Quarterly Review and Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsConverging Forces

Five pivotal U.S. economic considerations, including tariffs, monetary policy, fiscal policy, debt overhang, and demographics, are aligning to depress economic growth for the balance of this year and into 2026.

- First, the recessionary effects of tariffs, supported by compelling historical evidence and economic theory, will dominate the inflationary ones, potentially leading to a significant reduction in world trade and capital flows.

- Second, the Fed's continued maintenance of a highly restrictive monetary situation is significant and could have severe implications. A significant reversal in Federal Reserve policies this year is necessary for economic acceleration in 2026.

- Third, current federal spending plus the lagged negative multiplier effects from 2021 to 2024 will reduce economic activity this year. Benefits from the presumed tax reductions will impact 2026, but their delay will cause fiscal policy restraint for 2025.

- Fourth is federal indebtedness. After an unprecedented surge, the existing level of government debt will continue to drain economic activity. This pattern of excess debt restraining growth has been observed throughout history and noted by such outstanding thinkers as David Hume and Adam Smith in the eighteenth century; David Ricardo in the nineteenth century; Nikolai Kondratiev, Irving Fisher, Charles Kindlelberger, and Hyman Minsky in the twentieth century; and Carmen Reinhardt, Vincent Reinhardt, Kenneth Rogoff (RRR), Andreas Bergh, Magnus Henrikson, and others in the past 25 years.

- Lastly, the border closing also poses a very consequential drag on near-term economic growth.

Tariffs

Unintended Consequences

The philosopher George Santayana's words, "Those who forget the lessons of history are doomed to repeat it," ring true in current economic policy. The currency devaluations by the Dutch East Indies and Australia in the late 1920s, which quickly led to multiple country currency devaluations, the Smoot-Hawley Tariff Act of 1930, and devaluations of the British pound and U.S. dollar, respectively, in 1930 and 1933, serve as stark reminders of the unintended consequences of economic decisions. Similar "beggar thy neighbor" (BTN) practices occurred until the start of World War II, contributing to deflation and severely suppressing world economic activity. Basic economic theory was at work. Except for energy products, the demand for nearly all internationally traded goods is price elastic. This price elasticity means, in percentage terms, the fall in demand will be far greater than the associated tariff-caused price increase, resulting in a drop in total revenue.

The world is witnessing a unique high-stakes game where every player wins or loses big. The winning prize moves the world in the direction of Ricardo's law of comparative advantage and Adam Smith's "invisible hand" and away from mercantilist practices which include undervalued currencies, subsidies, nonenforceability of contracts, use of child and convict labor, nonpayment of fees for patents and copyrights, and drug trafficking. With less mercantilist practices, a more efficient allocation of resources would reduce inflation, improve the standard of living, and start rolling back the debt trap. Continuing the present situation of mercantilist practices characterized by tariffs and retaliatory actions will mean a loss for all. In the 1920s-30s, as today, many foreign countries suffer from below-trend growth rates and cannot accept tariff hikes. Not surprisingly, retaliations against U.S. tariffs have started.

Capital Flows

A country's positive capital account is the inverse of a negative current account. If tariffs reduce the current account deficit, fewer foreign funds would be available for fixed investment and the U.S. budget deficit. Thus, tariffs could initiate a downturn in the international trade and capital flow sectors, significantly weakening economic growth.

Monetary Policy

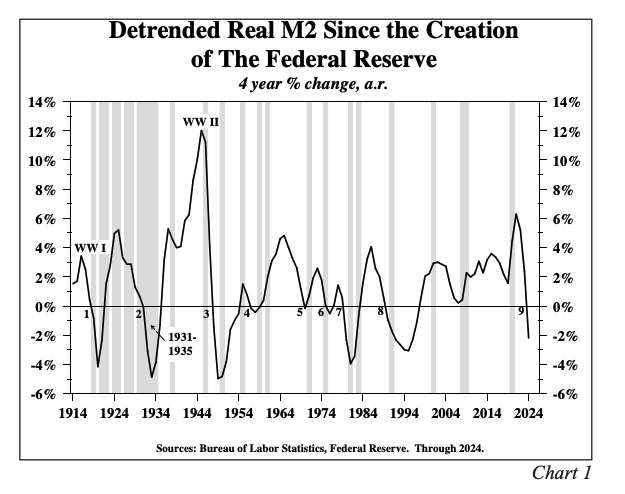

Since the Fed's first year of operation in 1914, the current four-year percent change for detrended real M2 is in its ninth fall into negative territory (marked as #9 in Chart 1). The second occurrence, marked as #2 Chart 1, is a highly relevant experience for the current situation. Money growth began decelerating sharply in the late 1920s and then turned negative from 1931-35. Then, aggregate demand faltered in response to repeated contractionary BTN measures and the depressive effects of extreme over-indebtedness. However, the Fed did not reverse the monetary contraction, for which it was subsequently excoriated by Nobel Laureate Milton Friedman and former Fed Chair Ben Bernanke.

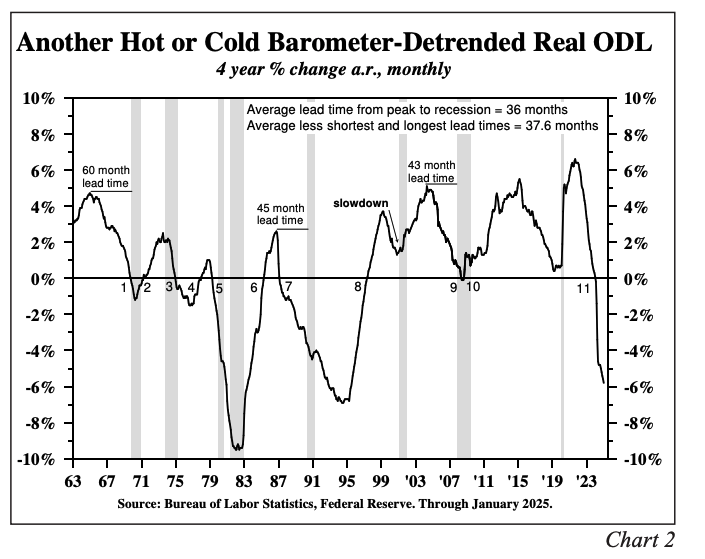

The lagged monetary restraint from 2022 is confirmed by the movement in the Fed's H.8 line item, Other Deposit Liabilities (ODL). As measured on a real detrended basis for the last four years, ODL, which decelerated before all recessions since 1961, has been negative since 2024 (Chart 2).

In recent times, Fed leaders have reiterated that they are data dependent. The experience of a century ago is that tariffs are recessionary but even more so when real money growth contracts. In such circumstances, the Fed should be preemptive, act before data confirmation and speed support to the economy.

Modestly higher commercial bank deposits from the middle half of the fourth quarter of 2024 into the first quarter don't alter the picture. Banks helped fund the buy-in advance phase ahead of March/April tariff increases. As the tariffs take effect, deposits and spending should simultaneously fall back while being reinforced by a decline in Modernized World Dollar Liquidity.

Fiscal Policy

Expenditures

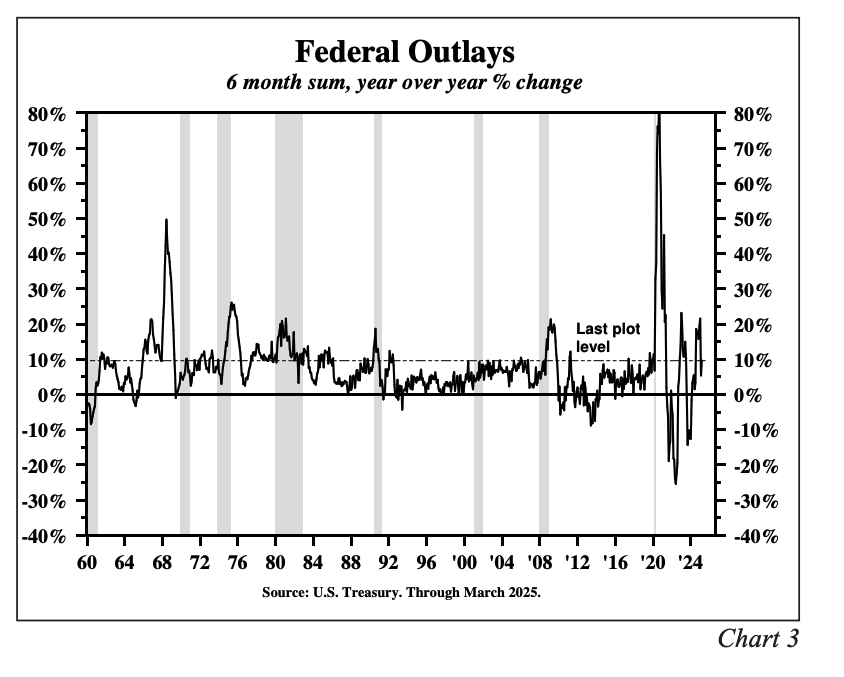

Federal spending exploded during the Pandemic, with year-over-year increases as high as 76% (Chart 3). Wrightson's Lou Crandall, an outstanding budget analyst, calculates that outlays will increase by 6% for FY2025. Since the increase for the first six months of FY2025 was a very fast 9.7%, nominal spending for the final six months will be flat. Such a considerable redirection will cut into economic growth.

The fiscal spending multiplier is positive for the first four to six quarters after an expenditure. Then, the multiplier reverses direction and diminishes growth over three years. Accordingly, the multipliers from the massive fiscal stimulus pumped into the economy before the second half of 2024 have now turned negative, a significant growth inhibiting development. By mid-2025, the enormous jump in federal outlays in the second half of 2024 will impair growth.

Taxes

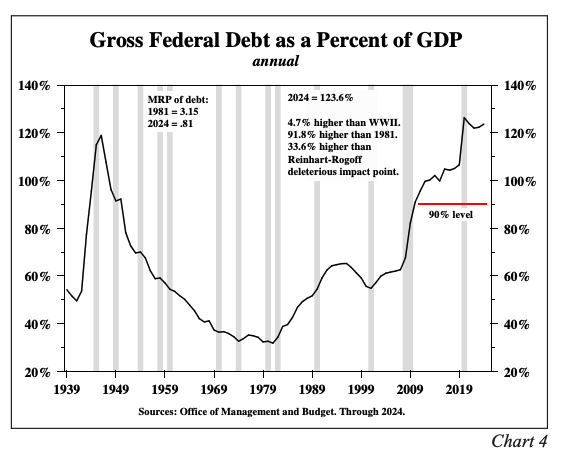

The Administration's proposed 2026 tax cuts will be less potent than in previous decades due to the adverse effects of excessive debt. Near the Pandemic high, gross government debt equaled 123.6% of GDP in 2024 (Chart 4), 4.7% above the peak of World War II, and 92% more than in 1981 (the year of Reagan tax cuts).

Debt Overhang

Diminishing returns

Economic output declines when a factor of production (land, labor, capital technology) is overused. Confirming this situation, the U.S. has experienced a decline in the dollar amount of GDP produced by a new dollar of government debt. In 2024, a new dollar had only 80 cents of GDP, down about $3.15 in 1981, thus dramatically illustrating diminishing returns.

Further evidence of the pernicious impact of government debt was illuminated when RRR found that when gross government debt exceeds 90% of GDP, an economy loses 1/3 of the trend rate of growth (Journal of Economic Perspectives, 2012). In 2024, the debt ratio was 35% higher than RRR's deleterious impact point (the red horizontal line in Chart 4). As they foretold, real per capita GDP (RPGDP) grew at a paltry 1.3% in the last 20 years, down slightly more than 40% below the long-term trend rate of growth of 2.3%. Numerous other academic studies have also confirmed the adverse effect of government debt on RPGDP.

Interest expense

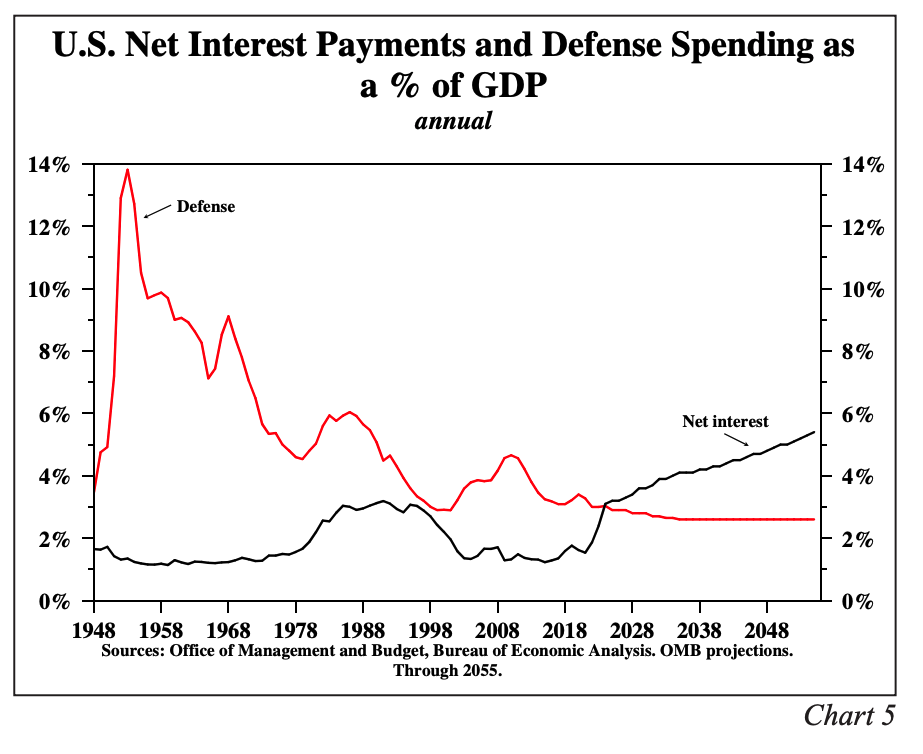

Interest expense, a deadweight loss that increases rapidly as the level of government debt rises, will worsen indefinitely for the U.S. without material policy changes (Chart 5). Debt servicing doesn't pay salaries or build bridges; 30% of these payments go to foreign holders of U.S. debt. Also, Niall Ferguson, a noted economic historian at the Hoover Institute at Stanford University, has found that rising interest expenses over military expenditures have marked a significant downward turn in great countries going back to the earliest days of recorded history. (Debt Has Always Been the Ruin of Great Powers. Is the U.S. Next? Wall Street Journal, 2/21/2025.) The collapse of the Mesopotamian, Roman, Bourbon, and British empires, plus many smaller ones that history has largely forgotten, are famous consequences of too much debt and its by-product - interest expense.

Demographics

The U.S. population increased by 3.3 million or about 1% in 2024, the fastest pace since 2001. Immigration, dominated by illegal entry, accounted for 84% of this increase. Global Economics at Goldman Sachs estimates "net immigration by the end this year will total 500,000" compared with slightly over 2.5 million in 2024. Immigration's recent history of indirectly boosting employment and raising both government and private spending is coming to an abrupt end.

Long-Term Treasury Bonds

The current and future direction of government spending is contractionary. Due to the extreme government debt and interest costs, proposed tax cuts, which are in the main extensions not additions, will be slow working. Decreasing regulation, increasing domestic energy production, shifting back to lower-cost fossil fuels, suppressing crime and its cost, and making the government more efficient are all disinflationary measures that help boost the standard of living. However, restoring the U.S. to its historical trend rate of economic growth depends heavily on reversing the debt overhang.

The Fed has yet to cushion the economic restraint from current federal spending and adverse multipliers, the lagged effects of prior central bank actions, and the immediate demographic drag. Thus, the five convergent factors mentioned initially suggest that the risk of recession is high, and the transition to meaningful recovery will be fitful, uncertain, and labored. Such an uncertain environment of tepid or negative economic growth will be conducive to a downward trajectory of long-term Treasury rates.

Hoisington Investment Management

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

DISCLOSURES

Hoisington Investment Management Company (HIMCo) is a federally registered investment adviser located in Austin, Texas, and is not affiliated with any parent company.

The information in this market commentary is intended for financial professionals, institutional investors, and consultants only. Retail investors or the general public should speak with their financial representative.

Information herein has been obtained from sources believed to be reliable, but HIMCo does not warrant its completeness or accuracy; opinions and estimates constitute our judgment as of this date and are subject to change without notice. This memorandum expresses the views of the authors as of the date indicated and such views are subject to change without notice. HIMCo has no duty or obligation to update the information contained herein.

This material is intended as market commentary only and should not be used for any other purposes, including making investment decisions. Certain information contained herein concerning economic data is based on or derived from information provided by independent third-party sources. Charts and graphs provided herein are for illustrative purposes only.

This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of HIMCo.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All