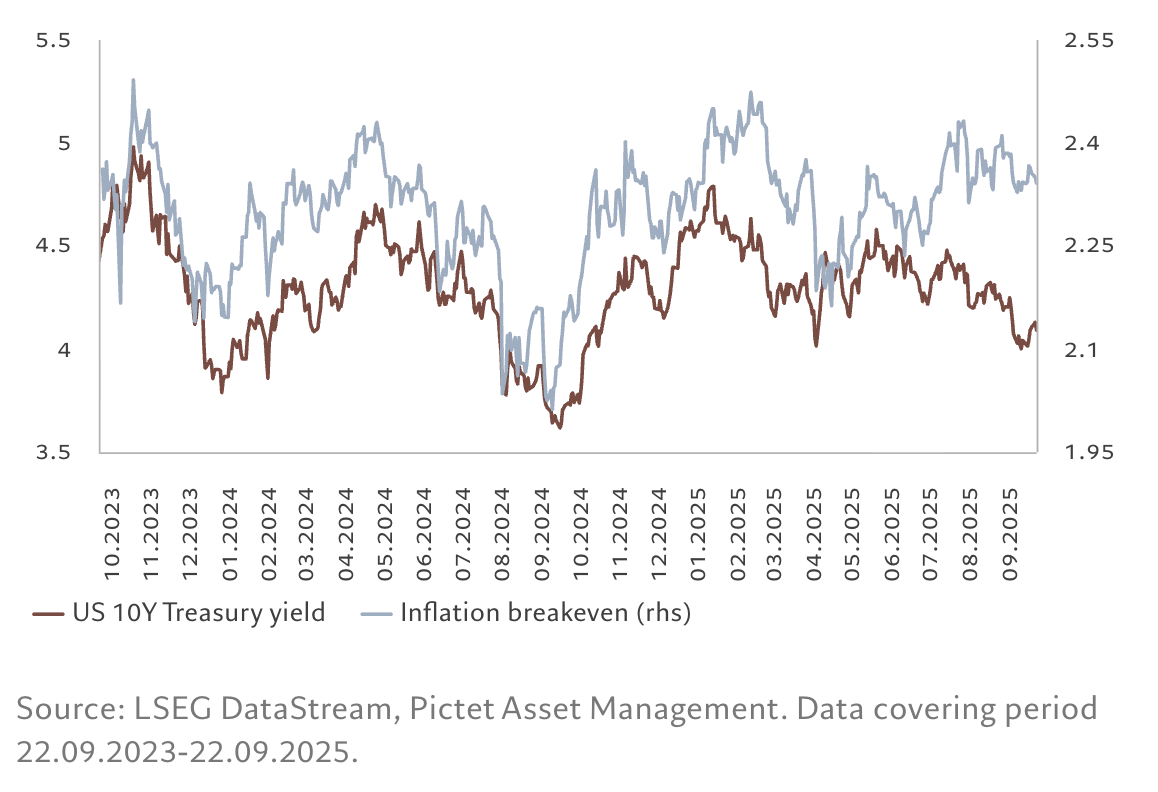

However, we are less optimistic on the other main traditional safe haven asset class – US Treasuries. We believe US bonds are under-pricing inflation risk, with 10-year yields now below our long-term target of 4.25%. Despite signs of reacceleration in core consumer price inflation components and the risk of inflationary pressures from trade tariffs, the market’s inflation expectations, as measured by break-even rates, remain stubbornly low (see Fig. 4).

Fig. 4 - Inflation disconnect

US 10-year Treasury yield versus 10-year breakeven rate (%)

Additionally, risks to Fed independence due to political interference could lead to unorthodox policy shifts, heightening uncertainty in the bond market. The result could be higher term premiums and a steeper yield curve. We therefore stick to a neutral stance on US Treasuries, preferring instead to allocate to other areas of the fixed income market.

Prospects for emerging market (EM) local currency government bonds, for example, are supported by benign domestic fundamentals, cheap currencies, and high relative real rates. We expect the growth gap between the emerging and developed world to widen to 2.7 percentage points next year from 2.4 percentage points this year – a trend which should also support EM corporate debt.

In developed market credit, our preference is for European high yield bonds due to attractive volatility-adjusted yields and a more favourable growth/inflation mix compared to their US peers.

Global markets review: stocks, gold at record highs

World equities gained nearly 4% in September, outperforming bonds as growing investor confidence in the global growth outlook and strong earnings reports, especially from big US tech companies, boosted investment inflows into risky assets.

US stocks added nearly 4% in the month, bringing this year’s gains to 15%. The benchmark S&P 500 index hit record high as investors looked past the likely impact of the US government shutdown and focused on strong growth prospects in AI-related investment.

Dwarfing Wall Street gains were emerging market stocks, which rose more than 7% in local currency terms to be the biggest outperformer of the month. Robust economic growth, stable inflation and supportive monetary policy encouraged investors to allocate to emerging market regions, which also benefit from the prospect of a structural dollar decline. Chinese technology stocks in particular enjoyed exceptional gains of more than 40% this year as the sector benefited from expectations of a home-grown AI boom.

Beyond the IT sector, which rose nearly 8% in September, communications services, consumer discretionary and materials stocks rose around 4-5%. In contrast, staples were the only one in red with a decline of nearly 2%.

In fixed income, emerging markets outperformed again, with emerging market dollar, local currency and corporate bonds all rising more than 1%. Japanese government bonds fell 0.4% as the Bank of Japan looks set to keep raising interest rates.

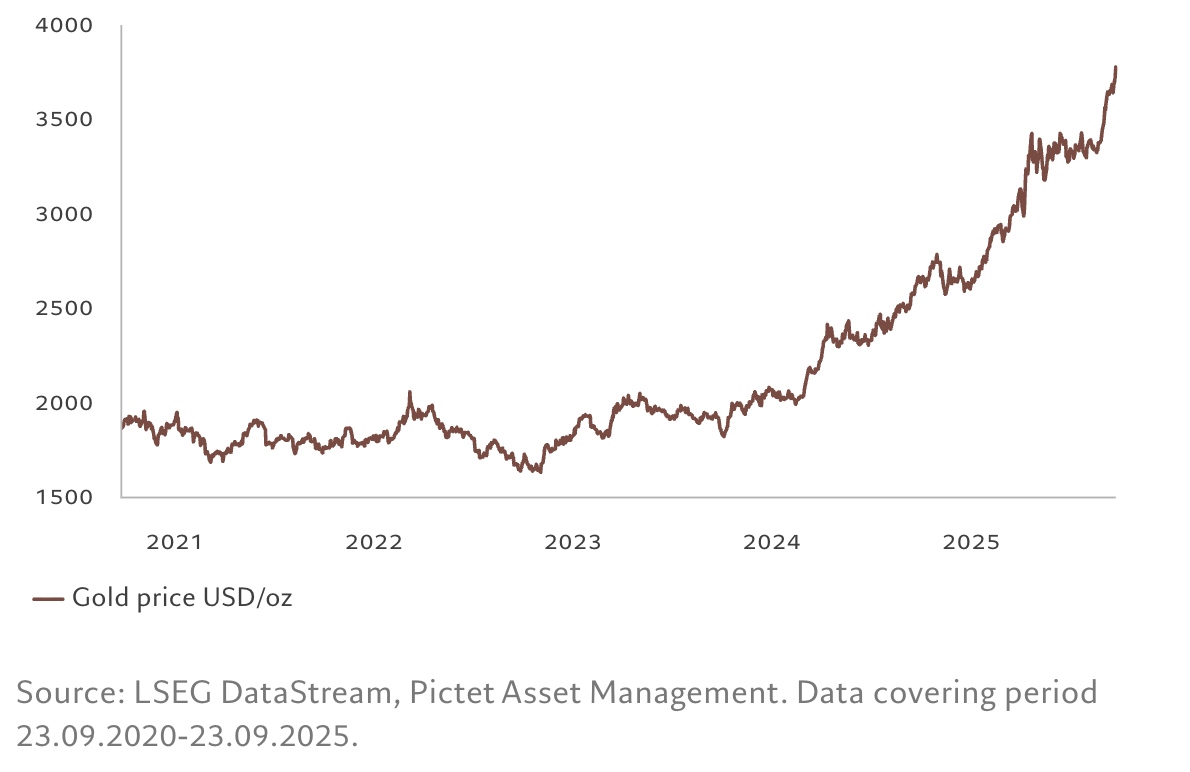

Fig. 5 - Gold: reaching new heights

Gold price (USD/oz)

Gold extended its rally to hit another all-time high in both nominal and real terms, up 40% year to date. Renewed global debt sustainability concerns, a dollar decline stemming from worries over eroding US institutional credibility, and elevated inflationary pressures are contributing to its gains.

Over the past two decades, gold has been the best-performing major asset class, delivering an annualised return of 11%, compared with 9% for equities and 2% or global bonds.

The dollar ended the month unchanged after its decline of nearly 10% in the year.

Information, opinions and estimates contained in this document reflect a judgement at the original date of publication and are subject to risks and uncertainties that could cause actual results to differ materially from those presented herein.

1 Excess liquidity is the difference between the rate of increase in money supply and nominal GDP growth

A message from Advisor Perspectives and VettaFi: Stay ahead of market changes with our daily updates on key market and economic indicators. Visit the AP Charts and Analysis site for our expert insights.

© Pictet Asset Management

Read more commentaries by Pictet Asset Management