2Q Earnings: The Beat Goes On?

Membership required

Membership is now required to use this feature. To learn more:

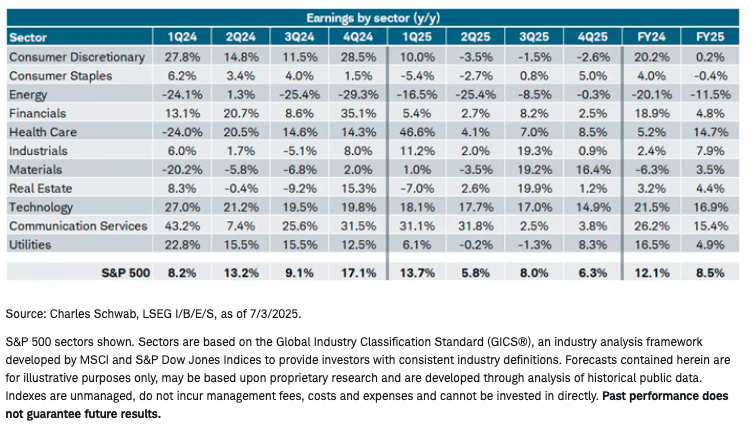

View Membership BenefitsThe second quarter 2025 earnings reporting season for the S&P 500 begins with investors facing a mix of slowing earnings momentum, ongoing macroeconomic uncertainty, and high expectations for the Technology and Communication Services. As detailed below, second quarter earnings are expected to rise less than 6% year-over-year, with wide sector divergences persisting. Strong year-over-year growth is expected for Communication Services (32%) and Technology (+18%), offset by notable weakness in Energy (-25%). Technology sector earnings are expected to remain strong throughout this year, while Communication Services' growth is expected to slow significantly in the second half. On the other hand, the laggard Energy sector's growth rate is expected to improve as the year progresses.

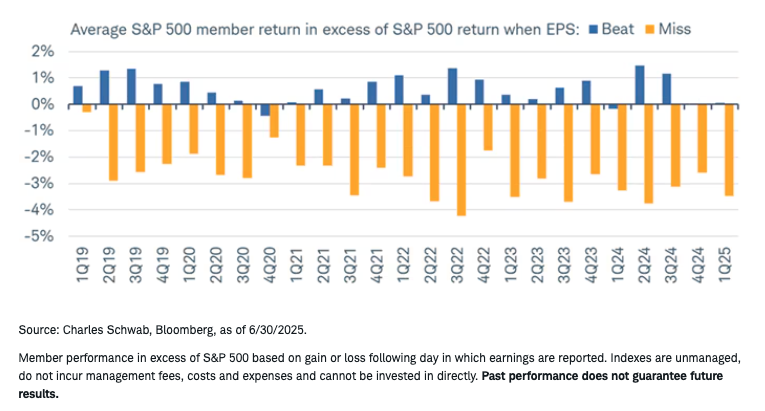

Guidance and earnings surprises will take on heightened importance as markets remain sensitive to forward-looking commentary, especially amid policy uncertainty and instability related to trade, tariffs, and interest rates. There is also increased attention being given to stocks of companies that don't meet or beat consensus estimates. As shown below, post-earnings stock price performance (for the first trading day following releases) remains asymmetric, with much stronger downside reaction to misses than upside to beats.

Misses get beaten

No extrapolation

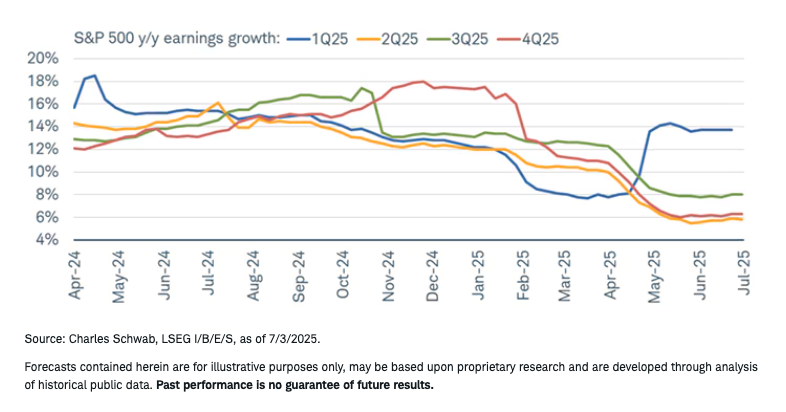

Second-quarter earnings follow what were very strong earnings in the first quarter, relative to where expectations were at the start of that reporting season. You can see the hook higher in the blue line in the chart below. Estimates were for less than 8% before first quarter reporting season began in April—a bar set too low given the ultimate growth rate of nearly 14%. However, as shown, analysts have not extrapolated that stronger growth into the remaining quarters this year. That suggests policy-related uncertainty and instability continues to cloud the outlook; but could also mean the bar has been (yet again) set too low as we move into the meat of second quarter reporting season.

Q1 strength not carrying

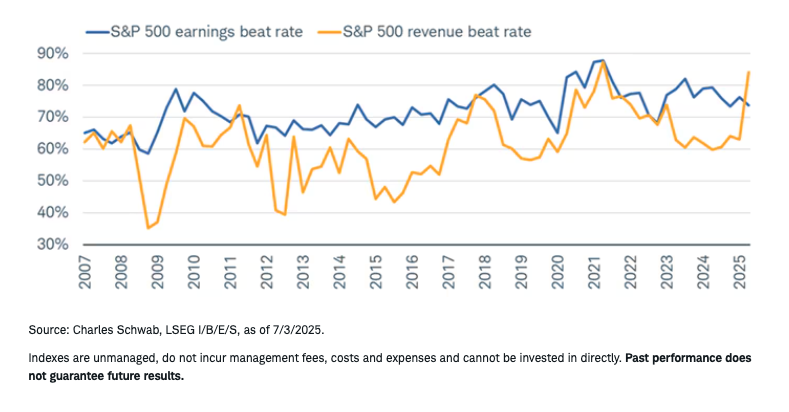

Incorporating the actual releases from the small percentage of S&P 500 companies having already reported second quarter results, and as shown below, the revenue beat rate has soared above the more muted earnings beat rate. It's too early to state with any certainty, but what would be suggested by a continued divergence between the two is that profit margins may be coming under increasing policy-related pressure.

Divergence between revenue and earnings beat rates

Guide us

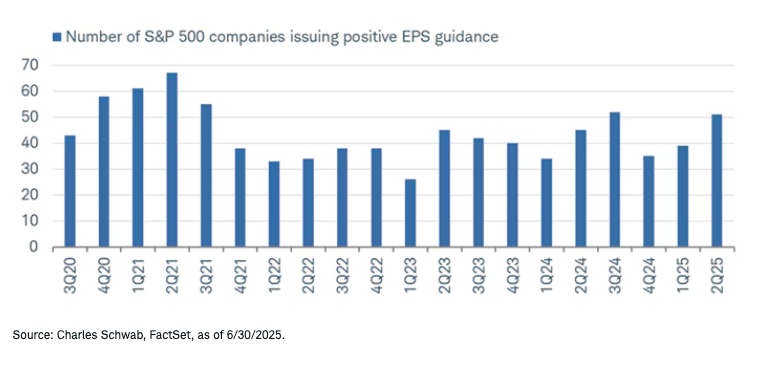

Building on the momentum from the first quarter of the year, the number of companies issuing positive EPS guidance for the second quarter has picked up sharply. Per data from FactSet through the end of June, more than 100 S&P 500 companies issued guidance for the second quarter—51 of which issued positive guidance, shown in the chart below. So far, that's above both the five-year average of 42 and 10-year average of 39.

In terms of tariffs' impact on companies' bottom lines, we can say so far, so good. In fairness, second-quarter results are unlikely to incorporate the full tariff effect, given the many pauses that were enacted for certain countries and sectors; as well as the fact that the effective U.S. tariff rate hadn't yet reached double digits by the end of May.

Jump

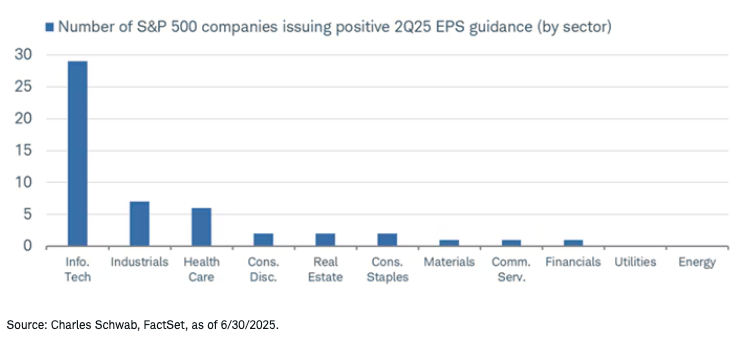

Most of the jump in positive guidance has been driven by the Technology sector, which has nearly 30 companies issuing positive guidance for the quarter. In contrast, the next highest number is seven for the Industrials sector, as shown in the chart below. Also worth mentioning is that Technology has seen the largest increase in the number of companies issuing negative guidance for the quarter—but importantly, the current total of 16 is below the five-year average of 20.4.

Tech driving revisions higher

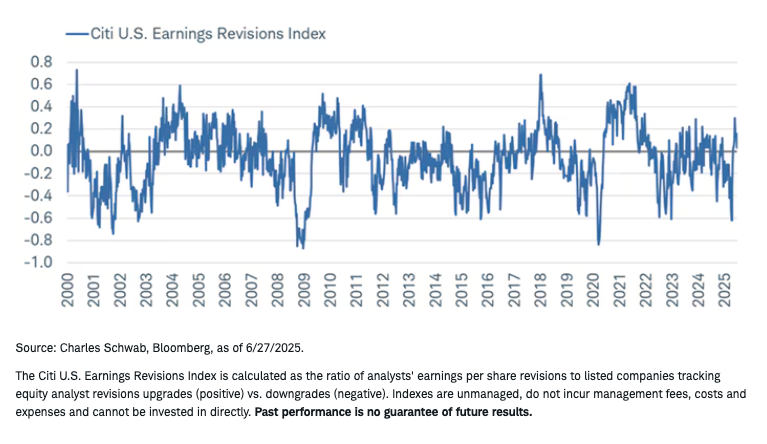

Putting the guidance picture together, much like the stock market over the past couple months, things have improved sharply. As shown below, Citi's U.S. Earnings Revisions Index (ERI) has jumped back into positive territory after falling to its lowest level since the 2022 and pandemic bear markets.

Lean back (into positive territory)

In sum

Analysts continue to expect growth in corporate earnings, but as we head into the beginning of reporting season, estimates remain tepid for the second quarter. If companies manage to step over a low bar and (in aggregate) maintain a fair degree of confidence when it comes to policy risks, we could face a repeat of the first quarter—during which the blended growth rate moved higher throughout the season. As pointed out in our midyear outlook, however, the economy still faces several headwinds. Ultimately, earnings will be the lens through which we can judge its resilience in the face of tariffs, higher rates, and a slowing labor market. So far, so good; but we think the bulk of the market's focus will be on forward guidance as opposed to backward-looking results.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, municipal securities including state specific municipal securities, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Diversification and asset allocation strategies do not ensure a profit and do not protect against losses in declining markets.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

Investment and Insurance Products Are: Not FDIC Insured • Not Insured by Any Federal Government Agency • Not a Deposit or Other Obligation of, or Guaranteed by, the Bank or any of its Affiliates • Subject to Investment Risks, Including Possible Loss of Principal Amount Invested

The Charles Schwab Corporation provides a full range of brokerage, banking and financial advisory services through its operating subsidiaries. Its broker-dealer subsidiary, Charles Schwab & Co. Inc. (Member SIPC), and its affiliates offer investment services and products. Its banking subsidiary, Charles Schwab Bank, SSB (member FDIC and an Equal Housing Lender), provides deposit and lending services and products.

This site is designed for U.S. residents. Non-U.S. residents are subject to country-specific restrictions. Learn more about our services for non-U.S. residents, Charles Schwab Hong Kong clients, Charles Schwab U.K. clients.

© 2025 Charles Schwab & Co., Inc. All rights reserved. Member SIPC. Unauthorized access is prohibited. Usage will be monitored.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All