Private credit isn’t necessarily new to retail investors. In fact, closed-end funds (CEFs) and business development companies (BDCs) have been giving everyday investors access to private loans and middle-market financing for years (see my previous note here). What is changing now is the scale and accessibility. More well-followed vehicles like ETFs are exploring methods to capture private credit in their wrapper. That includes the latest Simplify VettaFi Private Credit Strategy ETF (PCR).

The Private Credit Advantage

Private credit offers elevated yields, often with strong lender protections. For retail investors and advisors, it is a way to diversify beyond core fixed income and potentially improve the portfolio’s income profile. However, it often comes with potential trade-offs — like illiquidity and credit risk — and the biggest issue: barriers to direct investment.

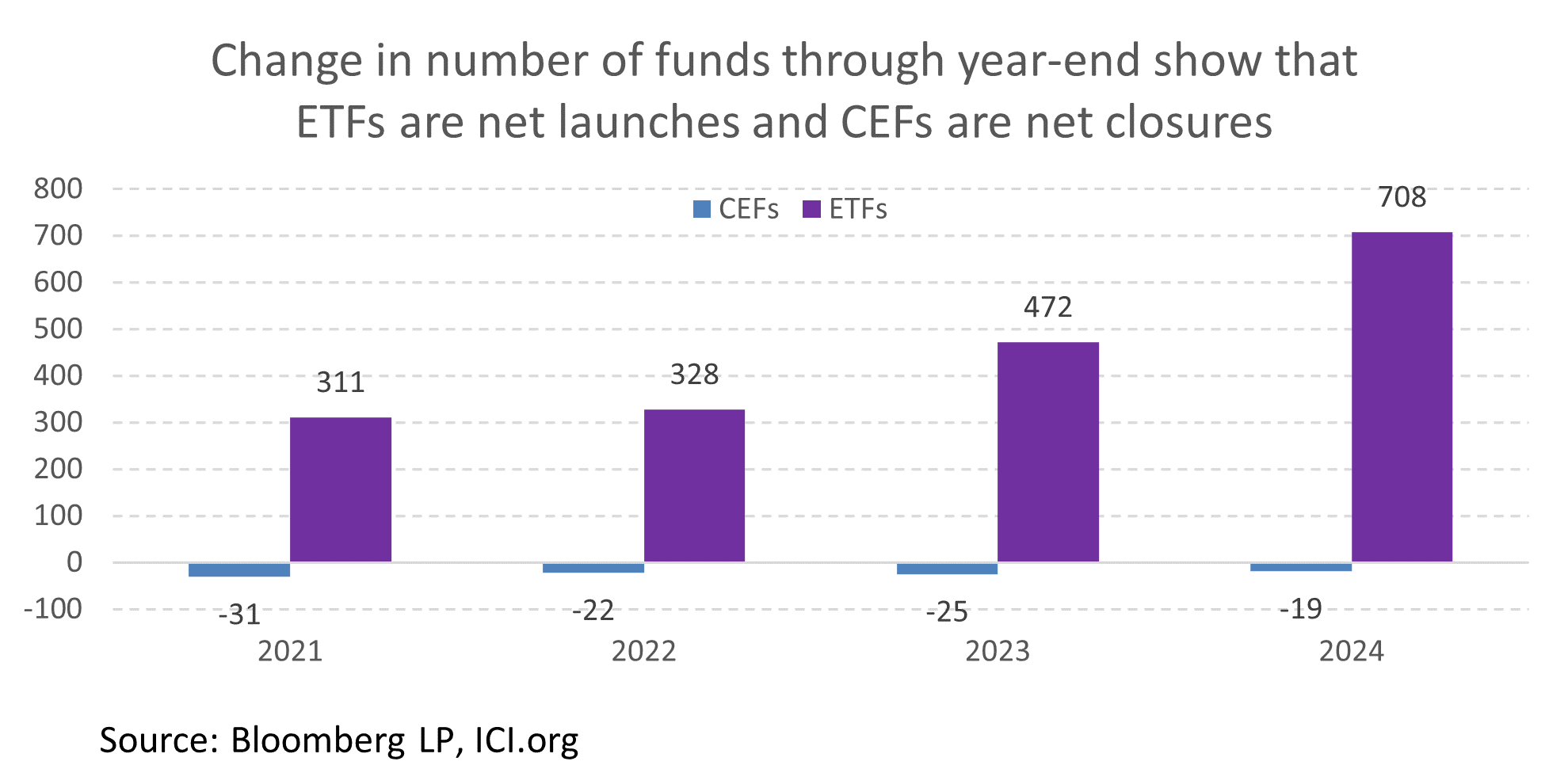

The main issue with ETFs accessing private credit is that ETFs face limits to the amount of private securities they can hold. Open-end funds (including ETFs) have a 15% limit on illiquid investments, according to SEC Rule 22e-4. Most private credit is illiquid and falls under that limit. The constraint ties back to the creation/redemption mechanism that ETFs are well-known for. ETFs must be able to facilitate in-kind creations/redemptions and need proper liquidity. (In contrast, closed-end funds issue a fixed number of shares and do not need to create/redeem daily. Because of this, they have less of a liquidity requirement.)

One approach to get around these limits has been indirect private credit exposure through ETFs that hold publicly traded alternative asset managers such as Blackstone Inc (BX), KKR & Co Inc (KKR), and Ares Management Corp (ARES). These firms generate significant revenue from managing private credit strategies. As such, owning their stock gives investors indirect participation in the growth of private credit markets. The trade-off is that this exposure is tied not only to private credit performance, but also to the broader businesses of these firms. VanEck, for example, offers an ETF that follows this strategy: the VanEck Alternative Asset Manager ETF (GPZ).

Another approach we’ve seen is the State Street/Apollo structure (e.g., the SPDR SSGA IG Public & Private Credit ETF (PRIV) and the State Street Short Duration IG Public & Private Credit ETF (PRSD)), where the ETF includes private credit (alongside public), using liquidity arrangements intended to support creations/redemptions while complying with liquidity rules.

Perhaps a simpler path to private credit is a fund that provides exposure to vehicles best suited for private securities — like CEFs and BDCs — in an ETF wrapper. There are a few existing ETFs of CEFs or ETFs of BDCs. However, the newest ETF from Simplify implements this exposure through swaps.

A New Strategy: The Simplify VettaFi Private Credit Strategy ETF (PCR)

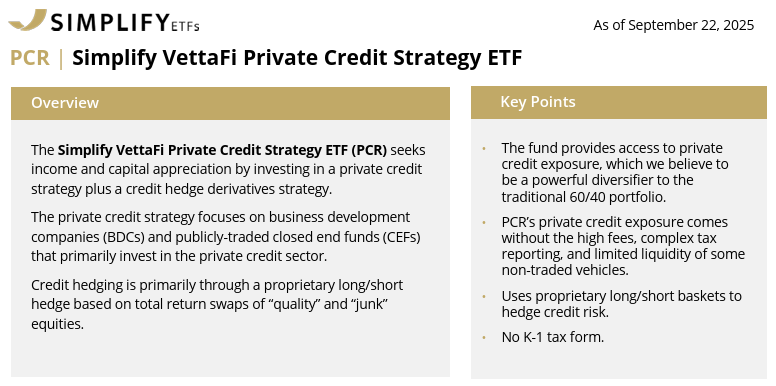

The Simplify VettaFi Private Credit Strategy ETF (PCR) is an actively managed fund seeking income and capital appreciation. It provides exposure to publicly traded BDCs and CEFs which hold private credit (i.e., the BDC or CEF holds over 50% of its portfolio in private credit) through swaps alongside a credit hedge strategy to mitigate adverse credit events. The BDCs and CEFs are selected through the VettaFi Private Credit Index. That index selects and screens based on high distributions and low volatility, along with market-cap and liquidity requirements. These BDCs and CEFs primarily include loan participation CEFs, collateralized loan obligation (CLO) CEFs, and debt-focused BDCs. PCR’s proprietary credit hedging strategy is primarily through a long/short hedge based on total return swaps (i.e., long holdings with high quality metrics and short holdings with low quality metrics).

Why Seek Exposure Through an ETF?

To put it simply, this ETF allows investors to access private credit in familiar way. BDCs and CEFs have been accessing private credit for years. They can do so efficiently because they do not have the same liquidity requirements as ETFs. Packaged exposure through an ETF makes things easier for investors rather than screening BDCs and CEFs on their own.

An investor can invest directly in BDCs and CEFs since they are retail vehicles, but there’s a big caveat. Analyst coverage, media, and even issuer marketing can all lean heavily toward ETF tickers and away from more niche funds like CEFs and BDCs. Growth in the market has been pointing more toward ETFs. Plus, more resources in the space allow the broader group of investors and advisors to follow ETFs more closely than other funds. In contrast, it might be easier for traditional advisors/investors to entrust CEF/BDC selection to an index provider and/or active manager.

Additionally, ETFs like PCR come with added benefits. Those include daily portfolio transparency, in-kind creation/redemption that helps keep prices aligned with NAV, and typically better tax efficiency. CEFs and BDCs, in contrast, can trade at premiums or discounts to NAV. That can be difficult for investors to evaluate and time correctly. Through the ETF wrapper, PCR delivers diversified access to private credit in a structure that is more liquid, visible, and intuitive for most retail investors and advisors.

Also worth noting — because PCR seeks exposure primarily through swaps, its expense ratio (76 basis points) is more aligned with derivatives-based funds. It’s also considerably lower than many true ETFs of CEFs, which have fees in the 200-300 basis points range.

Bottom Line

Private credit demand is real, but selecting individual BDCs and CEFs can be difficult. For income-oriented portfolios, PCR offers a simpler way to gain exposure to the asset class in a familiar ETF wrapper.

Glossary of Fund Terms Used

Closed-end funds (CEFs): A closed-end fund is an investment company that raises a fixed amount of capital in an IPO and then lists its shares on an exchange. Unlike ETFs, investors buy and sell shares in the secondary market. That means the price can trade at a premium or discount to the fund’s underlying net asset value (NAV). CEFs come in three main structures: traditional, tender offer, and interval.

Why are they attractive? Many CEFs use leverage and focus on income-producing assets, which can mean higher yields (but also higher volatility).

Business development companies (BDCs): A business development company provides financing to small and mid-sized private businesses. According to the ICI, they must have at least 70% of their assets in domestic private companies or domestic public companies with market caps of $250 million or less. While BDCs are technically a type of CEF, they are often grouped separately because they are not registered under the 1940 Act (although they still elect to follow certain provisions). BDCs may be listed or unlisted; listed shares can trade on exchanges.

Why are they attractive? Investors get exposure to private equity and credit investments that are normally difficult to access. They also get exposure to typically high dividend yields.

Exchange-traded funds (ETFs): Unlike closed-end funds, ETFs use a creation/redemption mechanism that helps keep their share price very close to the fund’s net asset value (NAV). That reduces the risk of trading at wide premiums or discounts. This terminology can sometimes be confusing because closed-end funds and (many) BDCs also trade on exchanges. However, unlike ETFs — “open-end” funds with daily creation/redemption — CEFs and BDCs issue a fixed share count and are “closed-end.”

Why are they attractive? ETFs are attractive because they offer low costs, daily liquidity, transparency, and tax efficiency. That makes them a straightforward way to access a wide range of strategies.

For more news, information, and analysis visit the Thematic Investing Content Hub.

VettaFi LLC (“VettaFi”) is the index administrator and calculation agent for PCR, for which it receives a fee. However, PCR is not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of PCR.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

More Specialty Investments Topics >