Washington Unleashes AI Gold Rush with Executive Order on Data Centers

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIf there’s one thing I’ve learned after decades in the investment world, it’s that government policy is a precursor to change. What’s unfolding right now with artificial intelligence (AI) in the U.S. is a full-blown industrial revolution, and it’s being backed and subsidized by the federal government like few things I’ve seen before.

This week, President Donald Trump signed an executive order that could mark the beginning of a new era in U.S. manufacturing and energy. With the stroke of a pen, the White House declared AI data centers and their supporting infrastructure—semiconductors, transmission lines, power generation and more—a national priority.

What this means is faster permitting, regulatory rollbacks, access to federal land and potentially hundreds of billions in new investment flowing into this industry over the coming decade.

The Rise of the AI-Industrial Complex

I believe that what’s happening right now with AI is similar in scale and ambition to the defense buildout of the Reagan years or the shale revolution of the 2010s.

The Trump administration’s new executive order, signed on July 23, seeks to streamline the development of large-scale AI data centers that consume more than 100 megawatts of power. That’s a massive amount of compute muscle, but it’s necessary to train and run next-generation AI models.

Trump’s EO also prioritizes projects with $500 million or more in capital expenditures, fast-tracking them through what used to be a years-long regulatory slog.

In short, the White House is telling the tech industry: “Build it, and build it fast.”

Trump Touts Billions in Private Investment at Energy Summit

One of the more ambitious announcements so far came earlier this month during the Pennsylvania Energy and Innovation Summit, where Trump unveiled more than $90 billion in new private capital pledges for AI and energy infrastructure.

That includes $25 billion from Alphabet (Google’s parent company) and another $25 billion from alternative investment firm Blackstone, all dedicated to developing AI data centers and natural gas facilities in the Keystone State.

Why was Pennsylvania selected? The state sits atop the Marcellus Shale, one of the largest natural gas deposits in the world. These new AI centers are energy-hungry, and gas is abundant and cost-effective.

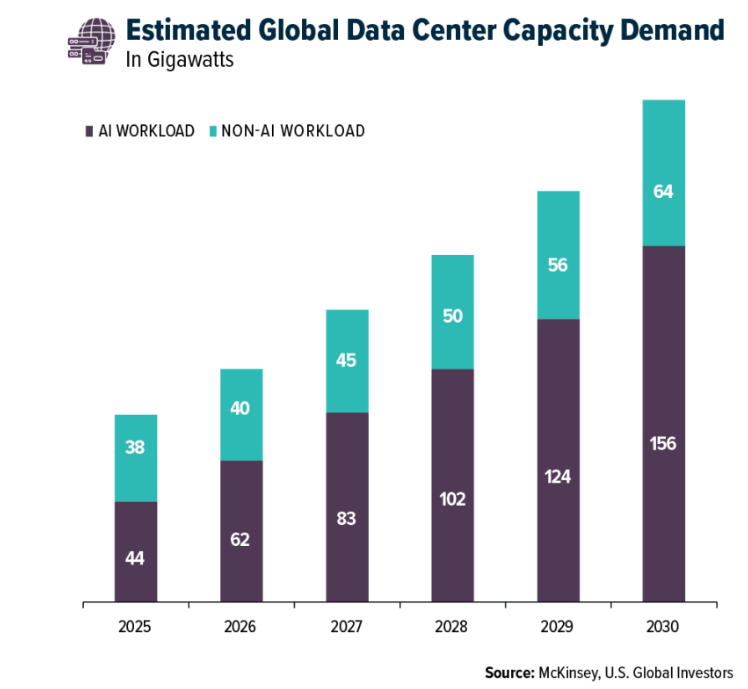

A $6.7 Trillion Infrastructure Boom

According to McKinsey, the global price tag to scale AI data centers could hit a staggering $6.7 trillion by 2030. Of that, $5.2 trillion would be earmarked for facilities designed to handle AI workloads.

That’s an unfathomable number. To put it in perspective, that’s more than twice the size of Germany’s GDP.

In February, Goldman Sachs projected that AI-driven data centers could push global electricity demand up 165% by 2030. That’s in a world where many utilities have seen flat demand for decades. Now, they’re scrambling to add new capacity, and Goldman estimates the U.S. will need over 500,000 new power-sector workers just to keep pace.

Wall Street’s Money Is Following Washington’s Lead

In many ways, it seems as if AI is eating the world. According to PitchBook, AI startups in the U.S. alone raised $104 billion in the first half of 2025, nearly matching their total for the entire year of 2024. That represents more than 60% of all venture capital raised nationwide.

Elsewhere, Facebook’s parent company Meta is raising $29 billion from private credit firms to build out data centers, including a new 20-year agreement to power its AI efforts with nuclear energy from Illinois.

Elon Musk’s xAI is reportedly on pace to burn through $13 billion this year as it builds custom AI infrastructure from scratch.

Even private equity is getting in on the act. The American Investment Council (AIC) reports that over $1 trillion has been invested in AI infrastructure since 2020, from data center buildouts to semiconductor fabs to clean energy projects.

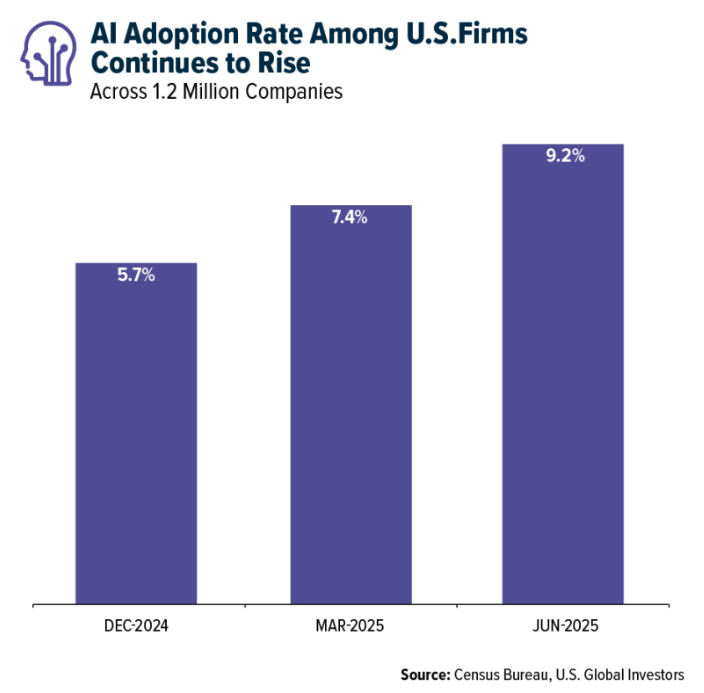

AI Adoption Still in the Early Innings

A recent survey conducted by the Census Bureau found that just 9.2% of American companies are using artificial intelligence today. That’s up from 7.4% in the first quarter of this year and 5.7% at the end of 2024.

The American AI Century

I believe we’ve entered a new industrial age—one where data is the new oil, and compute is the new horsepower. Washington is signaling that America’s future competitiveness depends on winning the AI race, and they’re laying the legal and financial groundwork to do just that.

I’m paying attention to policy. The last time we saw this kind of coordinated push was during the Space Race and the Reagan defense expansion. Both were followed by generational investment opportunities.

The AI revolution won’t be built overnight, but it’s already under construction. As always, the early movers stand to reap the biggest rewards.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.26%. The S&P 500 Stock Index rose 1.46%, while the Nasdaq Composite climbed 1.02%. The Russell 2000 small capitalization index gained 0.94% this week.

- The Hang Seng Composite gained 2.45% this week; while Taiwan was down 0.08% and the KOSPI rose 0.25%.

- The 10-year Treasury bond yield fell 3 basis points to 4.383%.

Airlines and Shipping

Strengths

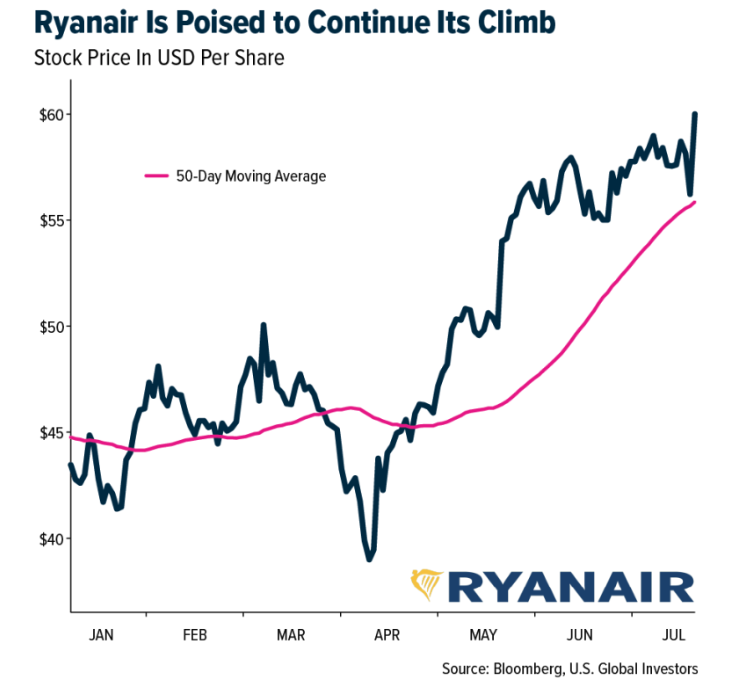

- The best-performing airline stock for the week was Ryanair, up 13.6%. SkyWest reported another strong quarter, earning $2.91 in GAAP earnings per share. After adjusting for a $0.20 benefit from X, adjusted earnings per share came to $2.71. This beat TD’s estimate by almost 12% and consensus by 15%, marking SkyWest’s 10th consecutive earnings per share beat. Profitability continues to benefit from the positive flywheel of improved labor staffing, which allows SkyWest to increase asset utilization and meet strong demand for regional capacity.

- Crude tanker ton-mile demand grew 4% year-over-year in the first half of July, with Chinese imports tracking at double-digit year-over-year growth. Middle East-to-China VLCC spot rates have started the third quarter of 2025 averaging 10% year-over-year higher, while VLCC forward curves suggest a rebound back to $40,000 per day in the coming months, tracking 10–20% year-over-year higher, according to Bank of America.

- Ryanair’s first quarter of fiscal year 2026 adjusted profit after tax of EUR 820 million was 15% ahead of consensus forecasts. Notably, the 21% year-over-year increase in average base fare exceeded the mid-May guidance of mid- to high-teens. Ryanair’s outlook for the second quarter and full fiscal year 2026 has also improved slightly from the mid-May outlook, according to Raymond James.

Weaknesses

- The worst-performing airline stock for the week was Southwest, down 9.0%. The Department of Transportation proposes to withdraw approval and the grant for a joint venture operated by Delta Air Lines, Inc., and Aero Mexico. Based on their review, the conditions required for an immunized joint venture do not exist, and the immunized joint venture no longer serves the public interest, largely due to anticompetitive measures imposed by the Government of Mexico.

- Global air cargo rates are averaging 5% year-over-year lower in July so far, with broader oversupply weighing on the market. North Asia cargo rates are down 5–10% year-over-year, showing the disruptive impact of U.S. tariffs on Hong Kong and China flows, reports Bank of America.

- On-time performance from North American airlines trailed their global peers. For June, the most on-time region was Latin America, averaging 83.90%, followed by Asia Pacific at 82.06%, Europe at 81.41%, and Middle East & Africa airlines at 80.65%. North America’s average was 73.30%. No North American carrier cracked the top 10 most on-time global airlines, according to CIBC.

Opportunities

- Legacy carriers are scheduled to grow third-quarter 2025 capacity by 3.9% year-over-year, with domestic capacity up 3.3% and international up 4.8%. American Airlines will see the most growth at La Guardia (+21%) and Chicago (+15%). Delta is expanding the most at Boston (+7%) and Salt Lake City (+7%), while United is expanding at Denver (+10%).

- Raymond James’ shipping “tightness indicator” (where a higher reading means tighter conditions according to shippers) increased to 5.4 in the second quarter of 2025, up from 5.1 in the first quarter, and has remained in a tight range of 5 to 6 over the last five quarters.

- According to Morgan Stanley, Alaska Air received Department of Transportation transfer approval for Hawaiian Airlines. This approval covers the transfer of “certificates and other economic authorities” from Hawaiian to Alaska Air Group. The transfer will be effective 60 days after July 14 and is expected to be completed by October 2025. This marks another step toward fully combining Alaska and Hawaiian under a single operating certificate.

Threats

- According to Morgan Stanley, Department of Transportation measures could severely impact Mexican carriers. These measures include filing schedules with the DOT and requiring prior approval for flights to or from the United States. Potential reciprocal actions by Mexico could affect U.S. carriers and worsen the impact on Mexican airports.

- UBS reports that total air cargo capacity deployed from Asia (including China) to the U.S. is down 7% year-over-year. This decline is mainly driven by Express capacity, which is down 14% year-over-year.

- Southwest Airlines reported adjusted earnings per share of $0.43 for the June quarter, below the FactSet consensus of $0.51. The miss compared to Goldman’s forecast was primarily driven by worse-than-expected revenue and higher-than-expected fuel costs. Revenue per available seat mile declined 3.1% year-over-year, near the lower end of the company’s flat to down 4% guidance, with management attributing 50 basis points of pressure to temporary issues related to the Basic Economy conversion rate.

Luxury Goods and International Markets

Strength

- Super luxury carmaker Ferrari closed at a record high this Wednesday. The company continues to deliver strong earnings and free cash flow. Analysts widely cite its pricing power, scarcity-driven demand, and sustained double-digit revenue growth of around 10% per year.

- The eurozone economy showed signs of improvement in June, with the services PMI rising to 51.2 from 50.5. Although manufacturing remained slightly below the 50 threshold (at 49.8), the pace of contraction eased and new factory orders stabilized—suggesting growing momentum and the potential for a regional recovery.

- Rémy Cointreau, the French manufacturer of alcoholic beverages, was the top performer in the S&P Global Luxury Index, gaining 16.5%. Shares rose after the company raised its operating profit target and reported higher-than-expected revenue.

Weaknesses

- Tesla reported an earnings miss. Revenue fell 12% year-over-year, marking the company’s worst annual revenue decline in over a decade. However, revenue rose 16.6% quarter-over-quarter. Shares declined by 6% on Thursday after the company released financial results the previous day after market close.

- LVMH reported second-quarter revenue of €19.5 billion, missing expectations with a 4% year-over-year decline instead of the anticipated 3% drop. Its core Fashion & Leather Goods division saw a 9% sales decline, worse than the expected 6%. Sales also weakened in China and Japan. LVMH’s ADR shares fell 3.5% on Thursday following the earnings release.

- Star Entertainment Group, the Australian casino and gaming company, was the worst-performing stock in the S&P Global Luxury Index, dropping 7.3%. Bally’s Corporation is acquiring a controlling stake through a $300 million investment that could give it up to 56.7% ownership, pending regulatory approval. However, Bally’s is also under scrutiny due to its high debt load and ambitious projects, including a $1.7 billion Chicago casino venture.

Opportunities

- China has been easing visa restrictions and offering incentives to reposition itself as a leading tourist destination. As of July 11, nationals from 75 countries can enter China visa-free for up to 30 days, driving a projected 16% increase in foreign tourists this year, who are expected to spend $15 billion on consumer goods and services. Local jewelry brands like Laopu Gold and Chow Tai Fook, along with luxury retailers, are positioned to benefit from the tourism rebound.

- European carmakers advanced this week following news that Japan and the United States reached a trade deal to cut tariffs on Japanese car imports from 25% to 15%. The move sparked optimism that similar tariff concessions could be extended to the Eurozone. Volkswagen, Mercedes-Benz, and BMW all posted gains on the news.

- LVMH’s private equity arm, L Catterton, announced an $800 million investment for a 20% stake in private jet company Flexjet. The deal highlights the luxury industry’s expansion into the experience economy as wealthy customers increase spending on travel, dining, and special events. While global luxury goods sales declined 2% last year (according to Bain and Altagamma), luxury hospitality spending grew by 4%, gourmet food and fine dining surged 8%, and sales of yachts and private jets rose 13%.

Threats

- BYD plans to enter Europe’s luxury car market in 2026 with its high-end Yangwang brand, starting with the launch of the Yangwang U8 SUV. Featuring advanced technology like a quad-motor drivetrain, tank turn, and floating capability, the U8 will compete with top European brands such as Bentley and Porsche. With over 1,000 horsepower and a starting price of around $150,000 in China, it poses a serious challenge to Europe’s luxury auto elite.

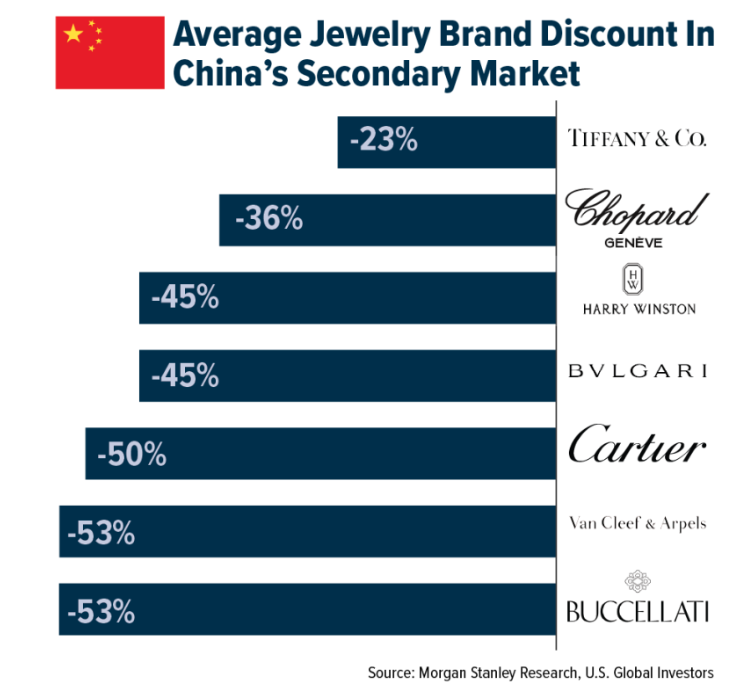

- Morgan Stanley’s luxury goods research team reports that secondhand platforms in China, such as Plum and Zhuanzhuan, are selling iconic jewelry from top brands like Van Cleef & Arpels and Cartier at steep discounts of 36% to 53%, while secondhand handbags are being sold at 32% to 68% below retail. These significant markdowns indicate persistently weak demand for luxury.

- A Financial Times report highlights a surge in Chinese-made synthetic diamonds, now costing approximately 7% of the price of mined ones. Over 50% of engagement rings in the United States now feature lab-grown diamonds, putting pressure on natural diamond giants like De Beers and Alrosa.

Energy and Natural Resources

Strengths

- The best performing commodity for the week was lumber, rising 12.33%. Weyerhaeuser’s second-quarter adjusted EPS of $0.12 beat analyst expectations despite a year-over-year decline, driven in part by higher margins in Real Estate, Energy & Natural Resources, which saw EBITDA surge 40% on a 41% jump in sales. This signals that rising lumber prices are contributing to margin expansion, particularly in timberland-linked segments, even as overall sales volumes decline.

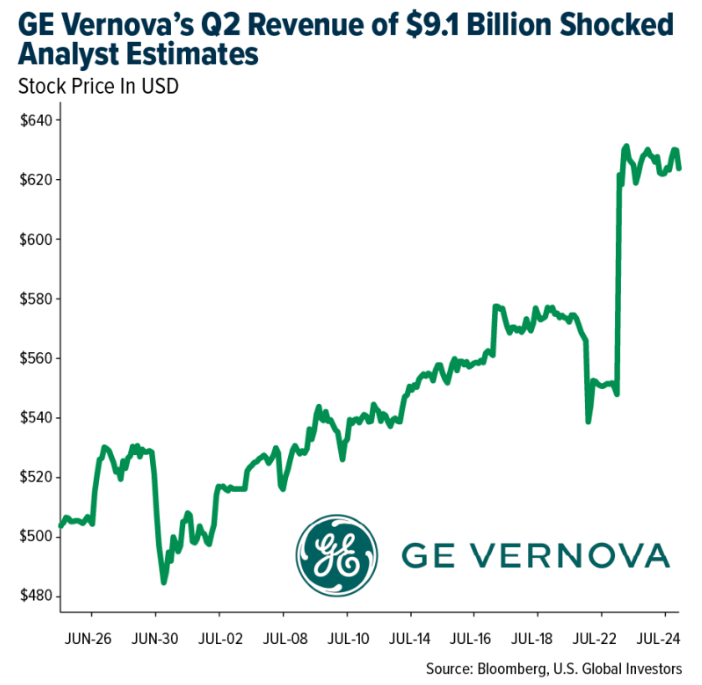

- GE Vernova posted second-quarter revenue of $9.1 billion, shocking analyst estimates by $328 million. Earnings per share came in at $1.86 versus $1.63 expected, and the company raised its free cash flow guidance by $1 billion to $3.25 billion, signaling strong performance and a positive growth outlook.

- TotalEnergies expects to generate $3.5 billion in asset sales by the end of the year through strategic divestitures, helping streamline its portfolio and focus on core operations. The added cash will enhance the company’s financial flexibility and support its long-term growth initiatives.

Weaknesses

- The worst performing commodity for the week was natural gas, dropping 13.07%. Two U.S. LNG cargoes originally destined for Europe were diverted to the Americas after a sharp drop in European gas prices, underscoring weakening demand and eroding profit margins for exporters. The diversions highlight a growing softness in the European LNG market, where ample supply and low volatility have undercut price competitiveness.

- Tata, Nucor, and Steel Dynamics remain the most resilient steel producers amid headwinds such as seasonal weakness, tariff uncertainties, and subdued demand from China—supported by strong fundamentals and robust Indian demand. However, overall market conditions are expected to remain challenging despite their current strength.

- The copper market remains in a wait-and-see mode as ongoing political and social tensions in Panama delay the restart of First Quantum’s key copper mine. This uncertainty highlights continued supply risks in a global copper market already disrupted by recent setbacks and tariffs, leaving prices and long-term stability on uncertain ground.

Opportunities

- Titan Mining is advancing its Kilbourne Graphite Project, with over half of the major equipment delivered and installation set for August 2025. It aims to become the first fully integrated U.S. graphite producer in over 70 years by the fourth quarter, offering a tariff-free domestic supply amid rising trade restrictions.

- NGEx Minerals will spin out net smelter return royalties from its Lunahuasi and Los Helados projects into a new company, RoyaltyCo, with shares distributed to NGEx shareholders. RoyaltyCo is expected to list on the TSX Venture Exchange to boost long-term value and diversification.

- Freeport-McMoRan expects $1.7 billion in added annual U.S. copper sales due to import tariffs lifting domestic prices. However, it warns the trade war could raise input costs by 5% and may require supply chain and volume adjustments.

Threats

- A court rejection of Barrick’s appeal and the continued detention of its employees could escalate tensions with Mali’s military-led government and disrupt about 14% of the company’s global gold output. The standoff raises political risk and may weaken investor confidence in Barrick’s ability to operate in unstable regions.

- Exxon is in talks to return to Iraq’s oilfields, just a year after exiting one of its largest. The move could challenge U.S. oil dominance by reintroducing strong international competition in Iraq’s energy sector.

- Global crude steel production fell 5.8% year-over-year in June 2025 to 151.4 million tonnes, with sharp declines in Asia, Oceania, and Europe. China’s output dropped 9.2%, while India and the U.S. saw gains of 13.3% and 4.6%, respectively. Year-to-date, global output is down 2.2% to 943.3 million tonnes.

Bitcoin and Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Conflux, rising 68.87%.

- PNC Financial Services Group has partnered with crypto exchange Coinbase Global to provide its banking customers with access to digital currency services. The collaboration will likely start by enabling wealth and asset management clients to trade cryptocurrency through their PNC accounts, according to Emma Loftus, head of treasury management at PNC, as reported by Bloomberg.

- Strategy’s upsized $2.5 billion offering to buy more Bitcoin highlights growing institutional confidence in digital currency as a strategic treasury asset. With favorable accounting changes and rising adoption among public companies, this move represents a major opportunity for firms to diversify balance sheets and capitalize on Bitcoin’s long-term upside.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Pump.fun, down 41.20%.

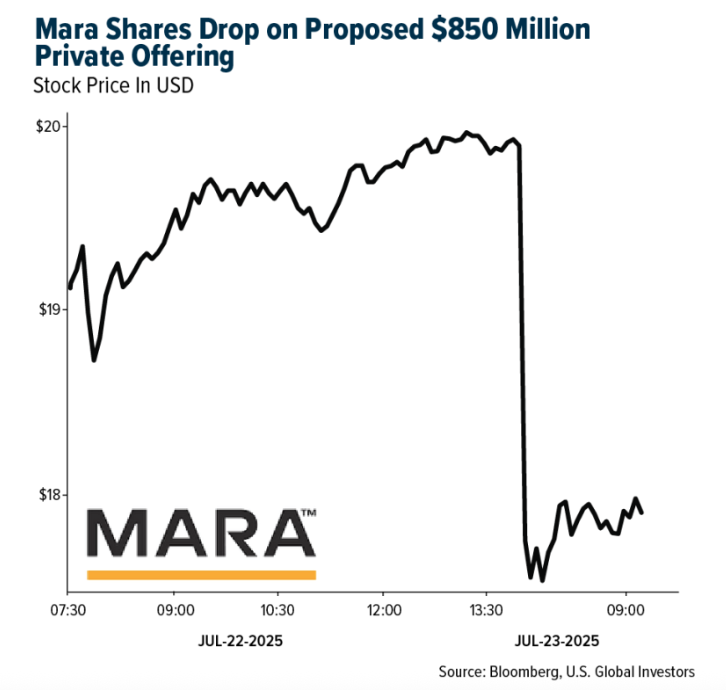

- MARA Holdings shares slid as much as 6.2% in premarket trading Wednesday after the Bitcoin miner announced it intends to offer $850 million of zero-coupon convertible senior notes due in 2032 through a private offering, according to Bloomberg.

- The SEC’s Division of Trading and Markets initially approved the conversion of the Bitwise 10 Crypto Index Fund into an ETF but later issued an indefinite stay suspending the launch. A Bloomberg analyst suggests the SEC may want to finalize a regulatory framework for crypto asset ETPs before allowing such products to convert to ETFs, according to Bloomberg.

Opportunities

- Bank of New York Mellon and Goldman Sachs are collaborating to use blockchain technology to maintain ownership records of money market funds. The firms will use GS DAP, a blockchain platform developed by Goldman, to allow institutional investors to record tokenized versions of select BNY funds, writes Bloomberg.

- The partnership between Goldman Sachs and BNY Mellon to tokenize money market fund shares marks a key step in traditional finance embracing blockchain. With JPMorgan noting the potential to rival stablecoins and use these funds as margin collateral, this move signals a structural shift in how cash moves through markets. Major banks are no longer on the sidelines—they’re leading the next wave of crypto integration.

- Tether Holdings SA is planning to resume business in the U.S. following the passage of landmark U.S. crypto legislation, with a focus on institutional markets. The firm’s CEO says Tether’s U.S. domestic strategy will provide an efficient stablecoin for payments, interbank settlements, and trading, according to Bloomberg.

Threats

- JPMorgan Chase considers the $2 trillion projection for the stablecoin market’s potential growth somewhat optimistic. JPMorgan strategists say the market’s infrastructure and ecosystem are still far from fully developed and will take time to build, making substantial growth over the next few years unlikely, writes Bloomberg.

- ConsenSys plans to lay off 7% of its workforce as part of a broader effort to improve profitability. The company recently acquired a startup with about 30 employees who will remain with ConsenSys, and it intends to continue hiring additional workers, writes Bloomberg.

- Crypto stocks slumped alongside Bitcoin as stronger-than-expected U.S. jobs data dampened hopes for imminent Fed rate cuts, pressuring risk appetite. Rising interest rates pose a clear threat to more speculative assets, tightening liquidity and drawing capital away from high-volatility sectors like digital assets and crypto-linked equities.

Defense and Cybersecurity

Strengths

- RTX Corporation posted stellar second-quarter 2025 results, with revenue up 9.4% to $21.58 billion and net income soaring nearly ninefold to $1.73 billion. Strong aftermarket growth and a record backlog led the company to raise full-year revenue guidance to $84.75–$85.50 billion. Despite trimming earnings per share guidance due to tariffs, the report reinforces RTX’s position as a key defense and aerospace powerhouse.

- Lockheed secured a nearly $1 billion Pentagon contract to continue producing and upgrading its JASSM and LRASM missile lines. These GPS-jamming-resistant missiles enhance U.S. airstrike capabilities and ensure a sustained revenue stream for Lockheed’s strike systems.

- The best performing stock in the XAR ETF this week was Northrop Grumman, rising 9.77%, after the company beat second quarter estimates and raised its full-year profit forecast on strong defense demand and segment performance.

Weaknesses

- Despite U.S. restrictions, over $1 billion worth of Nvidia’s high-end AI chips were smuggled into China via black markets, exposing enforcement gaps and undermining strategic efforts to limit China’s access to advanced AI infrastructure.

- Elbit Systems UK suffered a ransomware attack that compromised sensitive internal systems. Incidents like this highlight persistent cybersecurity vulnerabilities, even among top-tier defense contractors.

- The worst performing stock in the XAR ETF this week was Redwire Corp., which declined 17.21%, after the company launched an upsized secondary share offering which spooked investors due to dilution concerns. The company also closed its costly $1.1 billion acquisition of Edge Autonomy, triggering profit‑taking and renewed scrutiny over its financial runway.

Opportunities

- The UK unveiled a sleek new stealth fighter demonstrator under the GCAP program, while Italy’s Leonardo introduced a 120mm L55 tank gun with extended range and smart capabilities. These innovations highlight Europe’s growing autonomy in high-end military technology.

- Nvidia added RISC-V support to its CUDA software, opening the door to more diverse chip architectures in AI workloads. At the same time, Kallisto AI’s battlefield camouflage and Cleo Robotics’ GPS-denied drones offer AI-powered tactical advantages.

- BlackSky signed a contract to deliver real-time satellite intelligence and analytics to Latin American defense clients. The deal reflects rising demand for on-demand geospatial tools to monitor criminal networks and regional instability.

Threats

- Russia is mobilizing its economy, society, and global influence—including through Africa and cyber warfare—in preparation for a potential large-scale war. Its weapons production pace and alliance with China could outstrip NATO’s response tempo.

- A border dispute escalated into full-scale military conflict involving artillery and airstrikes, resulting in civilian casualties and mass evacuations. The clash destabilizes Southeast Asia and risks drawing in regional powers.

- House Speaker Mike Johnson stated that the U.S. aims to “restore peace through strength” and no longer seeks deep involvement in Ukraine. This shift may weaken long-term Western unity and embolden adversaries.

Gold Market

This week gold futures closed the week at $3394.70, down $19.40 per ounce, or 0.57%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 5.04%. The S&P/TSX Venture Index came in up 0.42%. The U.S. Trade-Weighted Dollar fell 0.80%.

Strengths

- The best performing precious metal for the week was silver, but yet down 0.30%. Bloomberg sees more room for silver to run, supported by rising industrial demand—especially from photovoltaics—and the potential for a rerating against gold as fundamentals improve. With silver still trading at a steep discount to gold and technical indicators suggesting $35 may shift from resistance to support, analysts believe a move toward and above $40 is increasingly plausible.

- According to Raymond James, Osisko Development has entered into a credit agreement with funds advised by Appian for a senior secured project loan facility totaling $450 million. The loan will support the development and construction of Osisko’s fully permitted, 100%-owned Cariboo Gold Project in British Columbia, Canada.

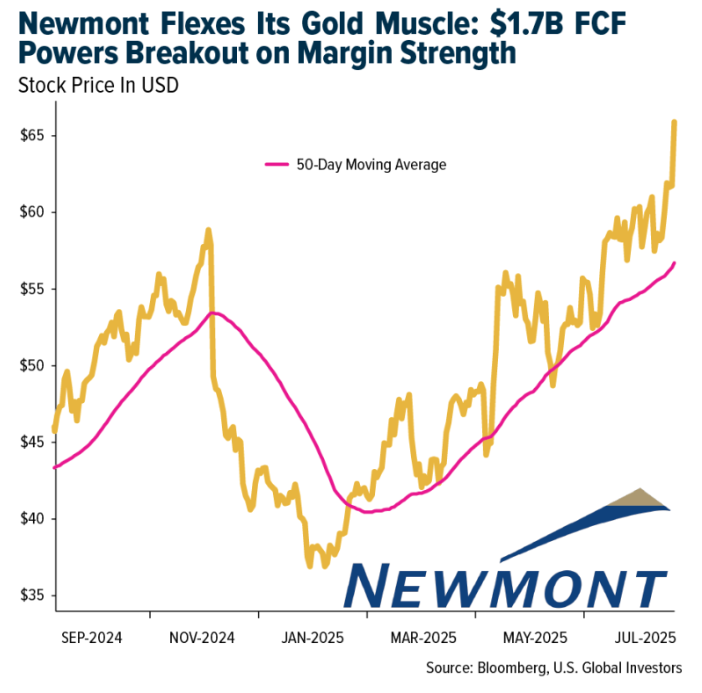

- Scotia reports that Newmont posted earnings per share (EPS) of $1.43, beating the estimate of $1.23. The beat was driven by higher revenue (due to better prices and sales), lower costs, and favorable below-the-line items such as exploration and G&A. Improved production (up 9%) and lower costs led to margin expansion. Newmont repurchased $1.01 billion in shares during the second quarter—or $1.36 billion year-to-date—with another $145 million repurchased in July. The company also announced a new $3.0 billion share repurchase program, bringing the total to $6 billion.

Weaknesses

- The worst performing precious metal for the week was palladium, down 3.15%. Palladium prices remained under pressure in Q2 2025 as Norilsk Nickel, the world’s largest producer, reported an 11% quarter-over-quarter drop in output, compounding a 5% year-over-year decline—reflecting both operational softness and broader demand headwinds. Despite these weak fundamentals, sentiment is showing signs of stabilizing as hedge funds trimmed net bearish positions to a nine-month low, while long-only positions surged to a five-year high.

- Westgold’s fourth-quarter production and FY25 guidance slightly missed, according to RBC. However, quarterly growth and strong cash flow signal upside potential. The company produced 88,000 ounces in Q4, totaling 326,000 ounces for FY25.

- Orla Mining reported a pit wall failure at its Camino Rojo mine in Mexico, caused by heavy rain. The incident occurred on the north wall, an area planned for future layback and processing. Pit monitoring systems detected the issue early; no injuries, equipment damage, or environmental harm occurred, but mining has been temporarily suspended, according to Scotia.

Opportunities

- Intermediate gold equities are trading at 0.98x P/NAV—an 18.3% discount to senior golds. Mid-tier gold equities trade at 0.84x P/NAV, a 14.3% discount to intermediates and 30.0% to seniors. Stifel notes the market significantly discounts gold equities’ leverage to gold prices and underappreciated discovery and exploration optionality.

- Sibanye has agreed to acquire U.S. metals recycler Metallix Refining for $82 million in cash, with the deal expected to close in Q3 2025 pending regulatory approval.

- Equinox Gold announced CEO Greg Smith’s departure. Darren Hall, formerly President and COO, is the new CEO, and David Schummer is the new COO. Darren, with strong operational experience, plans to focus on disciplined execution as Greenstone and Valentine advance toward production, according to Scotia.

Threats

- Fresnillo’s attributable silver production (including Silverstream) was 12.5 million ounces in Q2/25, up 1% quarter-over-quarter but down 15% year-over-year, falling 6% short of Scotia’s 13.3-million-ounce forecast. Management reiterated 2025 silver production guidance of 49–56 million ounces and maintained 2026 and 2027 guidance.

- Franco Nevada announced the acquisition of a 1% royalty on the Arthur Gold Project in Nevada (formerly the Expanded Silicon Project), operated by AngloGold, for up to $275 million. RBC views the deal as requiring high gold price assumptions and optimistic development to yield reasonable returns but notes its overall materiality to the company is low.

- Aya reported second quarter silver production of 1.04 million ounces at its Zgounder Mine, slightly below Scotia’s 1.09-million-ounce estimate, due to lower mill grades partially offset by better throughput and recoveries.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2025):

SkyWest Inc.

Ryanair Holdings

Delta Air Lines

Alaska Air Group

United Airlines

Weyerhaeuser Co.

GE Vernova

TotalEnergies SE

Steel Dynamics Inc.

Freeport-McMoRan Inc.

Barrick Mining Corp.

NGEx Minerals Ltd.

Exxon Mobil Corp.

Osisko Development Corp.

Newmont Corp.

Valterra Platinum Ltd.

Orla Mining Ltd.

Westgold Resources Ltd.

Fresnillo PLC

Franco-Nevada Corp.

Aya Gold & Silver Inc.

Sibanye Stillwater Ltd.

Anglogold Ashanti Plc

Ferraro

Tesla

Remy Cointreau

LVMH

Laopu Gold

Volkswagen

Mercvedes-Benz

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting our prospectus page or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All