Performance Commentary

This quarter might best be described as the “Big Beautiful Bounce”. Or the BBB. History has proven time and time again that markets do come back – but this was a historically quick market turnaround. We think that bodes well for the rest of the year – but that doesn’t mean investors should take off their seatbelts.

Fund Inception 8/18/05. Portfolio performance reflects Broadleaf’s Growth Equity Composite, described more fully under the caption “Performance Disclosures.” You are urged to read that information in its entirety in connection with any evaluation of Broadleaf’s performance statistics. All figures are shown net of actual fees. Any assumed fees have been calculated on a pro forma basis, reflecting the highest fee levels that Broadleaf would charge clients per our disclosures in Part II of our Form ADV.

Market Review & Outlook

What is the value of information?

In the digital age, data, or information, has been likened to digital gold. It’s everywhere around us, and for companies hoping to harness the power of AI, the first and most important step is getting their data aligned—a fancy way of saying “organized.” Palantir, a leading AI and data company, calls this process ontology, which is essentially a giant org chart for how and where information flows.

If that still sounds abstract, think of it like this: many companies are like third graders who just dropped their overstuffed binders in the hallway—papers everywhere, scrambling to get sorted before the next bell. In the current state, it is likely that the wrong papers are brought to the next class. We aren’t even sure if kids still learn using paper and pencil, but nevertheless, the world has become obsessed with organizing their messes of information and data.

But not all information is created equal.

Take it from me: our basement recently flooded during one of Ohio’s seemingly never-ending summer storms. I had to learn quickly what to do—cut the electricity, avoid standing water, and test the well afterwards (sure enough, the water came back positive for E. Coli - yuck). This might be second nature to others, but not to a first time homeowner.

On the other hand, I also recently learned that Albert Belle was snubbed for the AL MVP in 1995—the year I was born. As a diehard Cleveland baseball fan, this may help you impress your friends, but is not especially useful unless you're a baseball historian in Cooperstown.

In this age of information overload, the real challenge is discernment. Or knowing what matters. One blog post I read made me laugh—an AI model, asked to run a beverage company, got confused by a customer’s novelty order for a tungsten cube. Rather than ignoring the outlier, the model placed a full purchase order for more tungsten cubes, bankrupting the business. It mistook noise for signal—something most humans would instinctively recognize.

That’s the key: wisdom is learned experience. It’s knowing which signals matter, and which are just static. It remains to be seen if machines can develop this kind of judgment. They don’t feel the pressure of missing payroll or losing a customer, and thus, they don’t really learn from mistakes—at least not the way humans do.

So yes, AI may help us learn faster. But we believe businesses will only go as far as their employees will take them—especially when making high-stakes decisions. Most real-world problems live in the messy space between what you can learn from a textbook and what only comes with experience. And – maybe I am old school, but a smile and a handshake still goes a long way.

In terms of the economy – employment is definitely in a better balance. Inflation remains under control thus far, in spite of tariffs. Employees don’t quite have the upper hand that they have gotten used to over the last few years, and are being sent back to their offices in droves. At the same time, companies have avoided significant layoffs, as they remain uncertain about the future. Future hiring plans are on pause. Some have started to blame AI for the weakening, but we think it is too early to substantiate this. If you are a job seeker – none of this talk of averages or big picture matters, it’s not easy to find a job, and we empathize with you.

To the recent grads out there: if you're feeling anxiety about the future, you’re not alone. You can’t change the job market that you come into. But more often than not, technology ends up being an enabler, and the younger generations are always best equipped to help organizations implement technological change. At the same time, in a digital world, soft skills and relationships matter more, not less—it doesn’t cost anything to be kind and have a good attitude.

Perhaps it is an interesting parallel that as fewer of us work in fields that require physical labor, many of us now have to schedule movement—gym memberships, workouts, and walks that our ancestors got by simply living – hunting, farming, and commuting. Perhaps the same will happen with scheduling tedious mental activity. Crosswords and Sudoku just may replace monthly close processes and manual data entry. While we might mourn routine for a while, at the same time, our descendants will equally likely view us as crazy.

All of this is to say – 2025 has been a roller coaster year for markets. While discernment has been important, Patience is proving once again to be the most valuable investing virtue. Volatility has always been an inconvenient attribute of public markets, and in the world of immediate information and potentially even 24/7 markets, we don’t think this changes. We just ask that tariff announcements don’t interrupt our Fourth of July barbeques – it is a market holiday for a reason!

As always, we’ll continue to try our best to sift through the noise, apply the wisdom we’ve gained from touching our fair share of hot stoves, and patiently put our best ideas to work. Of our three cycles of value—Economic, Innovation, and Credit—you’ll notice there is no mention of a fourth: Geopolitical. While we will continue to monitor things closely, our past learned experience (wisdom) has taught us that patience through geopolitical events is often the best solution. We sure wouldn’t mind a little luck too!

Thanks, as always, for your trust and support. If you feel that we have done a good job for you, we would love to help any family or friends who could benefit from our investment management services, or perhaps a financial planning introduction.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

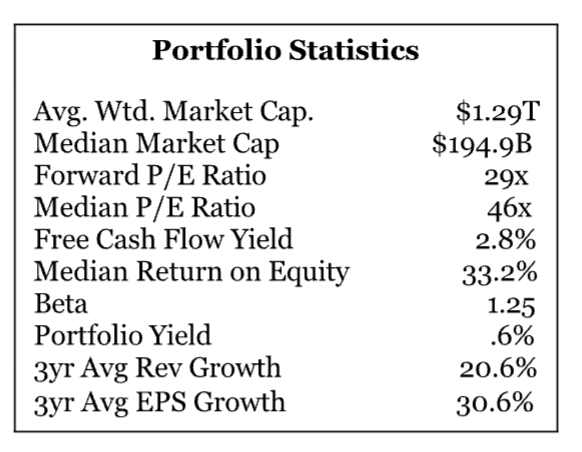

Portfolio Characteristics

Investment Style

The Broadleaf Growth Equity Portfolio employs a concentrated growth style of investing, holding approximately 25-35 equity positions from a cross section of economic sectors. Morningstar would classify us as a large cap growth manager, but we will invest in select small and midsize companies as unique opportunities avail themselves. Sector exposures are strongly influenced by our views on three determinants of investment value, which we define as the economic cycle, the innovation cycle, and the credit cycle. Individual securities are ultimately selected on the basis of their long-term growth potential, profitability, and intrinsic value as measured by their free cash flow generating characteristics. Innovative new ideas and themes are of particular interest.

Investment Objective

The portfolio’s goal is to provide equity like returns and to outperform the S&P 500 over a three to five-year time horizon or full market cycle, utilizing a growth oriented investment style. The portfolio is suitable for investors seeking an exposure to a concentrated investment style which may be more volatile than the market as a whole. Investors should consider it as a portion of their investment portfolio within the context of their overall asset allocation and related investment goals.

Performance Disclosures

Results reflect the actual performance of Broadleaf’s Growth Equity Composite. Performance data is shown net of advisory fees and trading costs. Broadleaf may charge different advisory fees to clients based on several factors, but primarily based on the size of a client’s account. Broadleaf’s basic fee schedule is available on its Form ADV, Part II. Results reflect the reinvestment of dividends and distributions, if any. Leverage has not been utilized. The U.S. Dollar is the currency used to express performance.

Broadleaf’s growth Equity Composite includes all fully discretionary accounts utilizing our growth equity style of investing with a minimum initial account size of $250,000. (From firm inception to 6/30/2009 our minimum account size for composite inclusion was $250,000 and from 6/30/2009 to 6/30/2013, the minimum had been $100,000. Historical results have not been updated retroactively to reflect changes in account minimums, but are reflected on a going forward basis.) To be included in the composite, an account must have been under management for at least one full quarter. If a significant cash flow in an underlying composite account during the quarter causes it to deviate from our intended growth style, we will remove the account for the period in which the significant cash event occurred. A significant cash flow is currently defined as 10% or more.

Total firm assets at quarter end were $534 million. Prior to January 5th, 2006 the firm did not have any investment advisory clients. As a result, composite data prior to March 31st, 2006 only reflects the performance of Doug MacKay’s personal retirement account.

The S&P 500 Index has been used for comparative benchmark purposes because the goal of the stated strategy is to provide equity-like returns and to outperform the S&P 500 over a three to five-year time horizon or full market cycle. The S&P 500 is a broad based index reflecting the performance of the equity market in general. The S&P 500 Index is based on total returns which includes dividends. We monitor the performance of our growth style of investing by comparing our results to those of other large cap growth peers. While we believe these are appropriate benchmarks to use for comparison purposes, it should be expected that the volatility of the Broadleaf Growth Equity Portfolio may be higher due to its concentrated nature.

Performance information since inception reflects actual performance of the composite over a period of greater than fifteen years. You are cautioned that information concerning comparative performance over this period of time may bear no relationship whatsoever to performance over other time periods. This information should not be regarded as in anyway representing the likely future performance of the portfolio in absolute terms or in comparison to the indices. Investment in securities, including mutual funds, involves risk of loss. Past performance is no guarantee of future returns. Yield should not be used as an indication of the income that has or will be received. We do not consider yield as performance but instead as an attribute relating to the income production profile of the portfolio and its underlying assets. Yield is shown without the deduction of fees and expenses. The overall effect of fees is best represented through the difference between gross and net performance.

Broadleaf Partners, LLC is a registered investment advisor with the Securities and Exchange Commission. The firm maintains a complete list and description of composites, which is available upon request.

Performance information contained in this document including any reference to the purchase or sale of a security, or a strategy, is not intended to constitute personalized investment advice. Personalized investment advice is always dependent on individual factors, involves risk and is not a guarantee that any investment will produce favorable results.

Read more commentaries by Broadleaf Partners