Revisiting Value

It’s become something of a parlor joke in certain circles to ask: “Is value investing dead?” After this week, a better question might be, “Has the death of value been greatly exaggerated?” (with a hat tip to Mark Twain).

Since the global financial crisis, value investing has been a lonely grind. Yet I know several managers who never gave up on value, and others who are uncomfortable with tech valuations and have been reallocating to lower P/E stocks. Now we have the talking heads of traditional financial media shouting, “Value is making a comeback!”

It’s worth asking: What happened to value over the past decade? Why could now be different? And where should we focus if we want to capitalize on a changing market?

A Rough Decade for Value

Value investing—buying shares seemingly undervalued by the market—once seemed unassailable. Legendary investors like Warren Buffett never deviated from their value bend. Yet, for nearly 30 years and especially since 2008, value has underperformed growth stocks, barring a brief post-dotcom resurgence. Why?

First, several sectors known for value, like banking, retail, insurance, and utilities, generated low returns and had weak balance sheets following the financial crisis. These companies couldn’t produce the rates of profit growth you’d see in technology. They lacked the means to invest in R&D, brand-building, and tech upgrades, making it hard to break their low-valuation cycle. They became “value traps.”

Second, the mean reversion that value investors expect from seemingly cheap stocks didn’t happen, or it took a lot longer than expected. Cheap stocks stayed cheap.

Indexing played a role. As ETFs and index investing grow, more capital is passively allocated to the big, expensive stocks that dominate today’s market. Reuters recently reported that nearly 60% of the US stock market is held in passive funds.

Don’t forget rates—big growth companies feasted on low interest rates, furthering their advantage in the markets.

Why value now?

So, why the renewed optimism for value investing? Perhaps there is a style box rotation underway—one that benefits small caps and value. What would cause a rotation? I’ll give you a few possibilities.

Higher interest rates and inflation are making value more attractive. Companies that generate profits and are less reliant on debt should do well if rates and inflation remain close to present levels.

Are large-cap valuations stretched? It’s hard to imagine money flowing out of the S&P 500. Ed Yardeni reported this week that foreigners continue to buy US equities, with net inflows at a record high for the past 12 months through June. Still, imbalances tend to self-correct. The S&P 500 is concentrated. The “Mag 7” stocks make up approximately 34% of the index. Ten years ago, they made up roughly 12%.

Then there is market valuation. The Mag 7 stocks have an average price-to-earnings ratio of roughly 28. The S&P 500’s forward P/E is around 22. Compare that to IJS, which is iShare’s S&P Small Cap 600 Value ETF, with a P/E of just under 15. Still not cheap, but cheaper.

Finally, there is the economic cycle. If the economic cycle still exists—a big “if”—then we may be close to a cycle’s end. That would indicate a good setup for value stocks, which tend to do better in the later stages of an economic cycle. That’s when old-fashioned metrics like cash flow, profits, and balance sheet strength matter.

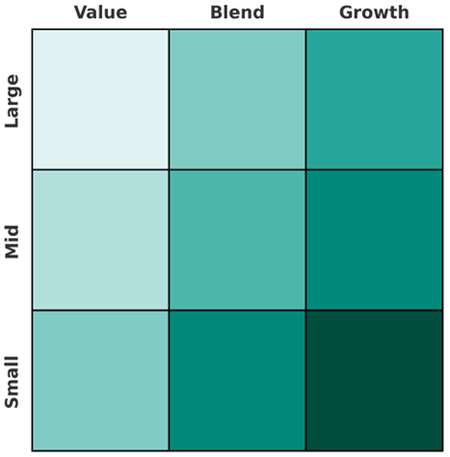

What’s a Style Box?

Morningstar coined the phrase as a way to visualize investment asset allocation. With stocks, a style box looks like a nine-square grid, with small-, medium-, and large-cap stocks from the bottom up on the Y axis, and value, blend, and growth stocks from left to right on the X axis. Here’s a picture:

Simply put, a rotation happens when capital moves from one box to another. My good friend Jared Dillian (former head of ETF trading at Lehman) told me months ago to get ready for a style box rotation. He and I discussed this while together recently in Nashville. You can see the conversation here:

You can find a transcript of our conversation here.

Jared and his longtime analyst, Adam Crawford, just launched a small-cap value letter at his research firm, Jared Dillian Money (full disclosure: I am an investor in this entity). The letter is not core to our conversation, but if you are interested in the service, there’s a link on the video page.

Where to look?

It’s hard to be a value investor today, for a new reason—it’s hard to find a cheap stock that offers value.

Some sectors where there might be opportunities include regional banks, energy, healthcare, and select industrials, but here’s where expertise comes into play. Passive investing in value can be tricky, and buying a blob of small caps typically will get you the good with the bad companies. There are niche ETFs, to be sure. If we are on the cusp of a style box rotation, stock picking could once again be a valued skill set.

Thanks for reading.

Ed D’Agostino

Publisher & COO

Prepare your bond portfolio for changing market conditions. Register today for the Fixed Income Symposium on Sept. 18, 2025, 11AM ET / 8AM PT.

© Mauldin Economics

Read more commentaries by Mauldin Economics