Investing in healthcare has long been a cornerstone of defensive, long-term growth strategies. It is, after all, a massive and expanding segment of the global economy. However, most healthcare ETFs tend to be biased toward big pharma and insurance companies.

The ROBO Global Healthcare Technology and Innovation Index (HTEC) represents a differentiated approach. It includes companies at the forefront of healthcare innovation that are solving healthcare challenges and improving lives through technology.

Equity investors should arguably have exposure to healthcare given the growth trajectory and its size in broad equity benchmarks. However, investors may benefit from taking a more technology-oriented approach to this sector.

Why Healthcare?

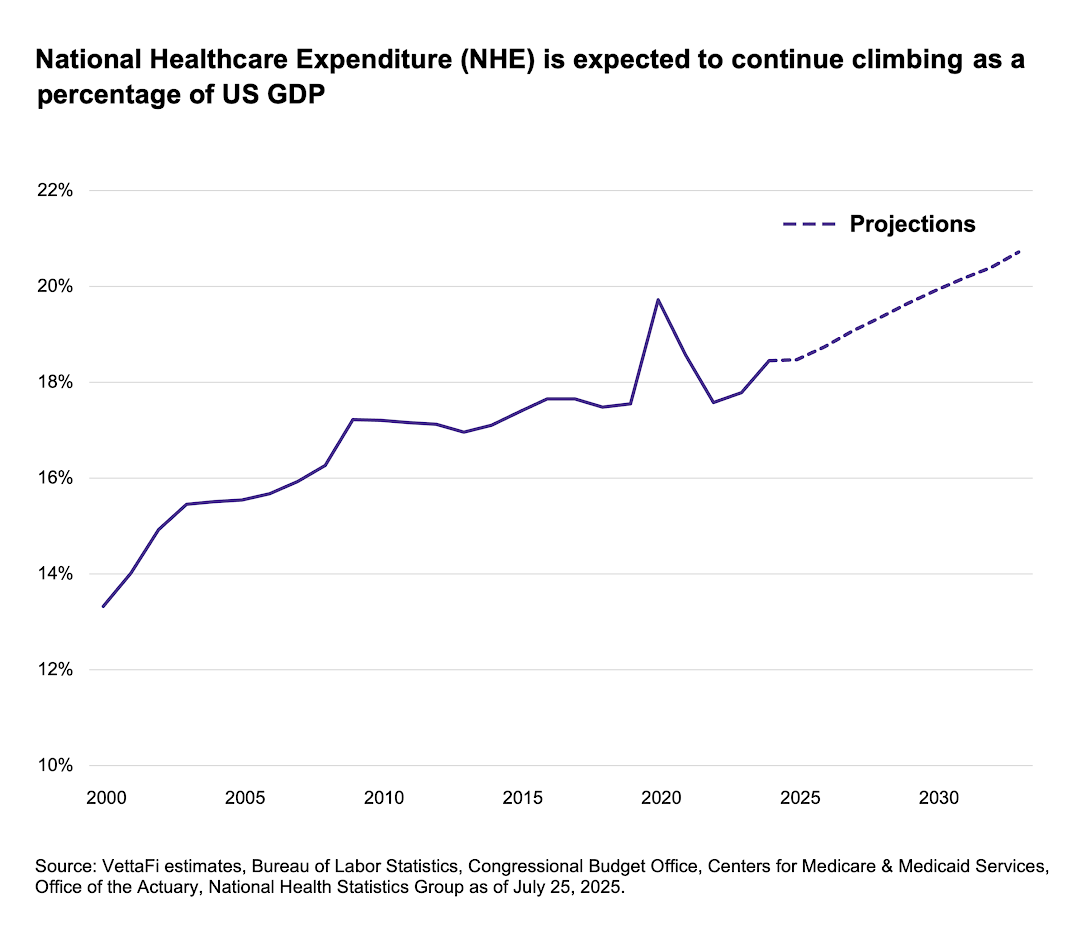

U.S. healthcare spending reached $4.9 trillion in 2023, representing over 17.6% of GDP. This share of the economy will likely expand further. National healthcare expenditure is projected to grow at a faster rate than annual GDP, pushing the figure above 20% by 2033, as shown below.

This trend is propelled by powerful demographic tailwinds. By 2050, one in four people in Europe and North America will be over the age of 65. This will drive inelastic demand for advanced medical solutions. However, this growth is set against a backdrop of immense secular challenges. These include spiraling costs, administrative waste, and a shortage of skilled workers, creating a complex investment landscape.

With the broader healthcare sector trading at a significant discount, many investors see a compelling entry point. The valuation gap is stark. Morningstar estimates a 10% discount to fair value based on median price for the broad healthcare sector. VettaFi data shows HTEC trading near its lowest historic NTM EV/Sales ratio.

Broad indexes, by design, capture all facets of the industry — innovators and the laggards alike. This risks exposure to “value traps”: legacy companies in structural decline or “zombie” firms trading below their cash value after failing to successfully commercialize their technology. Recognizing these pitfalls makes a selective, research-driven approach paramount.

Why a Healthcare Allocation Can Benefit From a Technology-Focused Strategy

This is where a targeted, technology-focused strategy offers a differentiated path. Instead of merely capturing revenue streams across the sector, an index like HTEC employs a research-driven process to identify the true leaders of the healthcare revolution (read more).

Potential constituents are scored on metrics beyond revenue purity. These metrics include technology leadership, market position, and investment in future growth. This “smart passive” methodology ensures the portfolio tilts toward the best-in-class companies poised to solve healthcare’s biggest challenges, rather than those simply benefiting from the status quo. The result is a fundamentally different portfolio construction.

A simple, market-cap-weighted approach to healthcare can be suboptimal. Many healthcare indexes tend to be heavily tilted to biopharmaceuticals, often with a concentration in a few mega-cap names. As of July 24, the Health Care Select Sector SPDR (XLV) was 12.9% Eli Lilly (LLY) and 8.3% Johnson and Johnson (JNJ).

HTEC, in contrast, has a more balanced exposure, with ~40% in biopharma, focusing on those using novel technologies. This diversification is further enhanced by a modified equal-weighting that limits top-10 concentration. The largest name in HTEC as of July 24 was just a 2.7% weight.

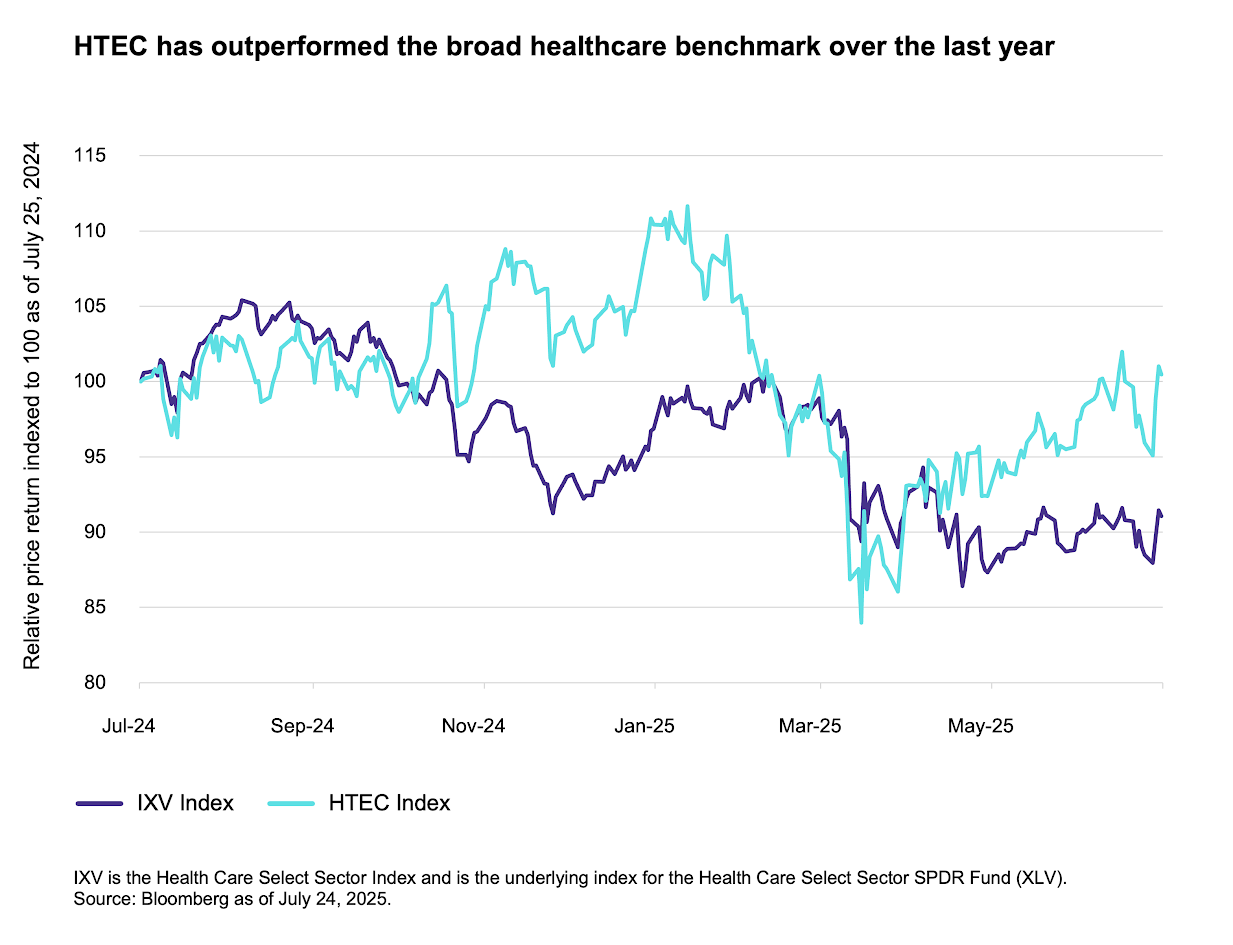

With HTEC’s unique approach, performance is differentiated as well. The chart below shows relative price performance for HTEC compared to XLV’s underlying index for the last year.

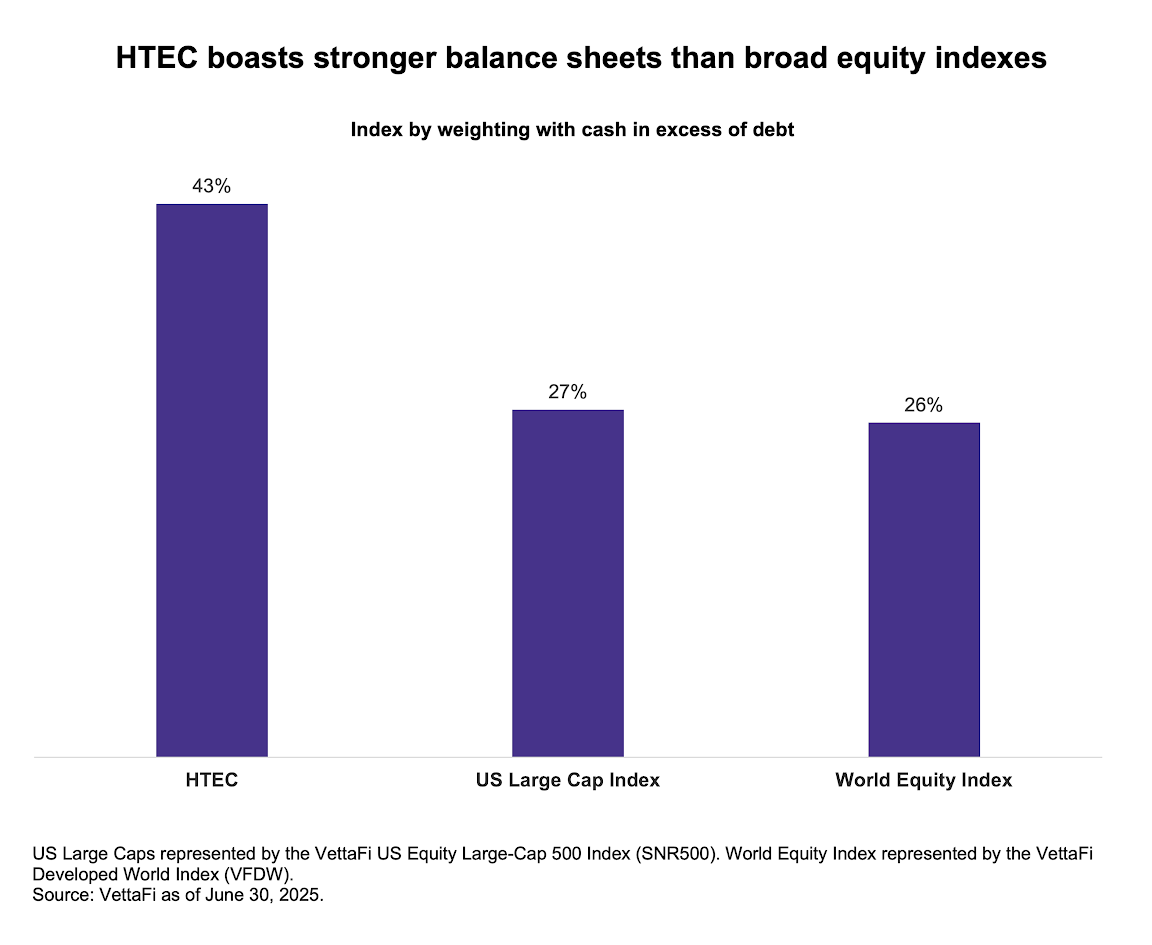

Critically, HTEC also filters for quality. While broad healthcare indexes may hold struggling legacy players, 43% of HTEC by weighting hold cash in excess of debt. This implies stronger balance sheets than a typical broad U.S. large-cap index or developed world index as shown below.

Ultimately, investing in the future of healthcare shouldn’t be a broad bet on the entire system, at least not any more. It should be a targeted investment in the innovators creating a more efficient and effective future. By focusing on the technology leaders in fields like genomics, robotics, data analytics, and precision medicine, a specialized strategy provides exposure to the solutions, not the problems. This offers a compelling way to capture the immense upside of the healthcare revolution while mitigating the risks embedded in broad, legacy-heavy indexes.

Related research:

The Robot Will See You Now & AI Will Read Your Results

Looking for regular updates? Subscribe here for weekly insights on robotics, AI, and healthcare technology, delivered straight to your inbox.

For more news, information, and strategy, visit the Disruptive Technology Content Hub.

HTEC is the underlying index for the Robo Global Healthcare Technology & Innovation ETF (HTEC) and the L&G Healthcare Technology & Innovation UCITS ETF (DOCT.LN).

VettaFi is the index provider for HTEC ETF and DOCT.LN, for which it receives an index licensing fee. However, HTEC ETF and DOCT.LN are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi and its affiliates have no obligation or liability in connection with the issuance, administration, marketing, or trading of HTEC ETF and DOCT.LN.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more commentaries by VettaFi