Volatility across major asset classes is currently sitting at unusually low levels. While volatility is often viewed as a broad measure of risk in financial markets, its role has evolved significantly in recent years. It’s no longer just a conceptual tool used to describe uncertainty or instability. In today’s financial ecosystem, volatility has become a core component of market structure — a directly tradable instrument that influences everything from portfolio construction to asset pricing. Quantitative strategies increasingly rely on volatility as a foundational input, while entire product suites — from vanilla ETFs to exotic options — are designed specifically to track and allow for speculation on its movements. As a result, when volatility reaches extremes, it doesn’t just reflect market sentiment; it actively shapes it. These shifts can have wide-reaching implications across asset classes, liquidity conditions, and investor behavior.

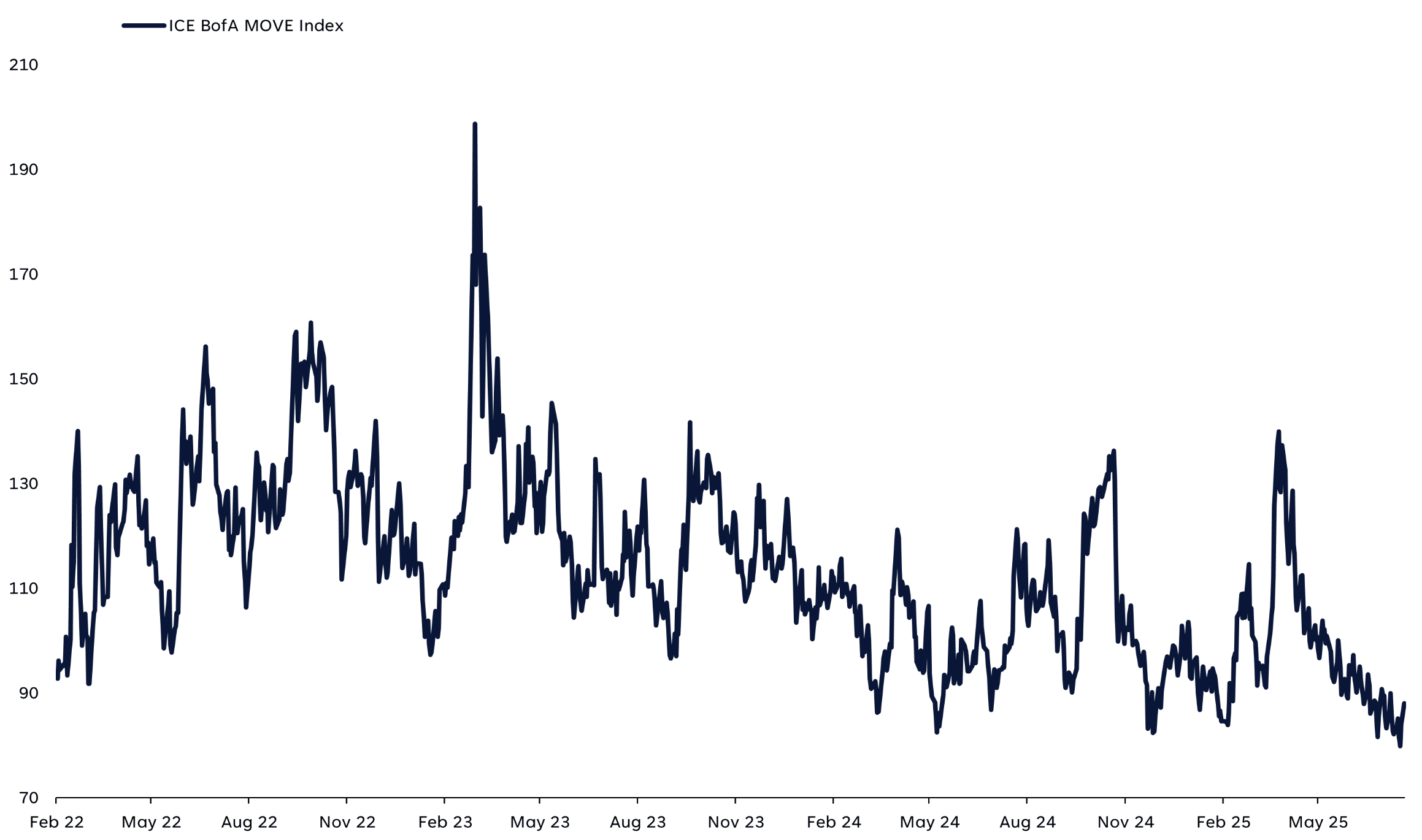

After a historic surge in volatility around the April 2 tariff announcement and subsequent uncertainty, markets have undergone a dramatic reset. Over the past few months, volatility has not just declined — it has pretty much collapsed. Consider the ICE BofA MOVE Index, which measures bond market volatility: it fell to its lowest level in over three years last week. In foreign exchange markets, the Deutsche Bank Currency Volatility Indicator (CVIX Index) — a gauge of volatility in the major currencies — dropped to its lowest level in nearly a year. Equities have also followed suit, with one-month realized volatility in some of the indexes falling to levels not seen since June of last year.

Source: LPL Research, Bloomberg 08/05/25

This widespread decline in volatility is notable as volatility tends to be mean-reverting, meaning periods of extreme calm are often followed by sharp reversals, and vice versa. This happens when investors extrapolate current conditions too far into the future — assuming that quiet markets will remain quiet, or that turbulent ones will stay chaotic. This behavioral tendency leaves markets vulnerable to surprise, especially when complacency sets in. History is replete with examples of this dynamic. When volatility is low, investors often take on more risk, reduce hedges, and stretch for yield — all under the assumption that calm will persist. But when volatility inevitably returns, it tends to do so abruptly, catching markets off guard and triggering rapid repositioning.

With volatility now at depressed levels and markets entering the seasonally challenging August-to-October window — a period historically associated with heightened uncertainty — investors should be prepared for a potential uptick in volatility. The possible catalyst for any renewed volatility is difficult to predict. It could stem from geopolitical developments, macroeconomic surprises, policy shifts, or even technical factors within the market itself. But whatever the case, the conditions seem ripe: depressed volatility, stretched positioning/sentiment, and a time of year that has often delivered surprises.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #779234

Disclosures: All indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

Read more commentaries by LPL Financial