Tariffs, Tech, & Shifting Momentum

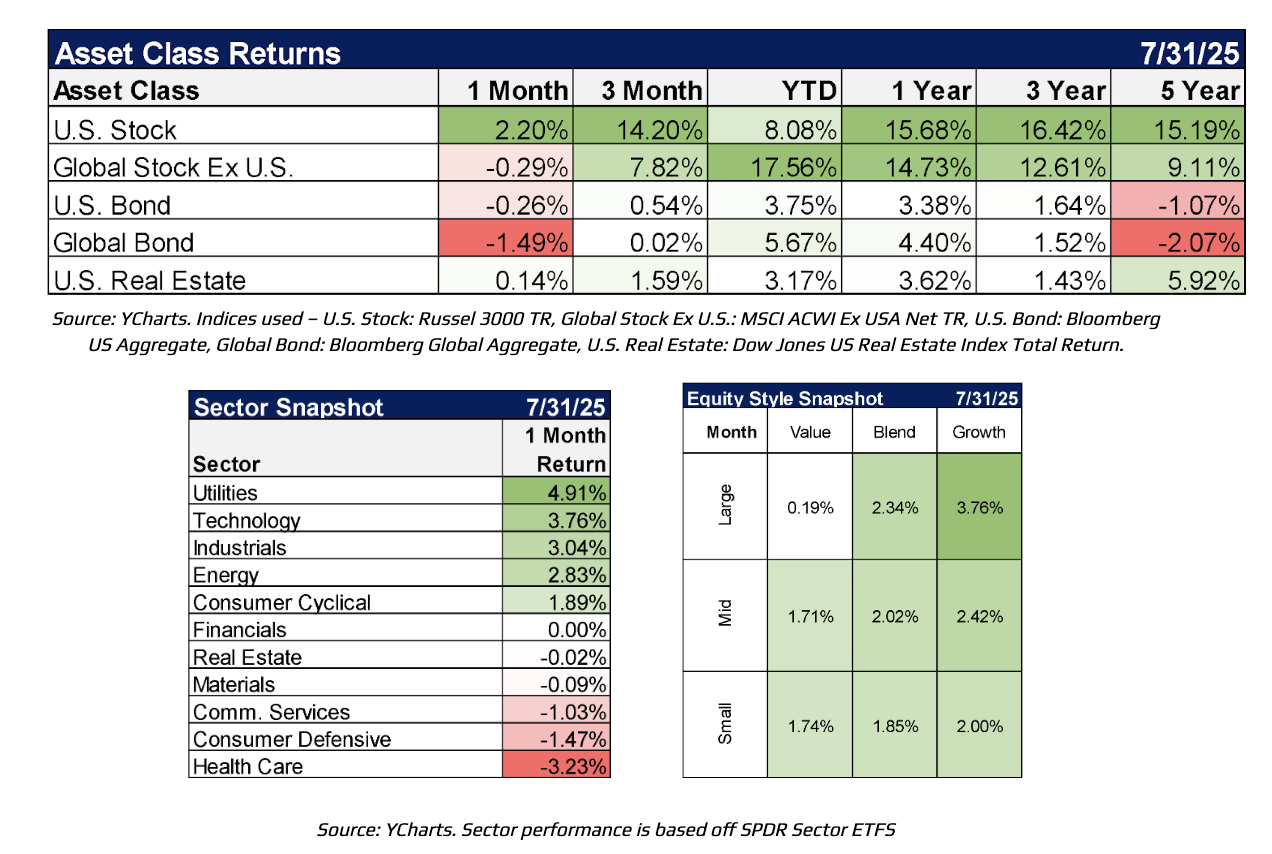

Markets have largely dismissed tariff risks, viewing them as manageable, with U.S. equities climbing to record highs and the S&P 500 trading at 22.5x forward earnings. Although international equities still lead year-to-date, U.S. stocks have outperformed over the past one and three-month periods as investors appear to be looking past near-term trade uncertainty. Much of the cost burden from tariffs to date was absorbed by importers and businesses, though the effects vary across sectors and are still unfolding.

Investor sentiment has been further supported by strong earnings from mega-cap tech and ambitious AI infrastructure spending plans by the so-called “Big Four of AI”, with Meta, Amazon, Microsoft, and Alphabet, marking a significant departure from their traditionally capital-light business models. The accelerating need for compute capacity will likely sustain demand for energy infrastructure, positively impacting adjacent sectors such as utilities and industrials within the AI ecosystem. Looking ahead, corporate profit margins will be a key indicator. Companies with stronger pricing power are likely to weather cost pressures more effectively. While tariffs may contribute to inflation and modestly slow growth, their longer-term impact on the broader economy is expected to remain contained.

Data-Dependent Swings

That narrative was disrupted by the July jobs report, which showed payrolls rising by just 73k versus expectations of 104k, alongside downward revisions of 258k for the prior two months, casting doubt on the idea of a resilient, tariff-insulated economy.

A deeper look reveals job growth concentrated almost entirely in Health Care and Social Assistance, which are defensive, non-cyclical sectors less reflective of underlying economic strength. Meanwhile, employment in more cyclical areas such as Information and Professional Services has stalled.

Similarly, manufacturing employment remains in contraction territory, with no meaningful rebound to date. While a shift toward domestic production is underway, its impact will take time to filter through the economy.

Given these dynamics, economic data must be interpreted in the context of broader trends. As the saying goes, “one data point does not a trend make.” Labor force participation has been suppressed by demographic shifts and restrictive immigration policies, distorting headline figures. Monitoring revisions and alternative data sources will be essential in assessing the true state of the labor market.

Where Are We Headed?

Much of the market’s attention remains focused on the Federal Reserve. As widely anticipated, the FOMC held interest rates steady for the fifth consecutive meeting, balancing the economy’s underlying resilience with the potential lagged impact of recently imposed tariffs. Inflation remains sticky, rising 2.67% year-over-year, partly due to cost-push pressures in tariff-affected sectors.

In this environment of policy ambiguity and geopolitical disruption, short-term yields remain attractive, and investors appear hesitant to fully re-enter risk markets. Reflecting this caution, M2 money supply growth has accelerated over the past 12 months, potentially signaling a rising preference for liquidity over risk exposure.

Meanwhile, private AI investment has overtaken consumer spending as the largest contributor to GDP growth in Q2, coinciding with a re-narrowing in equity market leadership. In July, NVIDIA alone accounted for over 40% of total Russell 1000 returns, highlighting how heavily concentrated performance has become.

This divergence suggests that any broadening of earnings growth outside of AI-adjacent sectors may be short-lived. Goldman Sachs Research reports that capex projections were cut most sharply for companies with high exposure to tariffs and trade policy uncertainty, including the risk of retaliation. As a result, AI and its supporting infrastructure continue to dominate capital allocation and earnings momentum in the near term.

The key question now is this: if the U.S. AI juggernaut falls short of earnings expectations, how will the market, and, increasingly, the broader economy respond, given how deeply intertwined the two have become?

Does this signal the market correction many feared during the height of this year’s tariff concerns? In short, not necessarily. It is far too early to draw definitive conclusions. More likely, markets will pause as investors await clearer evidence on how recent policy developments are affecting economic growth and, by extension, the Fed’s dual mandate. Against this backdrop, August is shaping up to be a more volatile and directionless month for equities.

From The Investments Desk at JSW

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Journey Strategic Wealth

Read more commentaries by Journey Strategic Wealth