The Federal Reserve is poised to cut interest rates this week, potentially offering some relief to prospective U.S. homebuyers hamstrung by elevated mortgage rates. But rate cuts might not be the Fed’s most direct path to supporting housing. For a more targeted approach, the Fed may just need to rethink its playbook for the mortgage bonds on its balance sheet.

Since 2022, when it started hiking rates, the Fed has also been steadily shrinking its bond holdings. It has allowed principal and interest payments on mortgage-backed securities (MBS) to roll off its balance sheet without reinvestment, a process known as quantitative tightening (QT).

QT is a reversal of the quantitative easing (QE) bond-buying policy the Fed used to support the financial system after the global financial crisis and the pandemic. The Fed bought its first mortgage bond in 2009, so managing its MBS holdings has been an active policy tool for 16 years.

QT can shift the supply–demand balance in the MBS market, with significant knock-on effects for mortgage rates. Agency MBS continue to trade at unusually wide spreads as the Fed passively reduces its holdings and with banks comparatively inactive in the market.

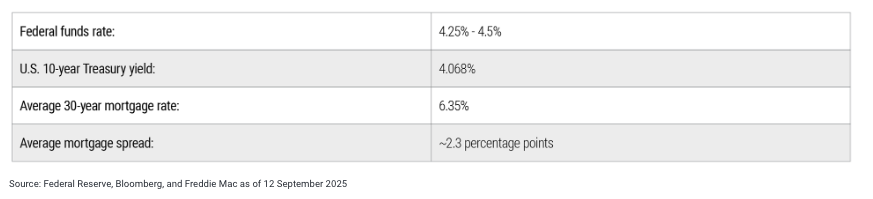

Although the Fed’s policy rate has a broad influence as a borrowing gauge, the 10-year Treasury yield is a more important benchmark for mortgage rates, and that’s set by the bond market. Meanwhile, mortgage spreads – the gap between Treasury yields and mortgage rates (see Figure 1) – are also determined by market forces, and those remain near historically wide levels.

Figure 1: Mortgage rates are well above 10-year Treasury yield

A more direct approach

Wide mortgage spreads present a problem for monetary policy transmission. The Fed’s policy rate may be heading down toward 4%, but mortgage rates remain north of 6%.

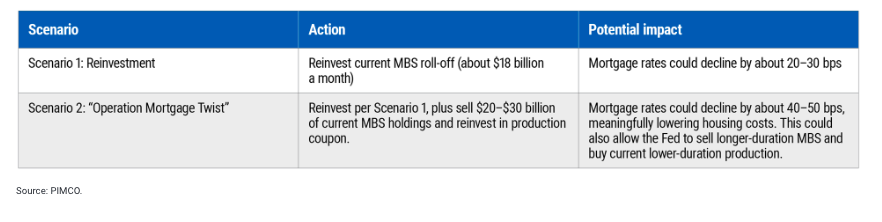

What if the Fed simply stopped shrinking its MBS holdings? Reinvesting the roughly $18 billion in current monthly roll-off into new mortgage securities could compress mortgage spreads by 20 to 30 basis points (bps), in our view. That wouldn’t be restarting QE – it would just keep MBS holdings steady. And it could deliver as much bang for the buck as a 100-bp cut to the federal funds rate, which is what has historically been needed to achieve a similar drop in mortgage rates.

An even more aggressive option: Sell $20–$30 billion of legacy MBS each month and reinvest proceeds into current securities (see Figure 2). We estimate that could push mortgage rates down by 40 to 50 bps.

Figure 2: Fed reinvestment could significantly lower mortgage rates

It could also meaningfully shorten the duration – a gauge of interest-rate risk – of the Fed’s balance sheet. That could be a win for policymakers worried about the effect of elevated federal debts and deficits on U.S. borrowing costs.

Affordability remains challenged

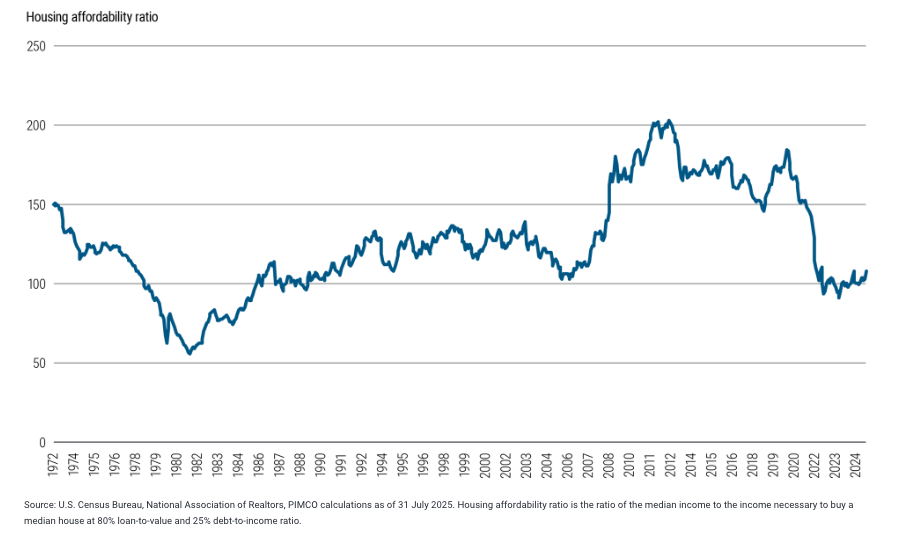

To be sure, ending MBS runoff wouldn’t be a cure-all for the U.S. housing market. Average U.S. home prices have ticked lower in recent months, according to Federal Housing Finance Agency data, but by some measures housing is as unaffordable as it has been in more than three decades (see Figure 3). A lack of inventory could continue to support house prices.

Figure 3: Housing affordability has fallen to the lowest levels in decades

But with officials now looking to reduce interest rates, it’s worth examining the relative effectiveness of the Fed’s monetary tools at transmitting policy into the U.S. economy. In a cycle where interest rate policy is politically fraught and inflation remains sticky, the Fed may find that the most effective easing tool is already hiding in plain sight.

If the Fed continues its current approach, expect mortgage rates to remain elevated through 2026, making homeownership a luxury good reserved for the wealthy. The question isn't whether Fed officials can improve this situation – it's whether they will.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Past performance is not a guarantee or a reliable indicator of future results.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. References to Agency and non-agency mortgage-backed securities refer to mortgages issued in the United States.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

It is not possible to invest directly in an unmanaged index.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

© PIMCO

Read more commentaries by PIMCO