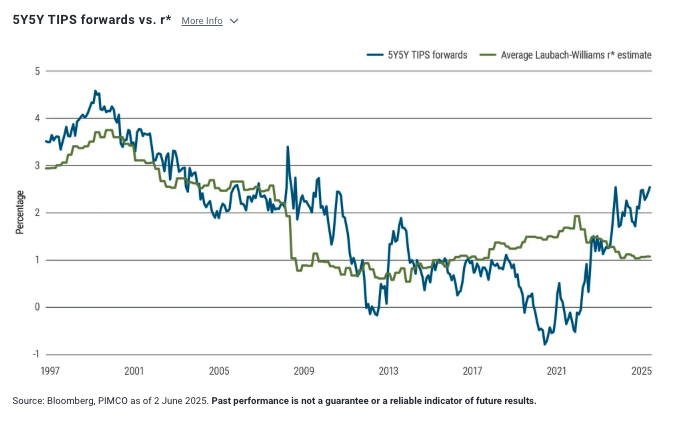

Recent rate volatility has left investors demanding clarity on the direction of yields and what fair compensation for risk-taking should be; but searching for answers when current environments do not seem to align with prior trends can be challenging. Over the past 25 years, the 5-year, 5-year forward Treasury inflation-protected securities (TIPS) yield has closely tracked the Federal Reserve’s estimate of the real neutral interest rate. That rate – commonly referred to as r* – is the estimated neutral or natural real interest rate that neither hinders nor stimulates economic growth, employment, and inflation. The close relationship between these two measurements reflects market confidence in the Fed’s long-term economic outlook.

However, in recent years, the 5Y5Y TIPS forward yield has risen above r*, suggesting that investors expect real interest rates to be higher over the medium term than the Fed’s benchmark, signaling in part a higher real term premium.

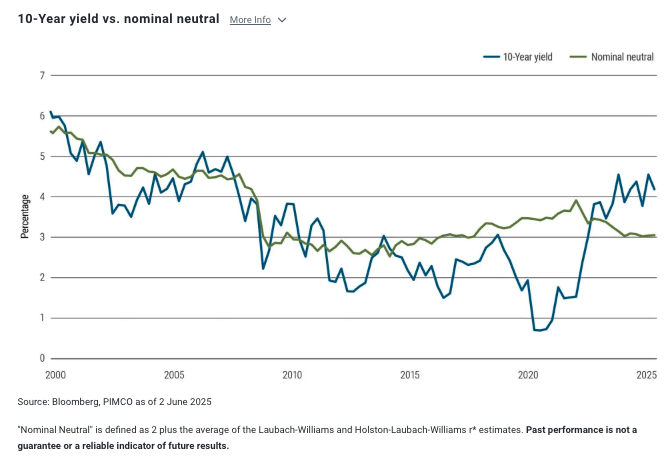

A similar trend is evident in the 10-year U.S. Treasury yield, which for decades remained anchored near the Fed’s nominal neutral rate.

Since 2021, however, the 10-year yield has risen while the neutral rate has fallen. In essence, investors are demanding higher returns for taking on the risks of longer-term borrowing along a steeper yield curve, especially in a world of challenging debt and deficit dynamics.

The rise in long-term yields could have broad implications, increasing borrowing costs for businesses and consumers and potentially hampering economic activity if sustained.

With this fragmenting environment in the backdrop, how should we think about valuing fair term premium?

The answer lies in the relationship between r* and term premium.

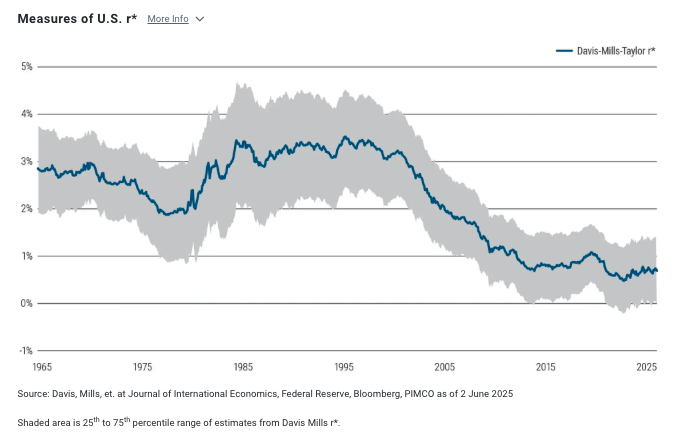

Despite these upward moves in nominal yields, the underlying real neutral rate (r*) has remained relatively steady, even declining slightly in recent years. This stability suggests that the fundamental drivers of economic growth and productivity have not dramatically changed.

Nominal bond yields can be thought of as the sum of expected average short-term real interest rates plus a term premium — the extra yield investors demand for holding longer-term bonds. The steady real neutral rate implies that much of the recent increase in nominal yields is driven by changes in the term premium rather than shifts in the core economic fundamentals.

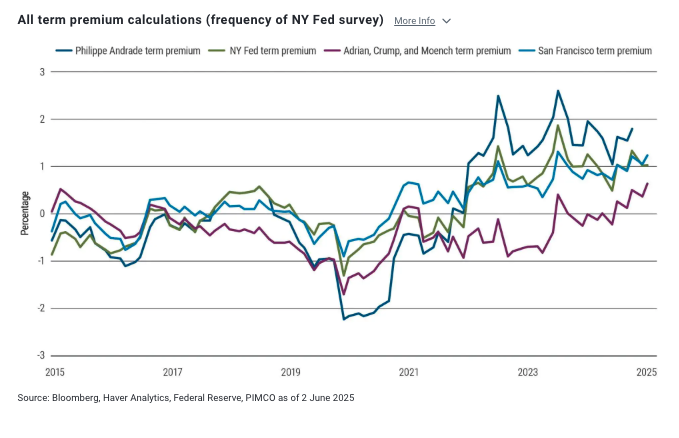

Indeed, the term premium has surged close to a 10-year high, reflecting heightened investor demand for compensation against risks such as inflation volatility, interest rate uncertainty, policy-related risks, and potential liquidity constraints in bond markets.

However, this is not a sudden or isolated event indicating market disruption; the multi-year rise in term premium suggests an orderly repricing of risk, which active portfolio management can help navigate. In particular, a fall in short term interest rates and a rising term premium signals that investors can look to lock in compelling yields over the intermediate term.

As we’re already beginning to see, economic cycles in this world are going to be amplified. Financial markets are going to be volatile. For an active investor, such environments are a playground for credit selection and strategic duration positioning opportunities.

Disclosures

Past performance is not a guarantee or a reliable indicator of future results.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Performance results for certain charts and graphs may be limited by date ranges specified on those charts and graphs; different time periods may produce different results.

It is not possible to invest directly in an unmanaged index.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager, and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2025-0624-4603701

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© PIMCO

Read more commentaries by PIMCO