Dating back to medieval falconry, the proverb “a bird in the hand is worth two in the bush” suggests that one should be thankful for the sure thing rather than boastful gambling on the spectacular.

That theme of modesty over hubris has also been an important one within portfolio management. One might rephrase it as “a dividend in hand is worth two expensive growth stories.”

Investors’ guidelines regarding the basics of building wealth seem distorted by the current speculative period. As investors have done during other late-cycle and speculative periods, they are taking spectacular portfolio risk and ignoring the power of compounding dividends.

It might be an appropriate time to remember the proverb. Investors seem universally focused on “AI” which seems eerily similar to the “.com” stocks of the Technology Bubble and the “tronics” craze of the 1960s. Meanwhile, we see lots of attractive, admittedly boring, dividend-paying themes.

Utilities vs NASDAQ: Believe it or not, they’re neck-and-neck through time

One of the easiest methods for building wealth has historically been the power of compounding dividends. Compounding dividends is boring as all get out, but it’s been highly successful through time.

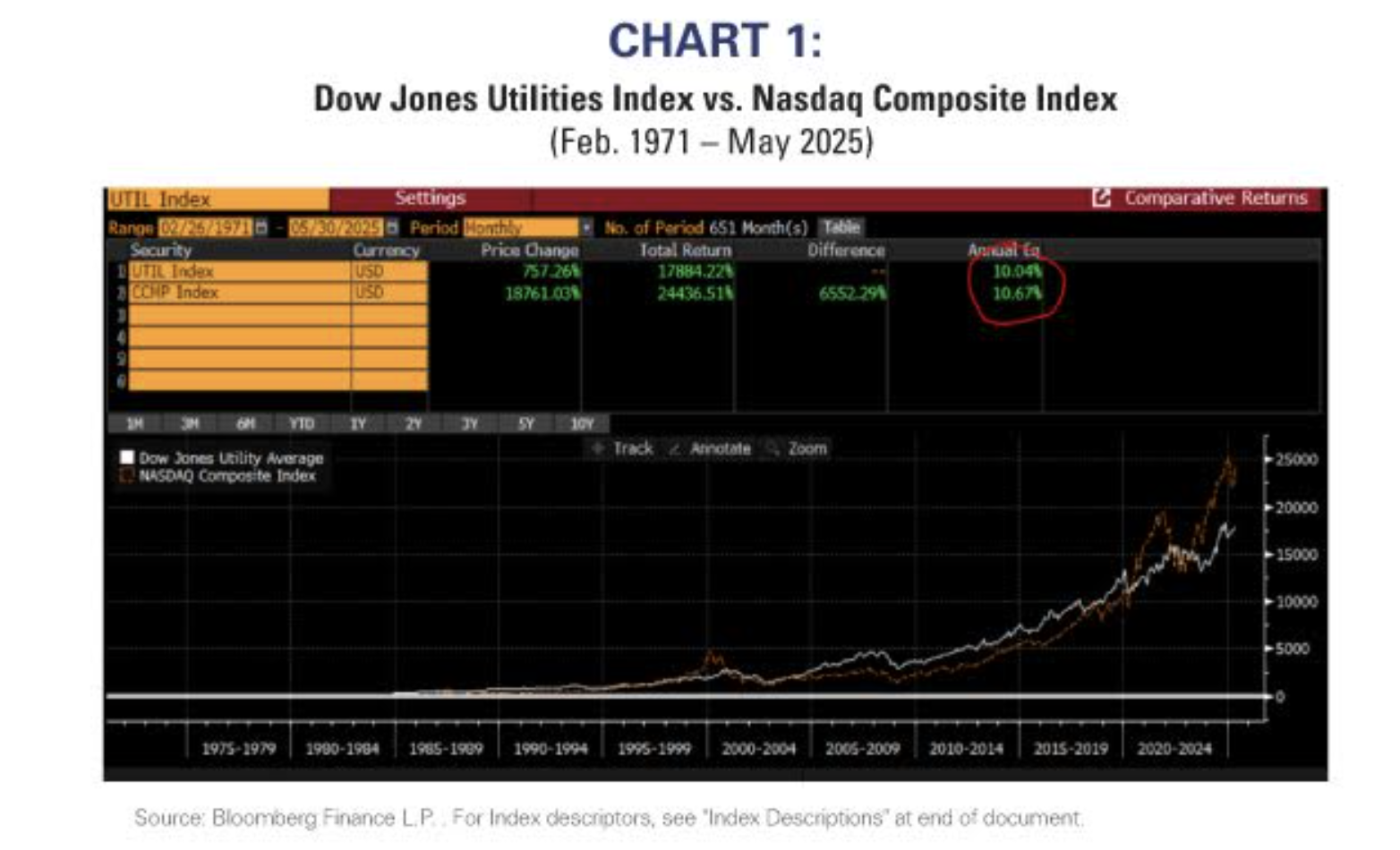

In fact, compounding dividend income has been so successful, that the Dow Jones Utilities Index’s returns have been roughly neck-and-neck with NASDAQ returns since NASDAQ’s inception in 1971!

Chart 1 shows the compound total return of the Dow Jones Utility Index versus that of the NASDAQ Composite since NASDAQ’s origination in February 1971. Several points are worth noting:

-

NASDAQ surges ahead of DJ Utilities only during more speculative periods and bubbles.

-

Utilities have underperformed NASDAQ by less than 65bp/year even when including the current speculative Magnificent 7/AI period.

-

Because such a large proportion of return comes from dividends, Utilities have achieved their returns with considerably lower volatility and beta.

-

The DJ Utilities Index has a beta of only 0.5 to the NASDAQ during the 50+ year period, implying its risk-adjusted returns are superior to those of NASDAQ.

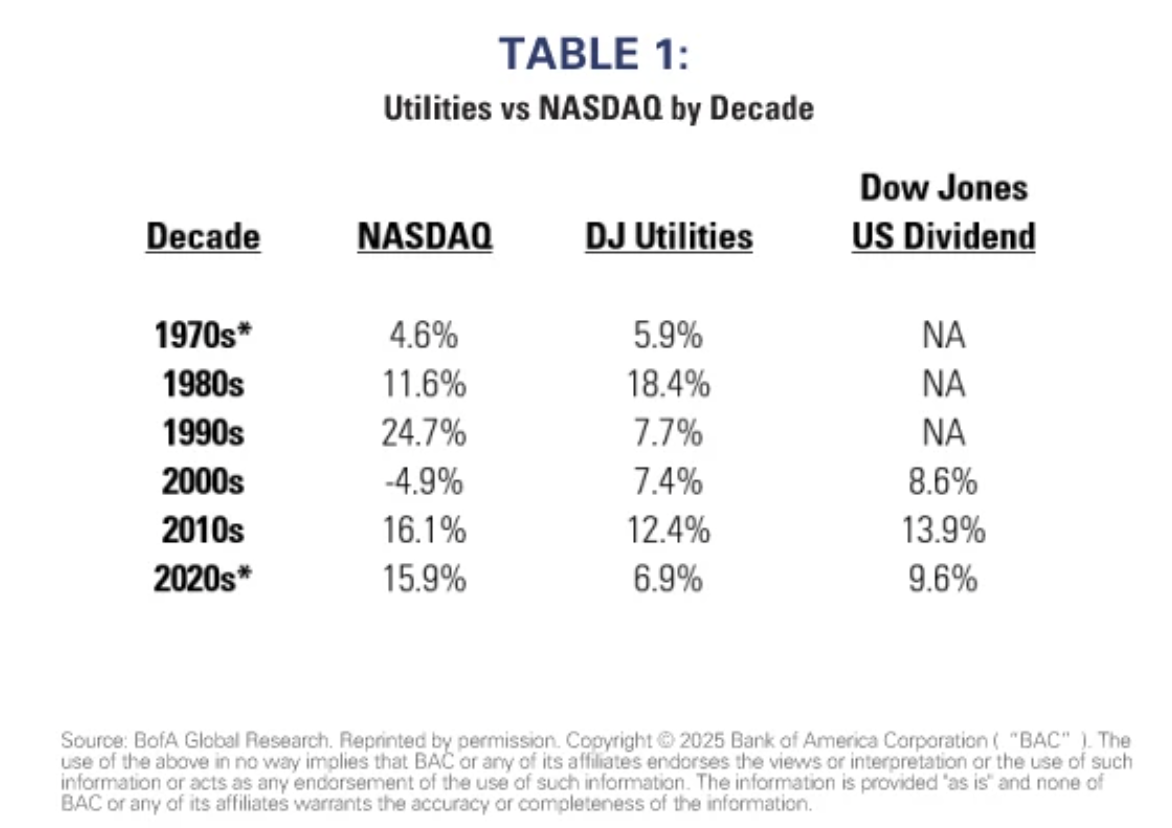

Table 1 breaks down the returns in Chart 1 by decade. Perhaps contrary to most investors’ current perceptions, Utilities outperformed NASDAQ during three decades and NASDAQ outperformed Utilities during three decades.

The table includes the Dow Jones US Dividend Index during the last three decades when it existed. This index is a broader representation of dividend-paying companies than simply utilities, and paints an even more appealing view of dividend-paying companies because it outperforms utilities during all three decades.

Investors currently want beta not yield

As we’ve pointed out many times, investors’ current appetite for beta risk seem insatiable. Whereas they were extremely hesitant to take any market risk at the beginning of the bull market, today (16 years later) they apparently can’t take enough.

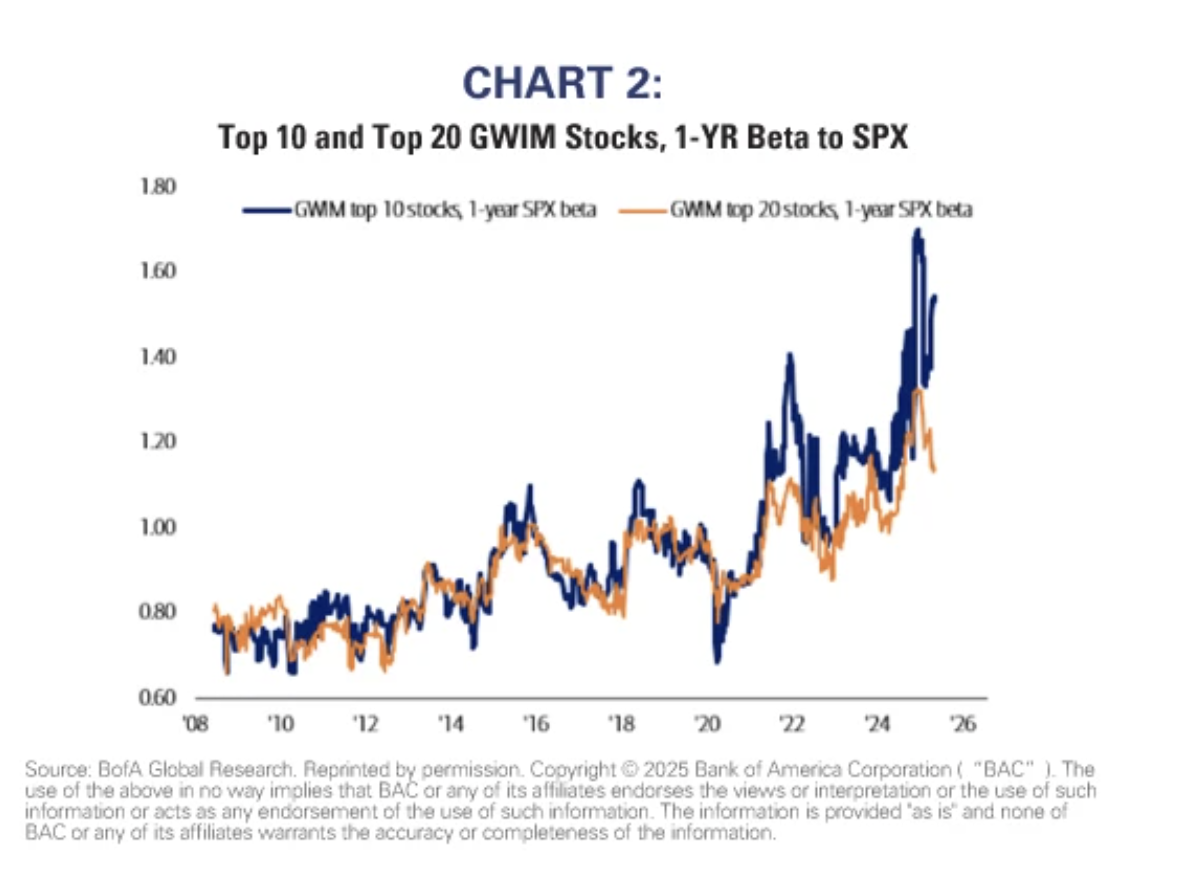

Chart 2 (courtesy of Michael Harnett at BofA Securities) is one we’ve published many times, and shows the beta of the major holdings in private clients’ portfolios. Regardless of whether one examined the top 10 or top 20 holdings, private client equity beta was roughly 0.75 at the beginning of the bull market. Today, the beta of their top 10 holdings is an eye-popping 1.5! Even the beta of the top 20 remains near historic highs.

Throughout the early portion of the 2010s, investors had interest only in “large cap high quality dividend-paying stocks”, because those stocks’ dividends and low betas were considered safer. Today, it seems as though investors are shunning dividends and are willing to take enormous beta risk.

A bird in the hand…

Investors tend to be out of step with the markets. At the beginning of a bull market when momentum and beta strategies are by definition most rewarded, investors’ fears leads them to emphasize dividends and lower-beta equities. In later-cycle periods when dividends and lower beta become more attractive, investors’ confidence leads them to risk-taking and momentum investing.

We have no idea when the bull market will end, and are not suggesting market-timing. However, we clearly are not at the beginning of a bull market and, as we’ve previously written, the profits cycle is starting to decelerate.

The combination of a late-cycle market and decelerating corporate profits suggests a bird in the hand might be worth two in the bush.

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Richard Bernstein Advisors

Read more commentaries by Richard Bernstein Advisors