The financial world is replete with terms and definitions, many of which overlap in concept or application. Perhaps I can simplify a familiar concept for most investors who strive to grow and preserve their wealth. Sometimes, these two goals overlap, and at other times, they represent two distinct ideas that require two different portfolio strategies. When broken down, neither concept is complex, yet the variables that can affect them may create challenges.

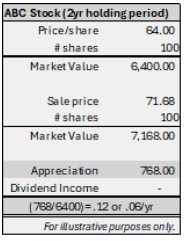

How do we grow our wealth? Total return is a term used to describe the earnings generated from an investment. The total return is intended to encompass all sources of return, including asset appreciation and income earned from dividends, interest, or other distributions. Using stock ABC as an example, an investor wants to see its price appreciate. For illustrative purposes, if an investor purchases ABC stock for $64 and sells it two years later at $71.68, they have accumulated $7.68 in appreciation per share over the two-year period. This represents an annualized total return of 6.0% [(7.68/64.00)/2(yrs)]. The growth in this asset occurred 100% through price appreciation. Some stocks pay dividends. If this stock paid a dividend, we would add the dividend income earned to the appreciation and divide that by the initial investment to calculate the total return. In practice, most of the return earned from stocks is in the form of appreciation. It is not guaranteed, but its potential is analyzed based on a company's potential growth, profitability, and current market price. Stocks are considered to have more risk due to unknown factors, but also have the potential for higher total returns. Stocks, including those that have dividends, are typically considered growth assets and may not be suitable substitutes for preservation assets.

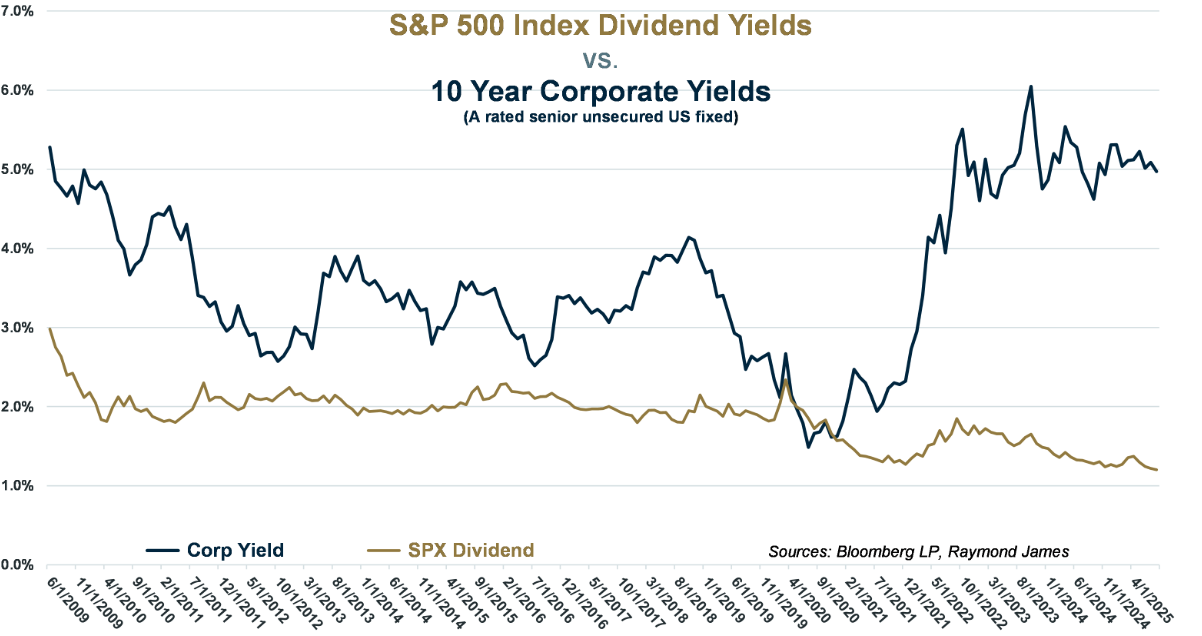

There have been very few moments in time when dividends have been higher than yields on 10-year corporate bonds (protective assets). That gets amplified in an environment of elevated interest rates, much like we have experienced over the last two years as the spread between the two has widened.

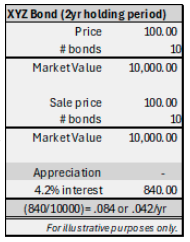

Individual bonds are a good representative of assets that help preserve wealth. Whereas the total return of most stocks is primarily derived through price appreciation, the total return earned on an individual bond is based primarily on the interest earned.

Bonds are usually issued in $1,000 increments, so holding 10 bonds at par or a price of $100 is a market value of $10,000. The cost of a bond can fluctuate with changes in the market; however, when it matures, it is typically at par, or a price of $100. In this illustration, 10 bonds were held for two years until they matured. The total return had no appreciation but earned 4.2% interest each year, resulting in an annualized total return of 4.2%.

Barring a default, which is possible but highly unlikely when investing in high-quality investment-grade individual bonds, a bond held to maturity has a known total return from the moment it is purchased. This is known because an individual bond has a redemption date, a feature not available in many other investment products, including funds that invest in bonds.

The notable differences between stocks and bonds are one reason they complement each other so well. Stocks offer the potential for unlimited growth but also carry the risk of potential losses. Bonds, when held to maturity, may help preserve capital with a known income stream and a predetermined date when their face value is returned. When properly allocated, growth assets and wealth preservation assets can form a formidable investment portfolio strategy. In the current elevated interest rate environment, individual bonds are providing a timely dual benefit of wealth preservation and income. Locking into individual bonds for a more extended period can yield investors a known return.