Many retirees hold substantial assets in traditional IRAs and taxable brokerage accounts. When planning for retirement income and considering your legacy, Roth IRA conversions can be a strategic way to reduce your tax burden and maximize the wealth you pass on to your heirs. Understanding the differences between traditional vs. Roth IRAs, the tax implications of a Roth conversion, and how to effectively cover the associated tax bill is essential in making this decision. The tax liability can be substantial, but so can the potential wealth savings (and transfer to your heirs), making thoughtful planning crucial.

In this article, we’ll explore why a Roth IRA conversion might make sense for you, how it works, and provide a few examples of the potential savings.

TLDR; When a Roth IRA Conversion Makes Sense

A Roth IRA conversion makes the most sense when you strategically plan for tax efficiency and long-term wealth growth. Here’s when you should consider it:

-

When you expect your tax rates to be higher in the future: If you anticipate being in a higher tax bracket later, converting now locks in today’s rates and avoids higher taxes in the future.

-

When you have large retirement accounts you want to leave to heirs: If you want to pass down tax-free assets to heirs (especially those in higher tax brackets), a Roth IRA conversion ensures your heirs won’t have to pay income taxes on Inherited IRA withdrawals.

-

Have Non-Retirement Funds Available for Taxes: You need to ensure you have non-retirement funds available to pay the tax bill so that the full conversion amount stays invested.

-

Won’t need the converted Roth funds for at least five years: In order to avoid the 10% conversion penalty you must wait five years before making a withdrawal from a converted Roth IRA.

-

Reducing Future RMDs: To minimize required minimum distributions (RMDs) that could push them into a higher tax bracket later.

Understanding Tax Implications Before Doing a Roth IRA Conversion

The primary reason we will recommend a client consider a Roth IRA conversion (typically in retirement or just before retirement) is to minimize the overall tax burden. Traditional IRAs require Required Minimum Distributions (RMDs) starting at age 72/73 (depending on when you were born), which are taxed as ordinary income and can push you into higher tax brackets. By converting to a Roth IRA, you pay taxes on the converted amount now, potentially at a lower rate, and avoid RMDs later, allowing your investments to grow tax-free.

However, it’s crucial to have sufficient funds in other accounts to cover the tax liability incurred by the conversion. Paying the tax from the converted funds diminishes the benefits of the conversion. Additionally, ensure you have adequate cash flow to support your retirement needs without relying on the converted funds.

For official IRS guidelines and tax rules on Roth IRA conversions, visit the IRS website.

Case Studies

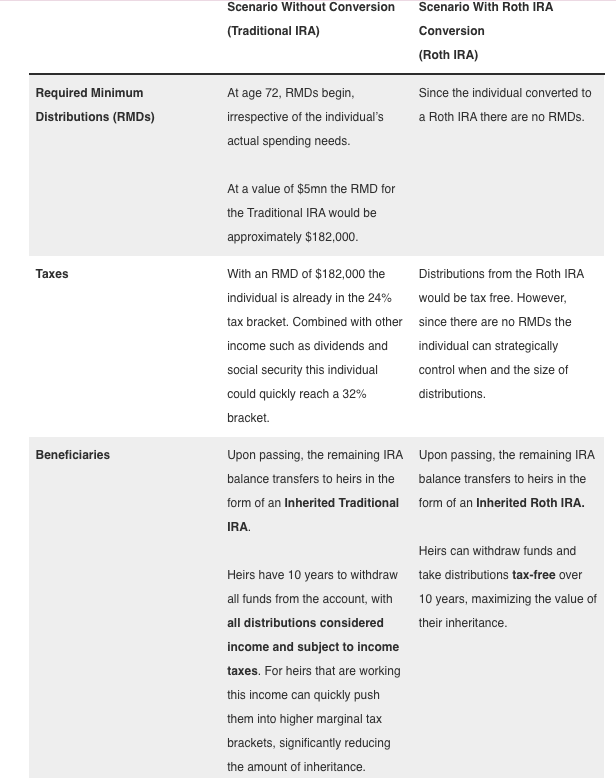

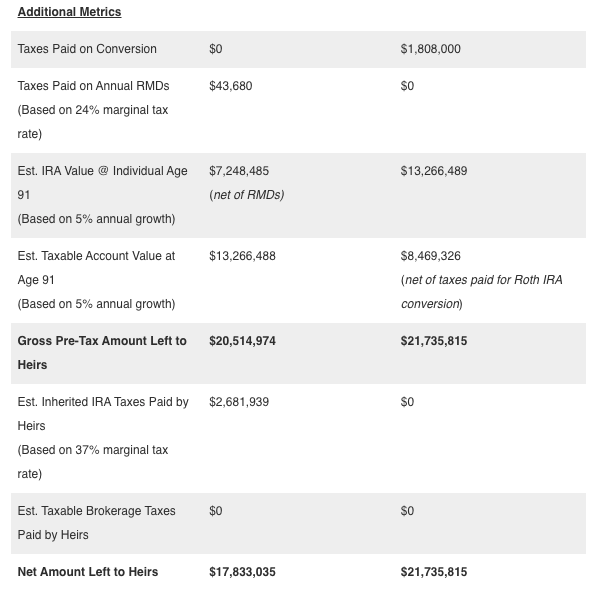

Case Study 1: Wealthy 70 Year Old Single Individual

Background: 70-year-old with $5 million in a traditional IRA and $5 million in a taxable brokerage account; two grown children.

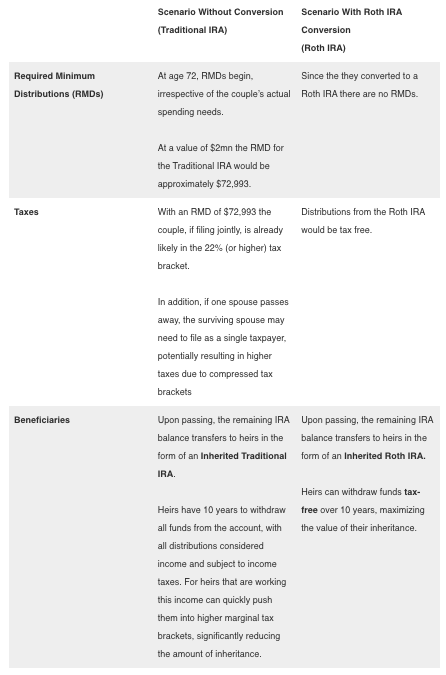

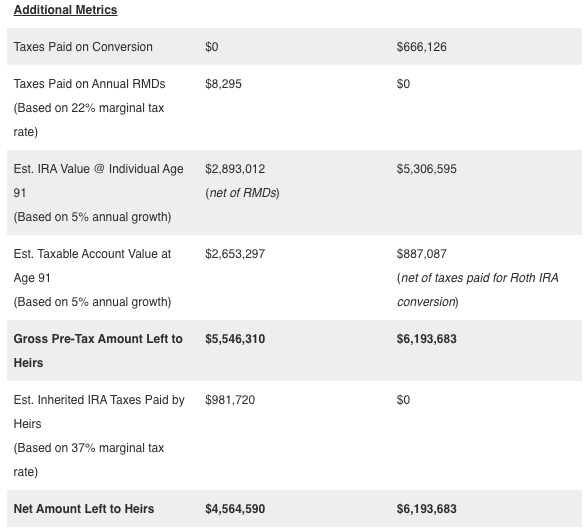

Case Study 2: High Net Worth Married Couple

Background: Couple with $2 million in a traditional IRA and $1 million in a taxable brokerage account; one grown child.

In both examples, the decision to convert depends on factors such as current and future tax rates, the ability to pay conversion taxes from non-retirement assets, and the desire to maximize the after-tax value of the inheritance.

Consulting with a financial advisor is essential to tailor a strategy that aligns with your financial goals and estate planning with Roth IRAs. Learn more about our investment management strategies.

We’re Here to Help

By carefully considering a Roth IRA conversion, you can enhance your retirement tax strategy and provide significant benefits to your heirs. To discuss your specific financial situation, schedule a consultation with Defiant Capital Group.

Frequently Asked Questions (FAQ)

What is a Roth IRA conversion?

A Roth IRA conversion is the process of moving funds from a traditional IRA to a Roth IRA. This requires paying taxes on the converted amount upfront, but once in a Roth IRA, the funds grow tax-free and can be withdrawn tax-free in retirement.

Can I undo a Roth IRA conversion and change it back to a Traditional IRA?

No, Roth IRA conversions are permanent. Previously, investors could “recharacterize” (undo) a Roth conversion, but the IRS eliminated this option in 2018. Once you convert, you must pay the taxes due and cannot reverse the decision.

Is there a certain age I need to do this by?

There is no official age limit for Roth IRA conversions, but after age 73, Required Minimum Distributions (RMDs) must begin for traditional IRAs. You cannot convert RMDs to a Roth IRA, so if you plan to convert, it’s often beneficial to do so before RMDs begin.

What happens to assets in my Roth IRA when I die?

If you pass away with assets in a Roth IRA, your beneficiaries will inherit the account tax-free. However, non-spouse heirs must withdraw the full balance within 10 years under current IRS rules. The good news is that these withdrawals remain tax-free.1. When is the best time to do a Roth IRA conversion in retirement?

The best time for a Roth IRA conversion depends on your tax situation. Generally, converting during lower-income years, before Required Minimum Distributions (RMDs) start, or when market values are down can be advantageous.

What are the tax implications of a Roth IRA conversion?

Converting to a Roth IRA requires paying taxes on the converted amount upfront. However, once in the Roth IRA, the funds grow tax-free, and withdrawals in retirement (including by heirs) are also tax-free.

Can I convert only a portion of my traditional IRA?

Yes, you can perform partial Roth IRA conversions over several years to spread out the tax liability and avoid pushing yourself into a higher tax bracket.

How does a Roth IRA benefit my heirs?

Since Roth IRAs do not have RMDs for the account owner, they can grow tax-free for heirs. Beneficiaries must withdraw the funds within 10 years, but these distributions are tax-free, reducing their overall tax burden.

Should I pay the conversion tax with my IRA funds or other assets?

It’s generally best to pay the conversion tax using non-retirement assets to maximize the funds remaining in your Roth IRA for tax-free growth.

Please read important disclosures here.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group