A key theme dominating global financial markets in recent weeks has been the general upward pressure on sovereign bond yields, particularly at the long end of government bond market curves. This move reflects a complex interplay of macroeconomic factors, but increasingly, political instability is emerging as a driver — most notably in Japan and France, where recent leadership shakeups have introduced fresh uncertainty into the policy outlook and fiscal trajectory.

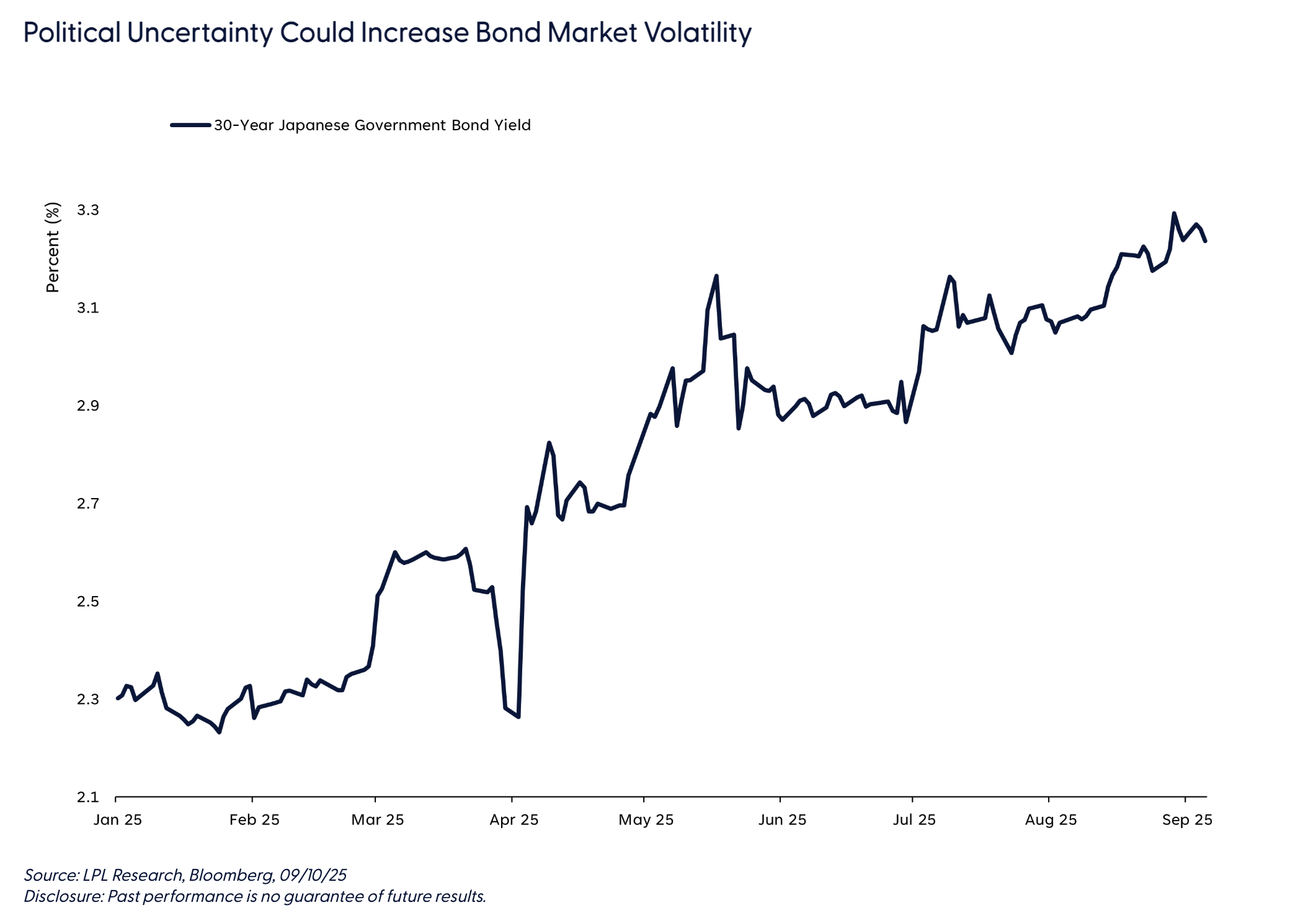

In Japan, the political landscape was rattled over the weekend when Prime Minister Shigeru Ishiba announced his resignation. His departure has triggered a leadership contest within the ruling Liberal Democratic Party (LDP), with internal elections anticipated to take place on October 4. However, the implications extend beyond party politics. The incoming LDP leader will need to secure a majority in the lower house of the Japanese Diet to form a stable government. The new prime minister would then need to either form a broad coalition or call snap elections. The LDP is generally considered the more long-term rates-friendly party by the markets, so failure to form a government could usher in a period of heightened political uncertainty, undermining investor confidence and amplifying volatility in Japanese government bonds. The Bank of Japan, already navigating a complex policy environment with inflation at the highest levels in the developed world, could also be forced into a bit of a holding pattern until greater political certainty is achieved.

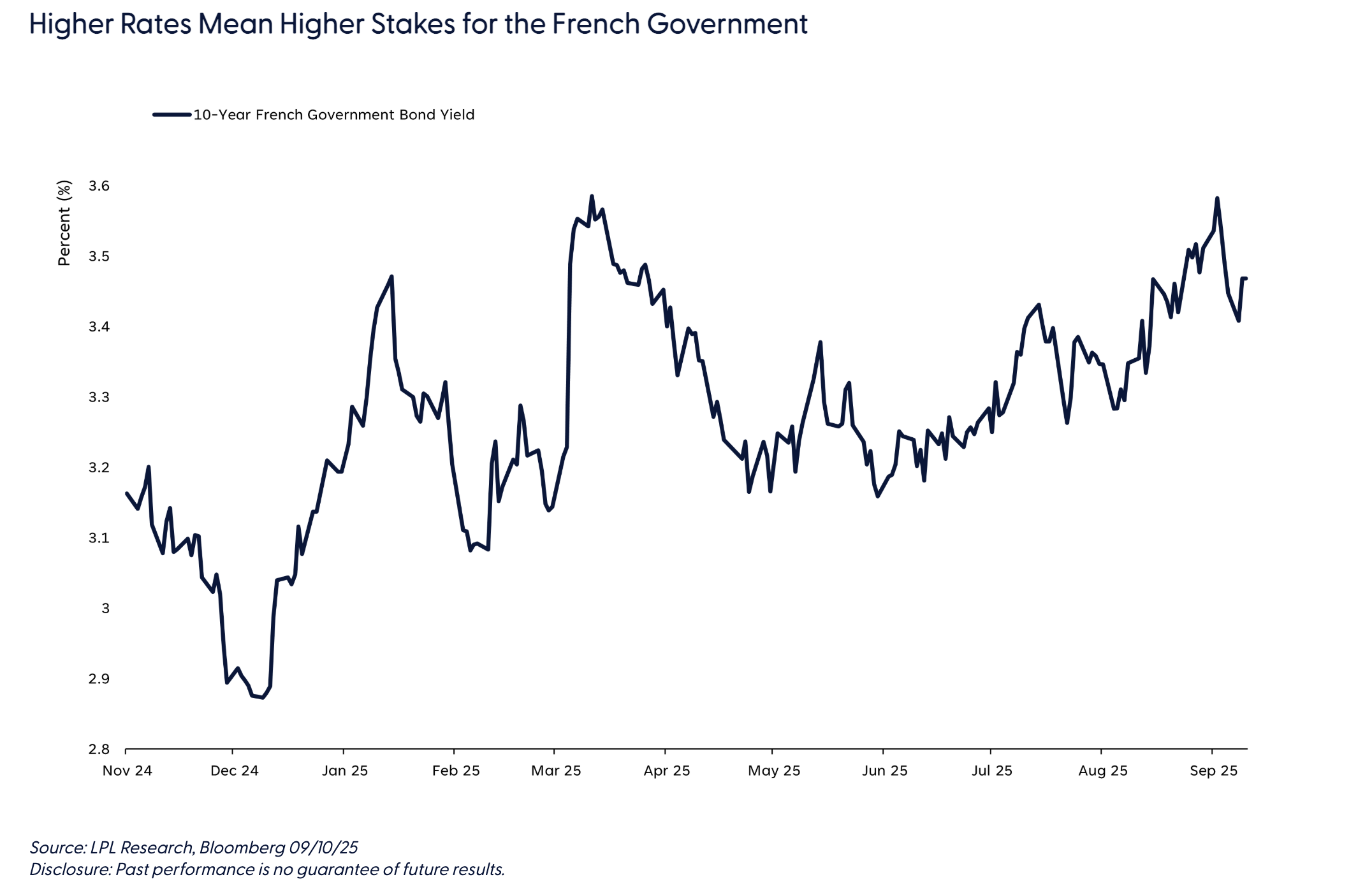

Meanwhile, in France, political tensions have also escalated. On Monday, François Bayrou lost a critical vote of no confidence and stepped down as prime minister after his government’s proposed austerity budget failed to gain sufficient support in the National Assembly. French President Emmanuel Macron has since appointed Defense Minister Sebastien Lecornu to become the new prime minister. This new appointment avoids snap elections, but it remains to be seen whether the incoming leader will be able to form a viable coalition capable of governing effectively. Odds in the betting markets of new elections before the end of the year are still around 35%.

The stakes are high. France is grappling with a €3 trillion debt burden, and the cost of servicing that debt amid higher interest rates. Under European Union (EU) rules, they need to reduce their deficit to 4.6% by 2026. Political fragmentation and policy paralysis could severely hinder efforts to implement credible fiscal consolidation. Should markets begin to perceive that political dysfunction is impeding necessary reforms, the risk of a sovereign credit rating downgrade becomes very real — potentially exacerbating the sell-off in French government bonds and further spread widening.

Conclusion

Taken together, these developments underscore how political risk is once again becoming a key driver of market dynamics. Investors are increasingly demanding higher term premiums to hold long-dated government debt in jurisdictions where political uncertainty threatens to derail fiscal discipline and economic stability. While inflation dynamics and central bank policy remain important, the recent move higher in yields in Japan and France underscores the budding influence of governance risk in shaping global fixed income markets.

The LPL Research Strategic and Tactical Asset Allocation Committee (STAAC) holds a neutral weight in core bonds, with a slight preference for mortgage-backed securities (MBS) over investment-grade corporates. The Committee believes the risk-reward for core bond sectors (U.S. Treasury, agency MBS, investment-grade corporates) is more attractive than plus sectors. The Committee does not believe adding duration (interest rate sensitivity) at current levels is attractive and remains neutral relative to benchmarks.

Kristian Kerr drives the broad, house investment strategy for LPL Financial Research. His career includes over 25 years of industry experience.

A message from Advisor Perspectives and VettaFi: Interested in learning more about how bond ETFs can help diversify your portfolio? Click here to read more.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #795442

Read more commentaries by LPL Financial