The tide is turning in favor of emerging market (EM) local currency bonds.

In the face of the global financial rout triggered by President Donald Trump’s tumultuous first 100 days in office, the long-term prospects for the asset class have been steadily improving.

Favorable valuations, high carry, loosening monetary policy and the growing probability of a long-term decline in the US dollar are supportive. All of which suggest EM local currency should feature more prominently in global fixed income portfolios.

Some investors might find reasons to be cautious. Recent years haven’t been kind to the asset class after all. Due to the Covid crisis and the Ukraine war, EM local currency bond funds suffered outflows.

But several trends now seem to be firmly moving in their favor.

Take the US dollar. Its uncontested run of the past few years, supported by US exceptionalism, has been the single biggest negative contributor to the performance of EM local debt. Now, though, the greenback stands on shakier foundations. In our view, it has entered a period of structural weakness, not least because of the uncertain policy backdrop in the US.

Our fair value model shows that the dollar is 20 per cent overvalued against emerging market currencies relative to its long-term average.1

We believe this gap will narrow in the coming years, just as GDP growth differentials between emerging and developed economies widen further from the current 14-year high.

A weaker dollar should act as a magnet for international capital for emerging markets. Recent market turmoil emanating from the US has already encouraged investors to gradually diversify portfolios that had become too reliant on American assets. Data from the Bank for International Settlements shows that one standard deviation depreciation in the US dollar against advanced economy currencies in any one month increases investment flows to local currency EM bonds by as much as 0.29 percentage points.2

Aside from benign moves in the dollar, we also expect monetary conditions to loosen in favor of emerging economies, drawing in even more capital into local bond markets. Already, three quarters of the world's major central banks are easing monetary policy, with the three biggest – the US Federal Reserve, European Central Bank and the People’s Bank of China – all providing stimulus.

The emerging world’s inflation dynamics are also positive. The inflation rate in emerging economies has been falling every year since 2022 and price pressures are likely to ease further this year. Our leading indicators and proprietary inflation momentum tools suggest that emerging market inflation will likely fall below that of developed markets in the months ahead.

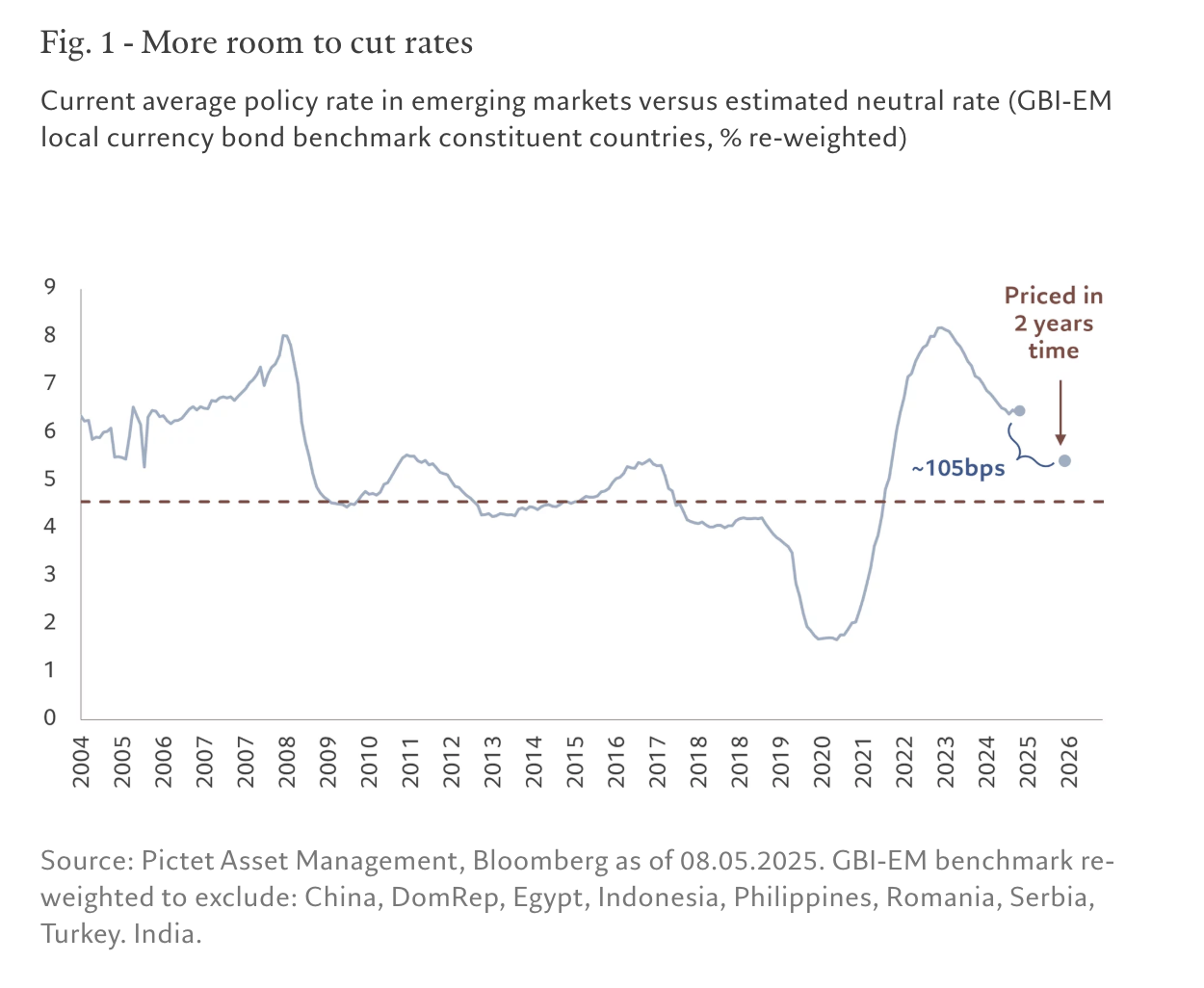

This should allow interest rates to fall further and faster across the emerging world. Many emerging market policy rates are above what we consider to be neutral levels (see Fig. 1). This rate is the sweet spot where the cost of borrowing is neither too restrictive nor too stimulative.

The real rate of the asset class – or the inflation-adjusted return investors can lock in – is likely to rise further from the current level, which is already well above its long-term average and that of developed market bonds.

Another boost to the asset class is China's economic recovery. China is beginning to see the fruits of a slow rebalancing of its economy in favour of domestic consumption. At the same time, Beijing has pledged to use fiscal and monetary policy levers in its toolkit to help offset the negative impact from US tariffs. The positive effect will spill over to the rest of the emerging world, particularly developing economies in Asia, which are China's largest trading partners and, just as importantly, represent nearly half of the EM local currency benchmark bond index.

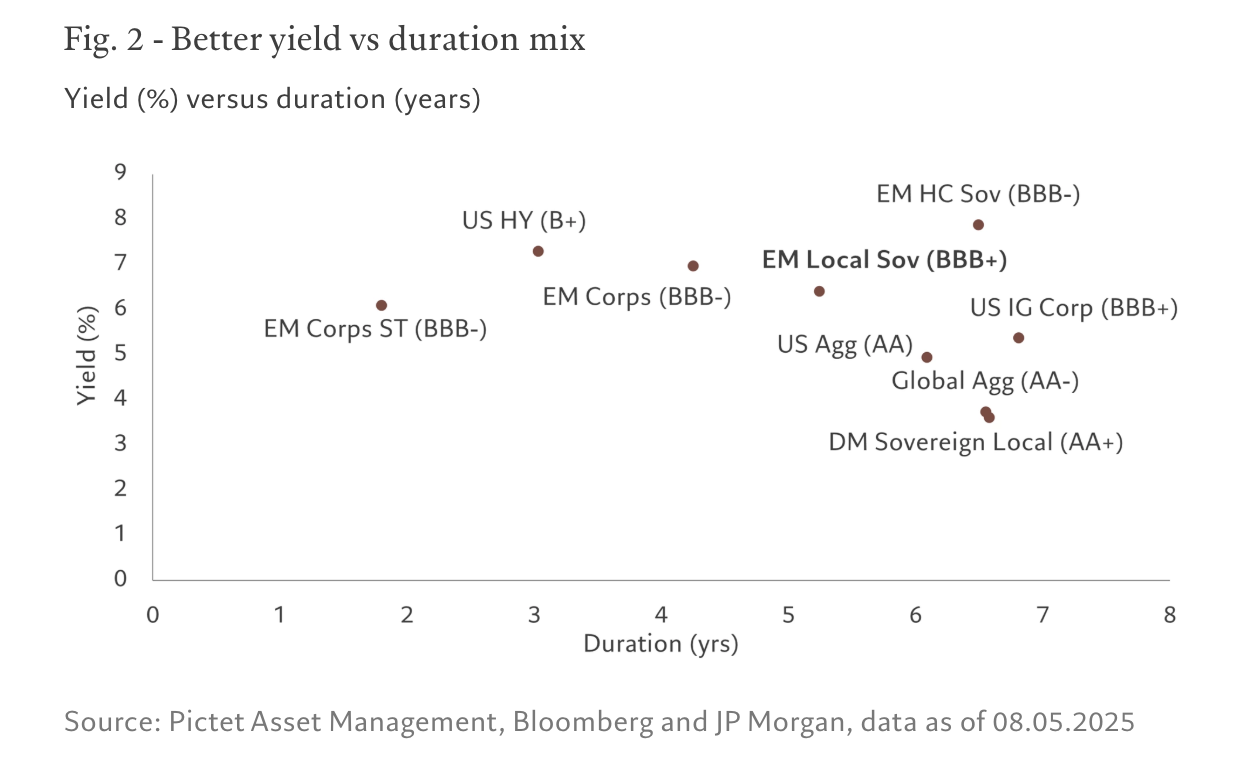

Attractive yield-duration mix

As each of these fundamental trends gather pace, EM local currency bonds' appeal as an alternative to developed market debt should grow. As Fig. 2 shows, the asset class already offers investors a higher yield and a lower duration risk than similarly-rated US investment grade bonds. (Duration indicates the expected percentage gain or loss in the capital value of a bond for every 1 percentage point fall or increase in its yield).

More predictable, more domestic

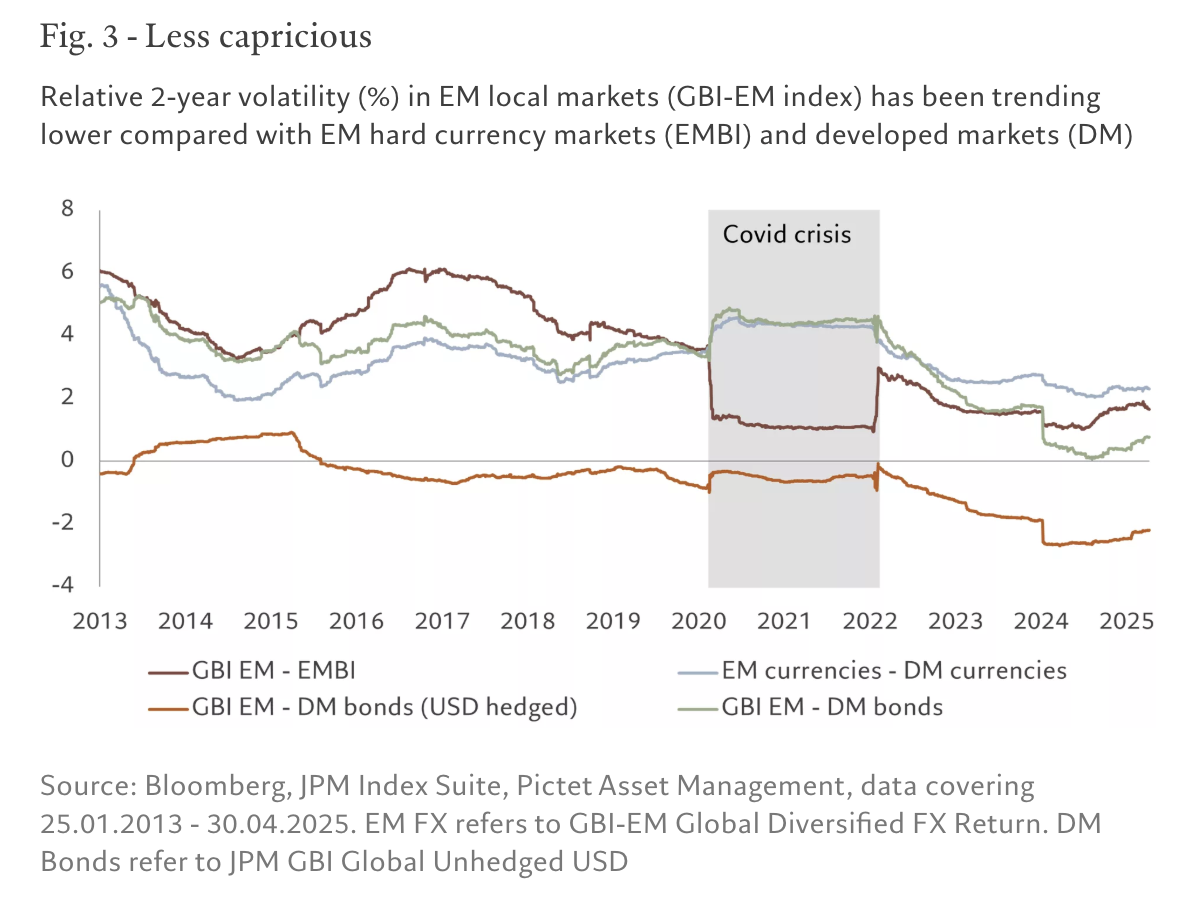

The asset class has seen a structural improvement in its governance, giving investors more reasons to be optimistic about emerging local bonds.

Effective monetary policy making, prudent fiscal measures and better coordination between policy levers have allowed emerging economies to become more predictable and credible. China’s ongoing coordinated easing is a case in point.

One measure of policy credibility – which evaluates how consistent and reliable a country’s economic policy is -- shows emerging economies are fast catching up with their advanced peers and narrowing a gap.3

Better policy credibility and higher economic growth have helped increase the local savings pools, encouraging domestic investors to save in local currencies and markets. A greater participation of domestic investors and the reduced reliance on external funding are positive for the asset class as it becomes less susceptible to external volatility.

All this is helping reduce volatility (see chart) in the long term, which adds to the appeal of the asset class.

With macroeconomic and structural factors all moving in its favor, it is time for investors to look again at EM local currency bonds.

1. Based on relative prices, relative productivity and net foreign assets, average of 31 emerging currencies

2. https://www.bis.org/publ/qtrpdf/r_qt2409d.htm

3. Sebnem Kalemli-Ozkan and Filiz Unsal, November 2023

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Pictet Asset Management

Read more commentaries by Pictet Asset Management