Still Special?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe United States has been on a remarkable run: exceptional growth and innovation, multiple structural advantages, and the financial market dominance to match. Yet this year there’s been increased murmuring regarding the feasibility of continued U.S. exceptionalism, as several economic challenges seem to lurk. Given that U.S. assets form the core of most global portfolios, this uncertainty has naturally led to questions regarding asset allocation.

In our view, the U.S. is still special and rightly at the center of credit portfolios; however, the option for global diversification remains valuable, providing the requisite asset availability and manager capability exists. The U.S. has the deepest, most liquid capital markets in the world, particularly in the sub-investment grade credit space, allowing managers to deploy capital at significant scale. That’s not to say investors should ignore compelling opportunities in other regions such as Europe and Asia: casting a broad net can only help in identifying the assets offering the best risk/reward balance.

If the massive advantage of the U.S. were to diminish, we believe it would be a larger headwind for equities than credit. With the S&P 500 at record-high levels, equity prices are predicated on continued growth and the willingness of investors to keep paying a significant premium for U.S. equities. Credit spreads appear on the tight side, but credit returns aren’t reliant on exceptional U.S. economic growth and innovation: these companies just need to survive for investors to get their (currently elevated) contractual income.

Foundations of Exceptionalism

The much-discussed U.S. exceptionalism is legitimately… exceptional. A country with less than 5% of the world’s population represents around 65% of some global equity indexes!1 From the lows of the Global Financial Crisis, the U.S. has staged an equity market boom as public equities set new highs and private equity expanded dramatically. Accompanying this rise has been unprecedented debt issuance across the leveraged finance markets, with the notable rise of private credit to a mainstream asset class.

So why has the U.S. been such a consistent growth story? Here’s just a few reasons:

- The U.S. dollar has long been the undisputed global reserve currency, leading to the consistent foreign demand for dollars that helps (a) compress borrowing costs on dollar-denominated debt and (b) permit significant budget deficits.

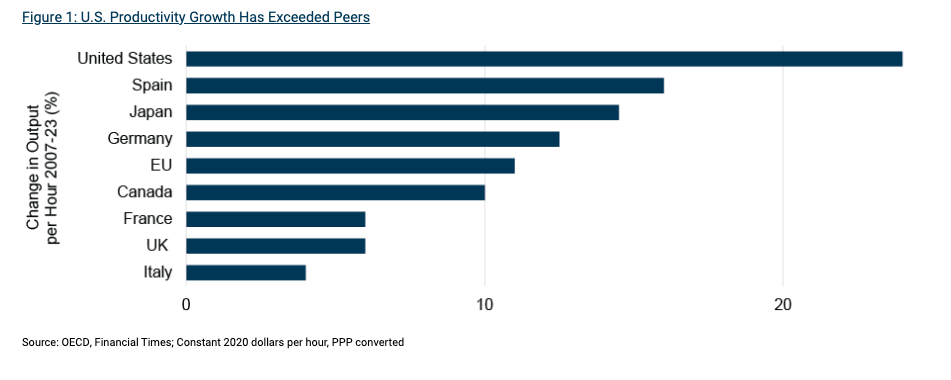

- The U.S. has been a consistent leader in labor productivity, benefiting from a talented workforce, culture of entrepreneurship, and high levels of technology adoption. (See Figure 1.)

- The U.S. has the most accommodative capital markets in the world, from venture funding for future unicorns to senior loans for jumbo-sized LBOs, providing the capital for U.S.-based businesses to rapidly scale. Meanwhile, the U.S. Federal Reserve has supported growth in a manner distinct to more conservative central banks.

Exceptionalism Questioned

Meanwhile, those who question U.S. exceptionalism have identified a few key threats to the country’s dominance, such as a weakened U.S. dollar. It’s hard to ignore that the dollar just experienced its worst first half of the year since 1973.2 This may raise import costs and thus contribute to inflation, while such a precipitous sell-off could also reduce the status of the U.S. dollar as a haven for investors. However, although losing the benefits of being the primary global currency would be significant, it’s hard to envision another currency taking over the status of number one in the world. The U.S. dollar is involved in an extraordinary 88% of foreign exchange transactions and constitutes around 60% of global foreign exchange reserves, with no other currency coming close.3

Additional macroeconomic headwinds may include:

- A stretched low-income consumer, as the U.S. economy bifurcates into a relatively small cohort of very wealthy individuals and an inflation-pressured regular consumer. While an increase in real estate values may make home-owners wealthy ‘‘on paper,’’ this wealth is locked up and may not support the consumption the U.S. economy relies on.

- Elevated national debt as a result of consistent reliance on budget deficits, even in healthy economic environments, including a $1.8 trillion deficit in 2024.4 This leads to an increasing interest bill that diverts government spending away from more productive uses.

- Increased global competition, as other nations rapidly modernize and attempt to catch up with American technological superiority.

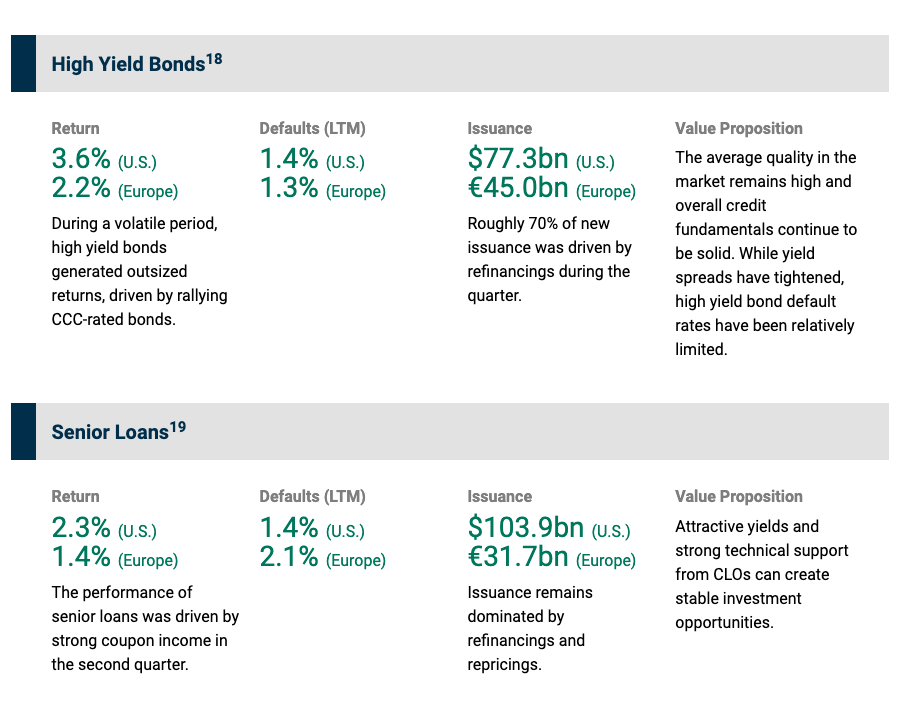

Some of these challenges may turn out to be more speculative discourse than eventual reality. The U.S. economy appears in good health and continues to power through potential challenges. That being said, macroeconomic outcomes are impossible to predict: for investors, regardless of geography, it remains a case of prioritizing fundamental selection, with a focus on risk management and close monitoring for potential signs of deterioration.

Limited Alternatives

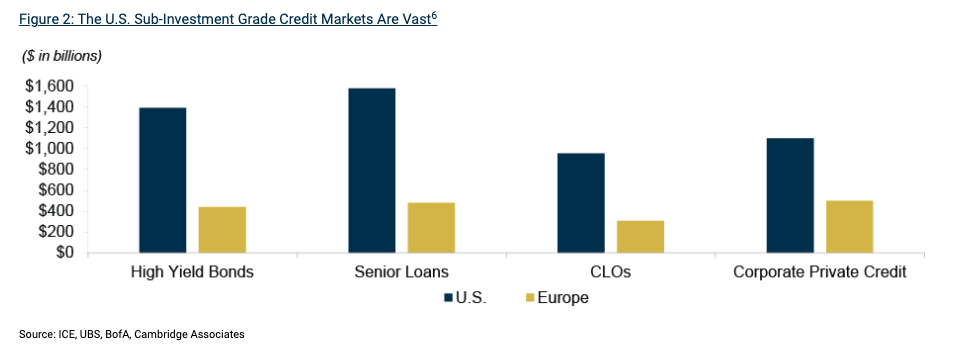

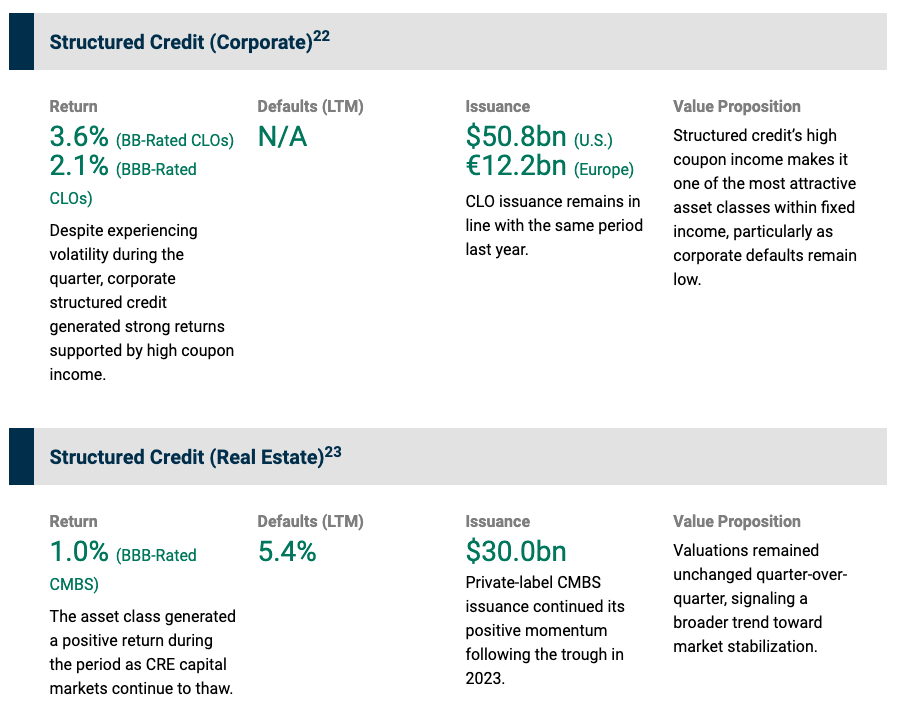

Potential macroeconomic challenges may loom, but the reality is for some asset classes, there is simply limited alternative to U.S. exposure. For alternative credit investors, there is no market outside the U.S. that offers comparable depth. The U.S. high yield bond and senior loan markets combine to nearly $3 trillion, with structured and private credit markets also remarkably extensive.5 (See Figure 2.) This is generally significantly more than other regions; for example, the U.S. high yield bond is around triple the size of the European market. Market environments fluctuate but managers can generally expect to rapidly put money to work in the U.S. leveraged finance markets and begin earning their coupons.

Broader Opportunities

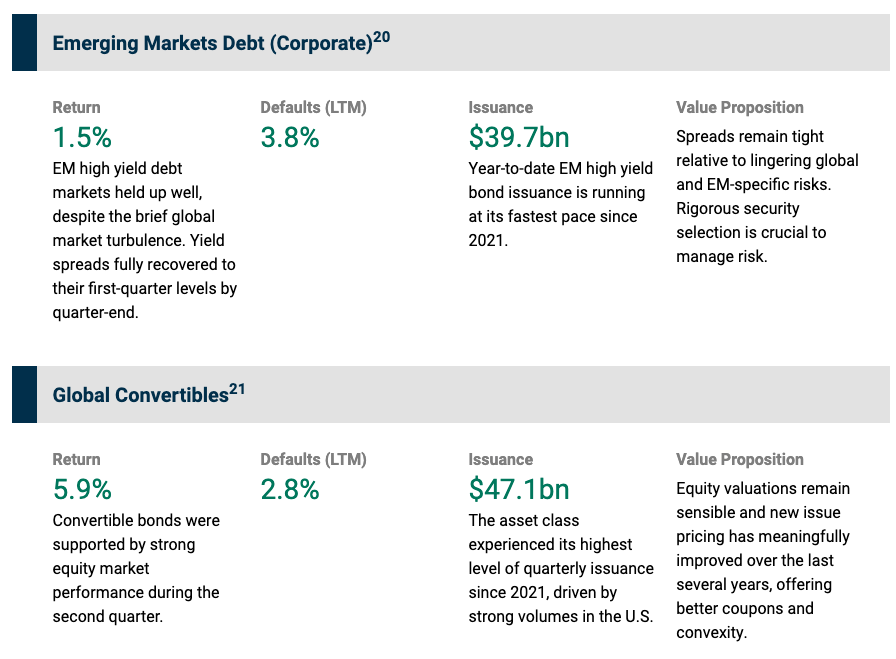

While the size of the U.S. markets will keep them the de facto center of global credit portfolios, we believe there are also attractive opportunities outside of the U.S. Europe is an obvious example, with a GDP not much below the U.S. ($29.2 trillion versus $23.0 trillion) but with capital markets that are much smaller.7 When appraising opportunities in European credit, we note:

- Attractive hedged yields and limited default expectations, from sub-investment grade liquid credit instruments. The European high yield, senior loan, and CLO markets are small compared to their U.S. counterparts but still significant in absolute terms; they currently offer a strong value proposition, benefiting from the technical support of a robust buyer base.

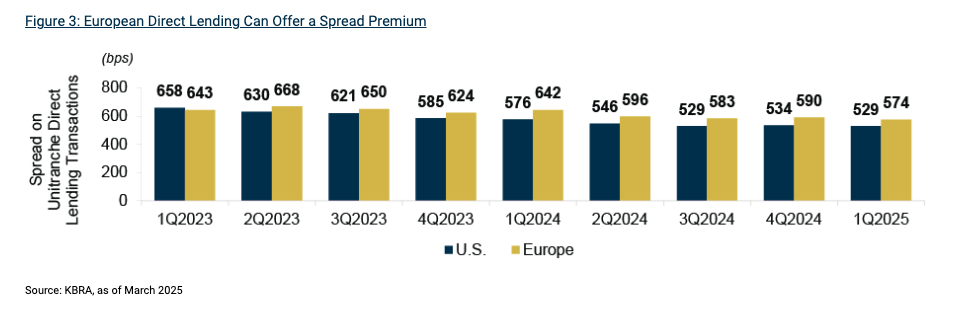

- Broad direct lending opportunities, generally with a spread advantage over U.S. deals. (See Figure 3.) Because Europe is historically a bank-driven market, there’s meaningful potential for alternative lenders to take share as traditional lenders retrench. Issuance in Europe has been relatively resilient despite macroeconomic volatility, with over €22 billion of direct lending volume in the first half of 2025.8

- A strong macroeconomic backdrop, standing to benefit from (a) increased government expenditure, most notably on defense, (b) a relatively stable policy environment, and © heightened demand from investors amid a perception shift towards Europe.

As we discussed in a recent podcast, European credit appears to be well-positioned for the current market environment, with limited default expectations and robust technical support. We highlight the value proposition for the likes of European senior loans, which remains a very stable asset class, underpinned by consistent demand from CLOs and limited access for retail investors.

Equities Most Exposed to a Slowdown

Even a modest decline in U.S. exceptionalism could present meaningful challenges for public equities. Over the last several months, the S&P 500 has reached record highs and now trades at a price/earnings (p/e) ratio of 23, significantly above the long-term average and also far above the level of equity markets in other regions, being predicated on the continuation of the U.S. as the best business environment in the world.9 Historically, buying into equities at such elevated p/e levels has led to meager returns, with research indicating buying the S&P 500 at today’s multiples leads to long-term returns between -2% and 2%.10

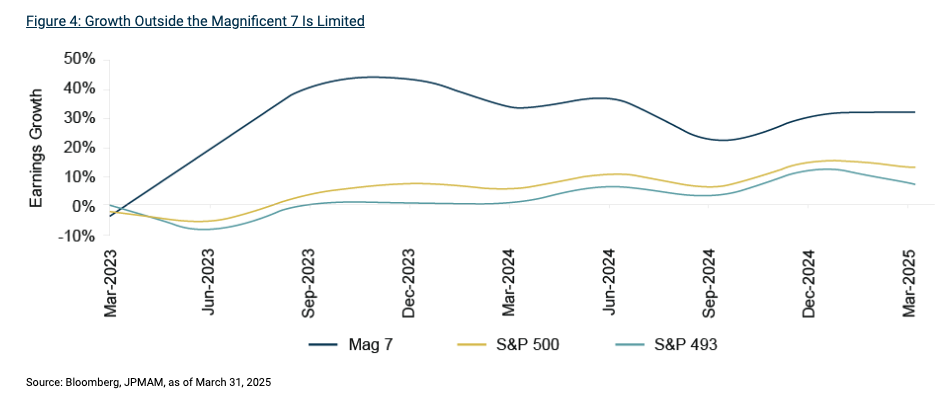

It’s well broadcast that there’s an extraordinary level of concentration in the S&P 500 right now, with the Magnificent Seven making up over 30% of the index.11 These high-flying companies all trade at elevated p/e ratios. However, Magnificent Seven investors can take some comfort in the fact these companies are legitimately exceptional, with unrivaled cash generation, deep competitive moats, and most crucially, an ability to keep growing earnings at an unusual rate. (See Figure 4.)

Perhaps, somewhat ironically, it’s the ‘‘S&P 493’’ that presents the biggest concern, even with its more modest p/e ratio. Excluding the Magnificent Seven takes the index multiple down to 21. But that’s still high, and many of the constituent companies aren’t high-growth superstars: they’re growing slowly (or not at all) and beginning to feel the pain of higher interest rates. Notably, the ‘‘S&P 493’’ generate most their revenue domestically (unlike the more international Magnificent 7), reducing the insulation provided by foreign earnings should U.S. growth slow. Ultimately, should these companies be unable to substantially grow the “e” in their “p/e” ratio, and investors stop tolerating the inflation of equity multiples, then it’ll be the “p” that must adjust downward.

In Summary

The U.S. remains the center of the sub-investment grade credit universe, offering extensive opportunities to deploy at scale in the likes of high yield bonds, structured credit, and private credit. A dramatic increase in borrowers since the GFC allows for the creation of diverse U.S. credit portfolios but we continue to greatly value the additional diversification and opportunities provided by credit in other geographies. Managers with expertise in both the U.S. and regions such as Europe and Asia stand to benefit from building global portfolios with a disciplined focus on relative value.

We note some U.S. economic challenges, and though it’s hard to imagine these being catastrophic, there is a chance of a slowdown. This potential downturn will likely deflate S&P 500 multiples before it hits credit. In other words, diversified credit portfolios remain a solid bet in this uncertain environment.

Credit Markets: Key Trends, Risks, and Opportunities to Monitor in 3Q2025

(1) Signs of Supply?

In Oaktree Credit Quarterly 1Q2025: Gridlock, we discussed the supply/demand imbalance in the leveraged credit markets. Put simply, credit issuance has been limited as private equity sponsors deal with the headache of rising interest rates, while demand from yield-seeking investors has been robust. Market participants have been waiting for more primary issuance – and there are some signs it’s starting to return.

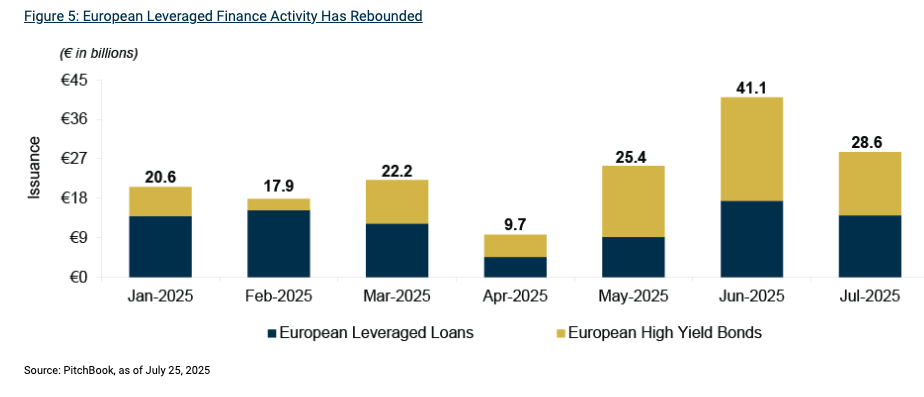

Sub-investment grade credit issuance has accelerated since the tariff-induced pause in April. Activity in Europe has been particularly notable, supported by improving investor sentiment toward the region. While much of the volume is refinancings, the €17.4bn of loan issuance in June still represents the highest level since March 2021.13 (See Figure 5.)

(2) CLOs keep coming!

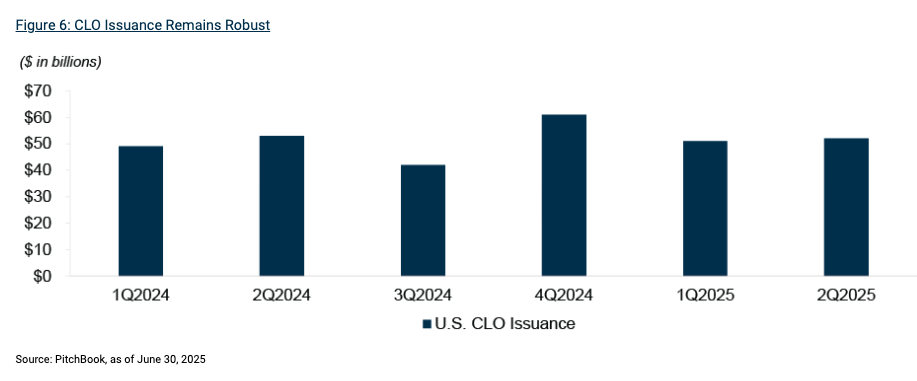

There’s sometimes talk of a looming slowdown in CLO issuance – and what it would mean for the leveraged loan market – but aside from brief pauses when uncertainty is particularly acute (e.g., April 2025), the CLO market has demonstrated the ability to “keep calm and print on.” So far this year, we’ve seen $125bn of new CLO issuance in the U.S. and nearly €40bn in Europe, supported by significant demand from investors for floating-rate debt with attractive coupons.14 (See Figure 6.) This demand contributes to the tightening of CLO liability spreads, providing a significant boost for CLO managers.

However, most CLO managers will likely remain hopeful that the apparent rebound in loan issuance will continue. If the resumption of primary market activity holds, managers will have the ingredients to fill warehouses and rotate out of certain portfolio holdings in favor of accretive primary paper. Moreover, an easing of the supply/demand imbalance will give CLO managers greater power to push back against aggressive loan repricings and unreasonably tight primary issuance.

(3) Spreads don’t break

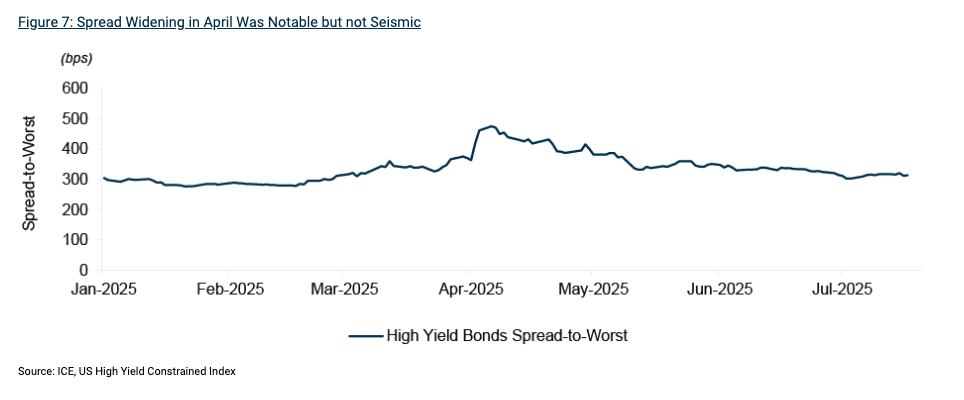

In April, credit spreads properly widened for the first time in a long time. High yield bonds went from trading at a spread of below 300 basis points to nearly 500.15 (See Figure 7.) That’s big but not that big given the circumstances: massive uncertainty regarding trade policy and a seemingly imminent all-out trade war. This has become a familiar theme – the sub-investment grade credit markets are able to shrug off volatility and, when dislocation does briefly occur, the rebound is remarkably quick. We assessed why on a recent podcast, but here’s a few factors worth highlighting:

- Market quality: the U.S. high yield market is now over 50% BB-rated, with that percentage even higher in Europe.16 With a higher average quality than the high yield market of old, it’s reasonable to expect a more moderate average spread range.

- A broader lender base: private credit has rapidly risen to become a complement to the syndicated markets. This has (a) transferred smaller borrowers from the public to private markets and (b) given borrowers a second funding option when syndicated debt placement is challenging.

- More opportunistic buyers: a proliferation of distressed debt managers has created a cohort of buyers ready to step in as spreads widen, serving to create a floor in pricing.

About Oaktree’s Credit Platform

Oaktree Capital Management is a leading global alternative investment management firm with expertise in credit strategies. Our credit platform has $149 billion in AUM and encompasses a broad array of strategy groups that invest in public and private credit instruments across the liquidity spectrum.25 All Oaktree investment activities operate according to a unifying philosophy that emphasizes key principles including the primacy of risk-control and benefits of specialization.

Endnotes

1MSCI, as of June 30, 2025; census.gov, as of July 24, 2025.

2Bloomberg, as of June 30, 2025.

3Federal Reserve, IMF.

4Congressional Budget Office.

5ICE, UBS.

6Incorporates multiple sources, with extrapolation where appropriate.

7International Monetary Fund, December 2024.

8PitchBook, as of June 30, 2025.

9Bloomberg, as of July 31, 2025.

10JP Morgan.

11LSEG Datastream, as of July 18, 2025.

12Bloomberg, as of July 31, 2025.

13PitchBook.

14PitchBook, as of August 1, 2025.

15ICE US High Yield Index.

16ICE US High Yield Index, ICE BofA Global Non-Financial High Yield European Issuer Excluding Russia Index, as of July 31, 2025.

17ICE U.S. Corporate Index for all return data; Bank of America for all issuance data (reflects U.S. issuance).

18ICE BofA US High Yield Constrained Index for all U.S. High Yield Bonds return data; ICE BofA Global Non-Financial High Yield European Issuer Excluding Russia Index for all European High Yield Bonds data; JP Morgan for all U.S. default rates; UBS for all European default rates (including distressed exchanges); PitchBook LCD for all U.S. and European issuance data (including refinancings).

19S&P UBS Leveraged Loan Index for all U.S. Senior Loans return data; Credit Suisse Western Europe Leveraged Loan Index for all European Senior Loans return data; JP Morgan for all U.S. default rates; UBS for all European default rates (excluding distressed exchanges); PitchBook LCD for all U.S. and European issuance data (including refinancings).

20JP Morgan Corporate Broad CEMBI Diversified High Yield Index for all return data; JP Morgan for default rates (including distressed exchanges) and issuance (including refinancing) data.

21Refinitiv Global Focus Convertible Index for all return data; Bank of America for default rates and issuance data.

22JP Morgan CLOIE BB Index and JP Morgan CLOIE BBB Index for all return data; PitchBook LCD for all issuance data.

23Bloomberg US CMBS 2.0 Baa Total Return Unhedged Index for all return data; Trepp for default rates (%, 30+ day delinquency, and REO); JP Morgan for all issuance data.

24Oaktree Market Observations

25The AUM figure is as of June 30, 2025 and excludes Oaktree’s proportionate amount of DoubleLine Capital AUM resulting from its 20% minority interest therein. The total number of professionals includes the portfolio managers and research analysts across Oaktree’s performing credit strategies.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Notes and Disclaimers

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. Responses to any inquiry that may involve the rendering of personalized investment advice or effecting or attempting to effect transactions in securities will not be made absent compliance with applicable laws or regulations (including broker dealer, investment adviser or applicable agent or representative registration requirements), or applicable exemptions or exclusions therefrom.

This document, including the information contained herein may not be copied, reproduced, republished, posted, transmitted, distributed, disseminated or disclosed, in whole or in part, to any other person in any way without the prior written consent of Oaktree Capital Management, L.P. (together with its affiliates, “Oaktree”). By accepting this document, you agree that you will comply with these restrictions and acknowledge that your compliance is a material inducement to Oaktree providing this document to you.

This document contains information and views as of the date indicated and such information and views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree believes that such information is accurate and that the sources from which it has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based. Moreover, independent third-party sources cited in these materials are not making any representations or warranties regarding any information attributed to them and shall have no liability in connection with the use of such information in these materials.

© 2025 Oaktree Capital Management, L.P.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All