Summary

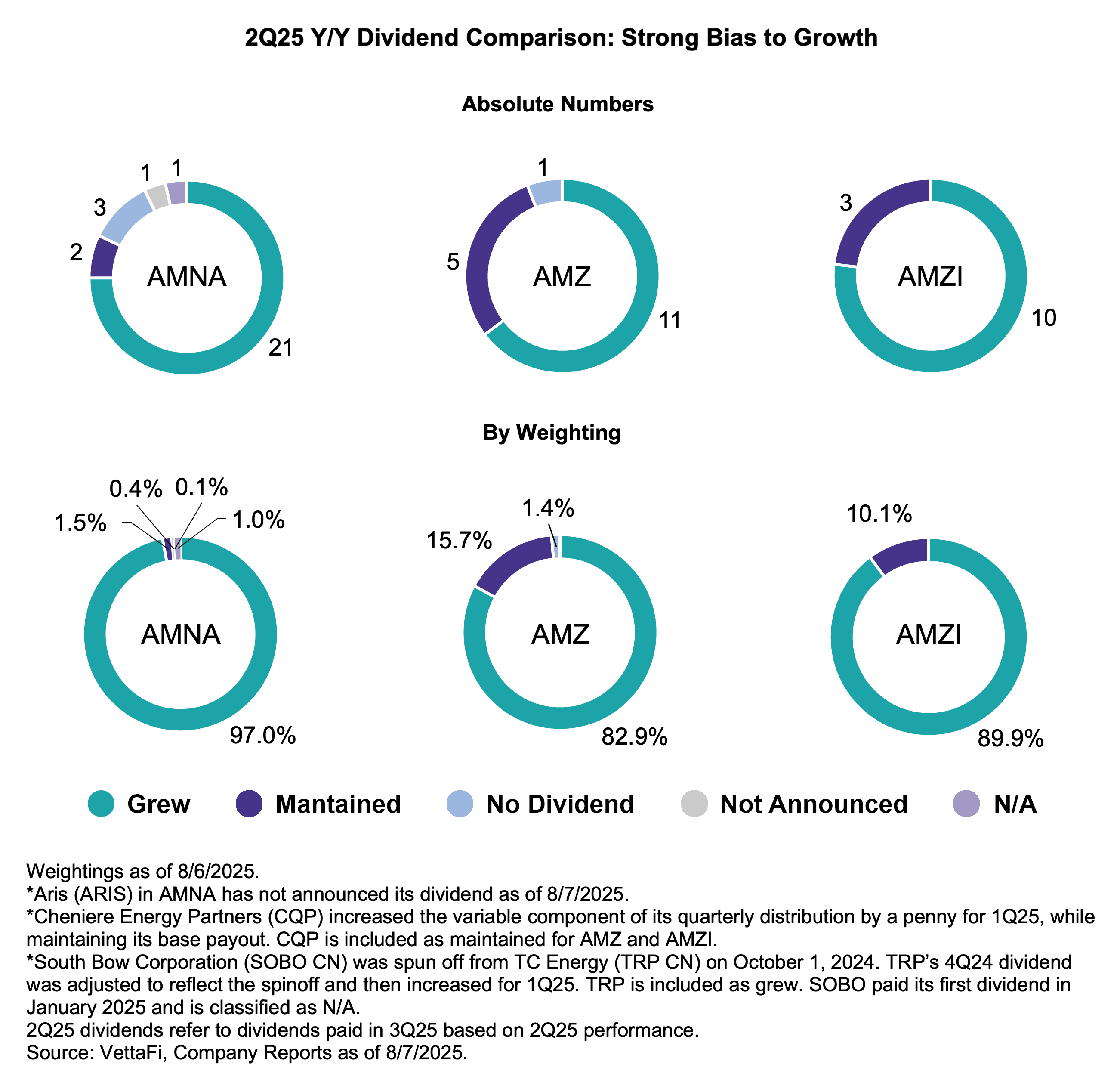

- On a year-over-year basis, 97.0% of the Alerian Midstream Energy Index (AMNA) by weighting has grown their dividends.

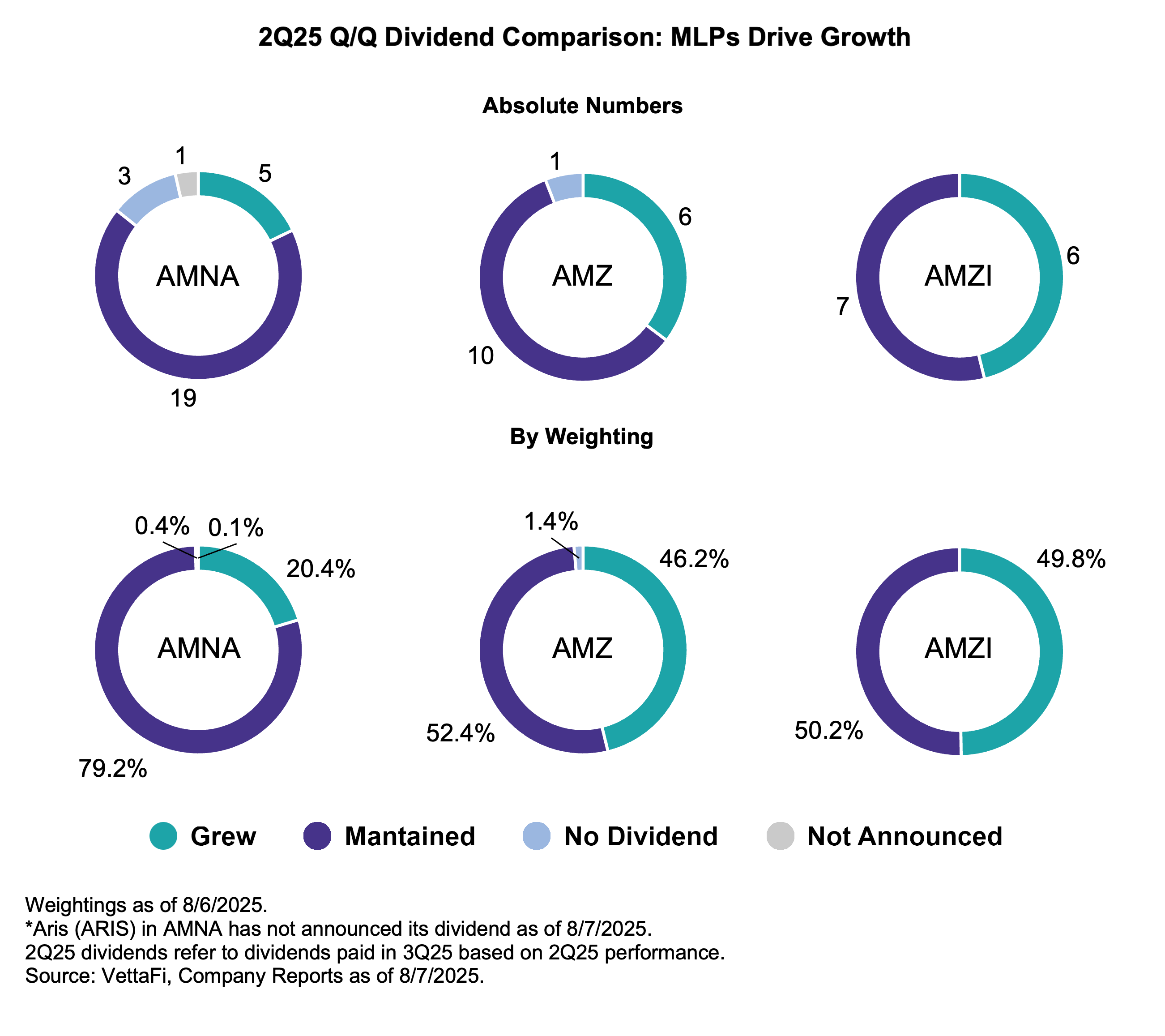

- MLPs largely drove sequential growth in payouts for 2Q25, while nearly all corporations are keeping their dividends steady. No AMNA constituent has cut its regular dividend since July 2021.

- Dividend growth continues to enhance already compelling midstream yields, and more dividend increases are expected for 3Q25.

For the second quarter of 2025, most energy infrastructure companies maintained their payouts, with MLPs largely providing sequential growth. However, the vast majority of midstream companies have increased their dividends within the last year. More growth is in store for 3Q25. Importantly, it has now been more than four years since there was a cut to regular dividends for a constituent of the broad Alerian Midstream Energy Index (AMNA). This note recaps 2Q25 MLP/midstream dividends, examines current yields, and previews anticipated dividend hikes for 3Q25.

2Q25 Payouts: MLPs deliver on growth.

Looking at sequential dividend increases, growth mainly came from the MLPs that typically grow their distributions each quarter. The majority of midstream names announce an increase once a year, and that often coincides with 4Q or 1Q announcements. In other words, 2Q25 was fairly quiet in terms of dividend increases, but that is typical of the second quarter.

Among corporations, Canadian C-Corp Keyera (KEY CN) increased its dividend by 3.8%. Bellwether MLP Enterprise Products Partners (EPD) raised its quarterly payout by a penny to $0.545/unit, representing a 1.9% increase. Hess Midstream (HESM) increased its distribution by 3.8%. While HESM has typically increased its payout each quarter, this marks a larger percentage increase than recent hikes.

The remaining sequential increases came from MLPs Energy Transfer (ET), Sunoco (SUN), Global Partners (GLP), and Delek Logistics Partners (DKL). One name in AMNA, Aris Water Solutions (ARIS), had not announced its payout at the time of writing but had increased its dividend earlier this year. Notably, Western Midstream (WES) announced the acquisition of ARIS last week.

The pie charts below show quarter-over-quarter changes to dividends for AMNA, the Alerian MLP Index (AMZ), and the Alerian MLP Infrastructure Index (AMZI) by comparing 2Q25 payouts to those made for 1Q25. To be clear, 2Q25 dividends refer to dividends paid in 3Q25 based on operational performance in 2Q25.

Year-over-year comparison spotlights bias to growth.

With only a handful of names raising their payouts sequentially, a year-over-year comparison can provide a clearer picture of dividend trends. The chart below shows a pronounced bias toward rising payouts. More than 80% of AMZ and almost 90% of AMZI by weighting as of August 6 have increased their dividends within the last year. For AMNA, 97.0% of the index by weighting has grown payouts in the last year. Looking at absolute numbers, the majority of constituents in each index have grown their dividends.

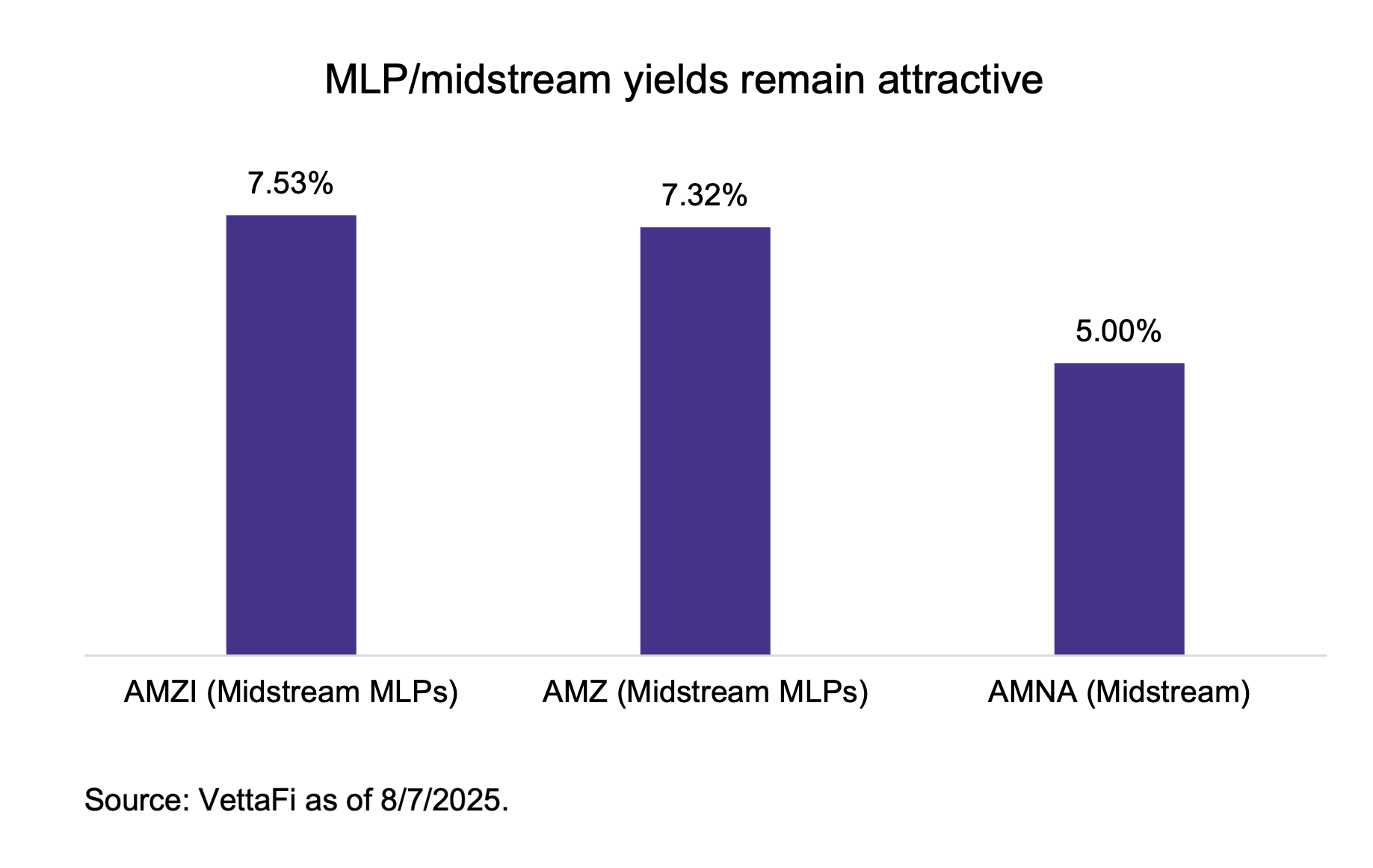

MLP/midstream yields remain attractive, with more dividend growth on the horizon.

Dividend growth enhances already attractive yields for MLPs and midstream corporations. As shown below, AMZI was yielding 7.53% as of August 7, which is slightly above its three-year average yield of 7.43%. MLP yields remain particularly attractive for income-seeking investors. More broadly, income can be beneficial in volatile equity and energy markets as seen so far this year.

Looking ahead to 3Q25 dividend announcements, more growth is anticipated. In June, C-Corp Cheniere Energy (LNG) announced plans to increase its dividend for 3Q25 by 11%. On its recent earnings call, management of MLP MPLX (MPLX) reiterated that its business can support 12.5% annual distribution growth. In recent years, MPLX has increased its distribution with the 3Q25 payout and increased by 12.5% last year.

Bottom Line

While the energy market and broader equities have seen volatility this year, MLPs/midstream continue to execute well on dividend growth. Strong dividend growth trends add important context to generous yields. Dividend growth is also being complemented by equity repurchases, which will be discussed in detail next week. Stay tuned.

Register today for our 60-minute webcast, “Checking MLP/Midstream Fundamentals as 2026 Approaches” on Wednesday, September 3, at 2 p.m. ET. CE credit will be available.

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMZ is the underlying index for the JPMCFC Alerian MLP Index ETN (AMJB), the ETRACS Alerian MLP Index ETN Series B (AMUB), and the ETRACS Quarterly Pay 1.5x Leveraged Alerian MLP Index ETN (MLPR).

Related Research:

MLPs/Midstream 1Q25 Dividend Growth Unfazed by Volatility

Examining 2024 Midstream/MLP Dividend Coverage

Delving Into MLP/Midstream Total Shareholder Yield

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMJB, AMUB, MLPR, AMLP, and MLPB, for which it receives an index licensing fee. However, AMJB, AMUB, MLPR, AMLP, and MLPB are not issued, sponsored, endorsed or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing or trading of AMJB, AMUB, MLPR, AMLP, and MLPB.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more commentaries by VettaFi