A major benefit of municipal bonds, or "munis," is that the interest they pay is generally exempt from federal income taxes. They're also generally exempt from state income taxes if the issuer is from the investor's home state. That may seem like a compelling argument for sticking with in-state munis. However, many muni investors may benefit by diversifying outside of their home state, even if it results in a higher state tax bill.

We've identified five factors when it could make sense to consider munis from other states. After considering all five, we think that muni investors in all states, with the exception of two high-tax states—California and New York—could benefit from investing in a national, not state-specific, portfolio of muni bonds. Even investors in California who are not in a high state tax bracket could achieve higher after-tax yields by diversifying nationally.

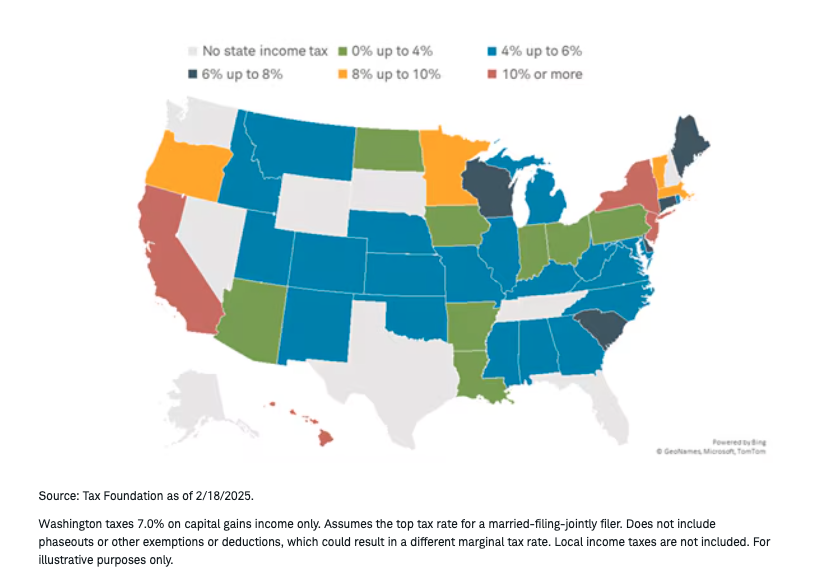

1. You live in a state with low or no state income tax.

If you live in a state with low or no state income tax, you will likely benefit from diversifying your muni portfolio with munis from issuers outside your home state.

The map below shows the maximum marginal income tax rate by state for married taxpayers filing jointly.

Investors in states with low or no state income tax could benefit from out-of-state munis

For investors in states with no state income taxes, like Florida or Texas, there's no state tax benefit to staying within your home state. For investors in California, on the other hand, the benefit can be large because the state tax rate is the highest in the country—13.3% for the top bracket. Therefore, it may make more sense if you're in a high-income-tax state to buy bonds issued in your home state, all else being equal.

In some instances, some states tax in-state bonds in the same manner they tax out-of-state bonds. For example, bonds issued by municipalities in Illinois are often subject to state income taxes—even if the tax filer is a resident of Illinois. In other words, Illinois investors don't necessarily save on their state income tax bill by holding Illinois munis. The rules can get complicated at times, so it makes sense to consult with your tax advisor.

2. You could earn a higher yield, even without state tax breaks.

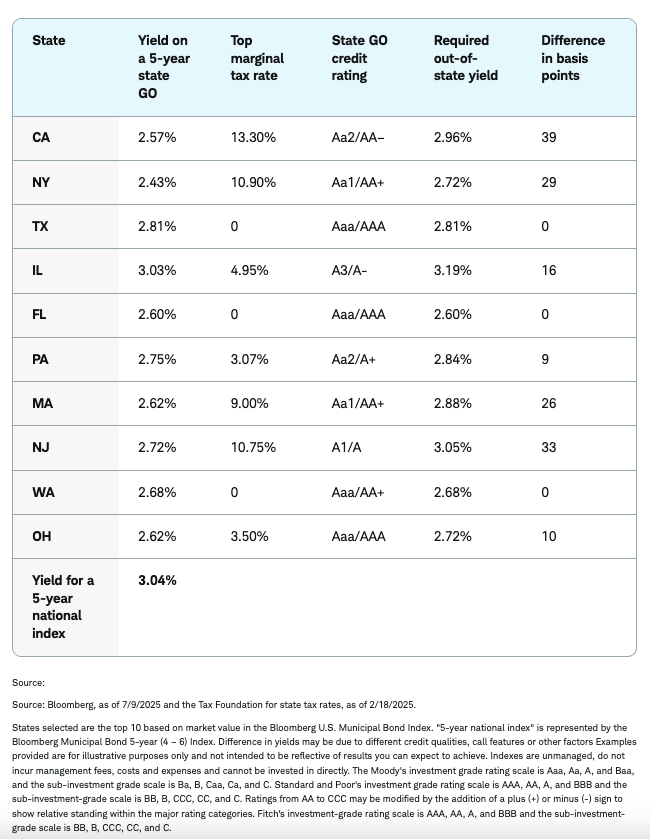

Some out-of-state muni bonds offer higher yields than in-state munis, even after accounting for any state income taxes.

It depends on where you look, though. The table below shows the yields investors in certain states would have to earn on out-of-state munis compared with the yield on an index of five-year general obligation munis issued by their home state to compensate for the lack of state income tax breaks. This assumes the investors are in their home states' highest marginal state tax bracket. The difference in yield is expressed in basis points (a basis point is one hundredth of one percent, or 0.01%). Florida, Texas, and Washington don't have state income taxes, so there's no spread.

Investors in various states would have to earn higher yields on out-of-state munis to make up for a lack of state income tax breaks

For example, the yield on an index of five-year general obligation bonds issued by the state of California is currently 2.57%. An investor in the highest marginal state tax bracket (which, in California, is 13.3%) would have to earn a yield of at least 2.96%—or 39 basis points more—on a bond from outside of California to achieve the same after-tax yield as on the in-state bond. It may be possible to achieve this higher yield if you invest in a bond issued by the state of Illinois, for example. However, Illinois has a lower credit rating than the state of California, and lower ratings imply higher credit risk.

Using a different example, an investor in the top marginal state tax bracket in Massachusetts would need to earn a yield of at least 2.88% to achieve the same after-tax yield as on the in-state muni. That's possible by investing in a nationally diversified index of munis with a similar maturity. However, the nationally diversified index may also contain lower-rated issuers, so it may not be a perfect apples-to-apples comparison.

3. You live in a state with few choices.

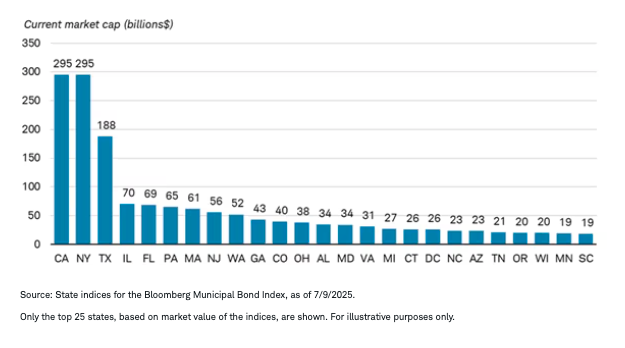

We recommend holding at least 10 different bonds from issuers with dissimilar credit characteristics, to create sufficient diversification in a portfolio of individual bonds. This could be difficult if your home state has a relatively small number of issuers with similar risks, but easier to achieve in larger states such as California, New York and Texas, which have many issuers. In fact, bonds from California, New York, and Texas account for approximately 44% of all issuers in the Bloomberg U.S. Municipal Bond Index. But in-state diversification is difficult for smaller states—as the chart below shows, many states have a small number of issuers based on the market value of bonds outstanding.

Bonds from California, New York, and Texas account for the vast majority of munis outstanding

4. You may find more highly rated issuers by searching nationally.

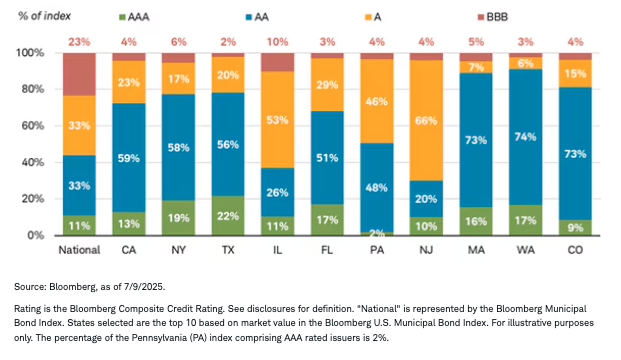

We suggest focusing on an average credit rating of AA/Aa for an attractive balance of risk and reward in today's environment. That means having some lower-rated (A/a or below) munis, but the bulk of the munis in your portfolio should carry higher ratings. It's easier to find highly rated munis if you live in a state like California, New York, or Texas, where there are large numbers of bonds rated in the AAA and AA categories, as illustrated in the chart below. It's more difficult if you live in a state like Illinois, Pennsylvania, or New Jersey, where the majority of bonds are lower than AA rated. Consider diversifying nationally if you live in a state with fewer highly rated options.

California, New York and Texas have high percentages of highly rated bonds

5. You live in a state where issuers face similar risks.

There are approximately $4.1 trillion of muni bonds outstanding1 spread among tens of thousands of issuers, and the credit quality of each state and issuer is affected by different factors. Even if you live in a state with many highly rated issuers, it could be beneficial to diversify nationally because those highly rated issuers are subject to similar credit risks, such as economic, political, and demographic risks. Credit quality is generally stronger in areas with steadily increasing populations, skilled workforces and diverse economies.

Although historically it has been rare for municipalities to fail to pay interest or make principal payments on time, it does occur occasionally. If the conditions in your home state, or regions of your home state, aren't favorable, other states' bonds might be more appealing.

Summing it all up

Considering all five factors, we generally suggest investors in all states other than New York and California consider munis outside of their home state. Investors in higher tax brackets in California and New York may benefit from investing in an all-in-state portfolio because of high state income tax rates and access to many different issuers with different credit risks. However, even investors in New York and California who are not in high state income tax brackets could achieve higher after-tax yields combined with greater diversification by diversifying nationally.

As always, your individual situation may vary. So choose a single-state muni or nationally diversified portfolio of munis based on your needs and situation.

Schwab clients can log in to research individual municipal bonds, view pre-screened municipal bond exchange-traded funds (ETFs) on Schwab's ETF Select List® or municipal bond mutual funds on Schwab's Mutual Fund OneSource Select List.® For additional help in selecting an appropriate solution for your needs, a Schwab Financial Consultant or Fixed Income Specialist can help.

1Source: Bloomberg, as of 7/9/2025.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Charles Schwab & Co., Inc. (member SIPC) receives remuneration from fund companies in the Mutual Fund OneSource (R) service for recordkeeping and shareholder services, and other administrative services.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Investing involves risk, including loss of principal.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

All issuer names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and the Schwab Center for Financial Research does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

The information and content provided herein is general in nature and is for informational purposes only. It is not intended, and should not be construed, as a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager) to help answer questions about specific situations or needs prior to taking any action based upon this information.

The Bloomberg 5-Year (4-6) Municipal Index measures the performance of the investment grade, US dollar-denominated, tax-exempt bond market for those with remaining maturities of four to six years. The index includes four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and pre-refunded bonds. It is a market-value weighted index.

The Bloomberg Composite (COMP) is a blend of a security's Moody's, S&P, Fitch, and DBRS ratings. The rating agencies are evenly weighted when calculating the composite. COMP is the average of existing ratings, rounded down to the lower rating in case the composite is between two ratings. The Bloomberg Composite is not intended to be a credit opinion.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or 'Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Charles Schwab Corporation provides a full range of brokerage, banking and financial advisory services through its operating subsidiaries. Its broker-dealer subsidiary, Charles Schwab & Co. Inc. (Member SIPC), and its affiliates offer investment services and products. Its banking subsidiary, Charles Schwab Bank, SSB (member FDIC and an Equal Housing Lender), provides deposit and lending services and products.

This site is designed for U.S. residents. Non-U.S. residents are subject to country-specific restrictions. Learn more about our services for non-U.S. residents, Charles Schwab Hong Kong clients, Charles Schwab U.K. clients.

© 2025 Charles Schwab & Co., Inc. All rights reserved. Member SIPC. Unauthorized access is prohibited. Usage will be monitored.

© Charles Schwab

Read more commentaries by Charles Schwab