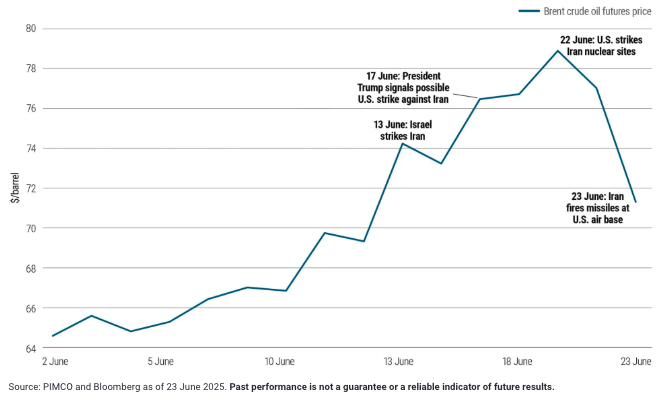

In the weeks leading up to last month’s Israeli and U.S. strikes on Iran, oil prices climbed – not due to actual supply disruptions, but in response to a geopolitical risk premium. Fears of a potential closure of the Strait of Hormuz drove market anxiety, though those concerns ultimately didn’t materialize. Iran’s muted response helped ease tensions, and the risk premium quickly unwound.

That said, the situation remains fluid. Ongoing concerns about Iran’s uranium stockpiles – and the possibility of further Israeli action – mean the geopolitical backdrop remains a source of potential volatility.

Oil prices experienced significant volatility

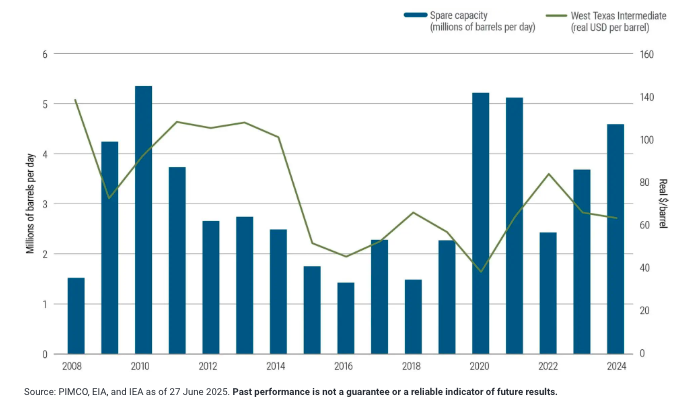

If tensions in the Middle East re-escalate and Iranian oil supply is disrupted, we could see another spike in oil prices.

But there are key stabilizers in place: U.S. shale producers can ramp up output given enough time, and OPEC currently holds significant spare production capacity. While that spare capacity remains largely tied up in regions recently impacted by conflict – limiting its near-term ability to reassure markets – it could serve as a longer-term stabilizer for supply dynamics.

These structural buffers may limit both the duration and the magnitude of any price rally.

So while short-term volatility is likely, we continue to expect oil prices to revert to the $60s range after any temporary spikes.

OPEC spare capacity

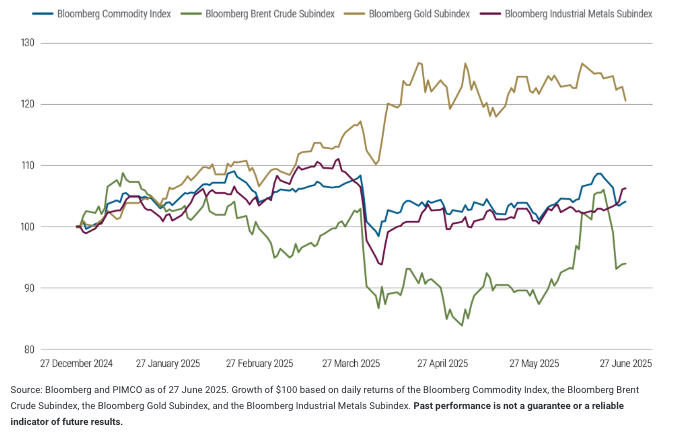

While oil has experienced notable volatility, the broader commodity complex has remained remarkably steady this year.

Gold prices continue to climb, supported by sustained central bank buying and ongoing de-dollarization efforts.

Base metals have also held firm, showing resilience even in the face of tariff-related growth concerns.

Investors, recognizing their portfolios were underexposed to real assets and more vulnerable to inflation than expected, have renewed interest in gold and broader commodities.

Overall, the Bloomberg Commodity Index has delivered strong returns – demonstrating that a diversified commodity basket has the potential to help weather sector-specific shocks and contribute to portfolio stability.

Growth of $100 for commodities

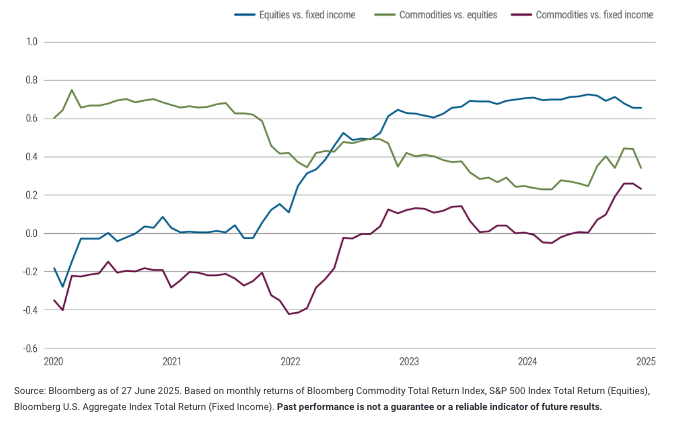

This diversification potential was also seen during the inflation spike in 2021–2022, when both stock and bond markets were challenged.

Commodities, however, maintained low correlations to both asset classes.

They have not only helped diversify portfolio risk but also enhanced inflation sensitivity – which we believe could make them a valuable option for strategic allocation in today’s environment of persistent inflation uncertainty.

Rolling 3-year correlations

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Past performance is not a guarantee or a reliable indicator of future results.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Performance results for certain charts and graphs may be limited by date ranges specified on those charts and graphs; different time periods may produce different results.

The Bloomberg Commodity Index is a diversified benchmark tracking futures prices of energy, metals, agriculture, and livestock commodities. The Bloomberg Brent Crude Subindex tracks futures prices of Brent crude oil within the Bloomberg Commodity Index. The Bloomberg Gold Subindex tracks futures prices of gold as part of the Bloomberg Commodity Index. The Bloomberg Industrial Metals Subindex tracks futures prices of key industrial metals like copper, aluminum, and zinc.

It is not possible to invest directly in an unmanaged index.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager, and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

Pacific Investment Management Company LLC (“PIMCO”) is an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”). PIMCO Investments LLC (“PIMCO Investments”) is a broker-dealer registered with the SEC and member of the Financial Industry Regulatory Authority, Inc. (“FINRA”). PIMCO and PIMCO Investments is solely responsible for its content. PIMCO Investments is the distributor of PIMCO investment products, and any PIMCO Content relating to those investment products is the sole responsibility of PIMCO Investments.

The information provided herein is not directed at any investor or category of investors and is provided solely as general information about our products and services and to otherwise provide general investment education. No information contained herein should be regarded as a suggestion to engage in or refrain from any investment-related course of action as none of PIMCO nor any of its affiliates is undertaking to provide investment advice, act as an adviser to any plan or entity subject to the Employee Retirement Income Security Act of 1974, as amended, individual retirement account or individual retirement annuity, or give advice in a fiduciary capacity with respect to the materials presented herein. If you are an individual retirement investor, contact your financial advisor or other fiduciary unrelated to PIMCO about whether any given investment idea, strategy, product or service described herein may be appropriate for your circumstances.

Check the background of this firm on FINRA's BrokerCheck.

Account Managers Compensation

PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2025 PIMCO. All Rights Reserved. Investment Products: NOT FDIC INSURED | MAY LOSE VALUE | NOT BANK GUARANTEED.

© PIMCO

Read more commentaries by PIMCO