Matthews Emerging Markets Small Companies Fund

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhat is the objective of the Matthews Emerging Markets Small Companies Fund?

The Matthews Emerging Markets Small Companies Fund seeks long-term capital appreciation by investing in small companies that have a market capitalization of less than US$5 billion at purchase, or the largest company included in the Fund’s primary benchmark, the MSCI Emerging Markets Small Cap Index, and that are located in emerging markets (EM). A company or other issuer is considered to be “located” in a country or a region if it has substantial ties to that country or region, such as deriving at least 50% of its revenues or profits from goods produced or sold, investments made, or services performed, or has at least 50% of its assets located, within that country or region.

How do you define small companies?

Typically, the Fund will invest in companies that have a market capitalization between US$100 million to US$5 billion at the time of purchase (or the largest company in the benchmark). However, the Fund can continue to hold current companies in the portfolio that have grown in market capitalization over US$5 billion.

What countries will the Matthews Emerging Markets Small Companies Fund be able to invest in?

Emerging market countries generally include every country in the world except the U.S., Australia, Canada, Hong Kong, Israel, Japan, New Zealand, Singapore and most of the countries in Western Europe. Certain emerging market countries may also be classified as “frontier” market countries, which are a subset of emerging market countries with newer or even less developed economies and markets, such as Sri Lanka, Bangladesh and Vietnam.

Will the Fund invest in frontier markets?

Yes, the Fund will be able to invest in frontier markets. Given the portfolio’s broad investment universe, it will be able to invest in a large number of emerging and frontier markets.

Why should investors consider a dedicated allocation to emerging markets small cap equities?

We believe small companies offer attractive growth potential, as well as the opportunity to gain highly differentiated portfolio exposures. For many global investors, a dedicated allocation to emerging markets small companies are unlikely to overlap with existing investments. The MSCI EM Small Cap Index provides for differentiated country allocations versus the MSCI EM Index. For example, China is 40% of the MSCI EM Index but only 11% of the MSCI EM Small Cap Index. An allocation to emerging markets small cap equities can therefore diversify country/currency exposure and in our view help improve the risk/reward profile of an overall portfolio, while providing access to nimble, entrepreneurial businesses in fast-growing economies. Another potential benefit is that stocks of smaller companies may be inefficiently priced, creating a marketplace where active management can add value. And finally, smaller companies tend to offer access to businesses whose earnings and market share are growing faster than that of larger companies.

I already own an emerging markets fund—why should I consider adding an emerging markets small companies fund?

Emerging market equity funds that take a “core” all-cap investment approach typically have a low weighting to small and mid-sized companies. Consequently the exposure to fast-growing, typically under-researched and under-valued smaller companies is low and investors may be missing out on companies that may offer attractive potential for generating alpha and given their growth momentum, could be an advantage that compounds over time.

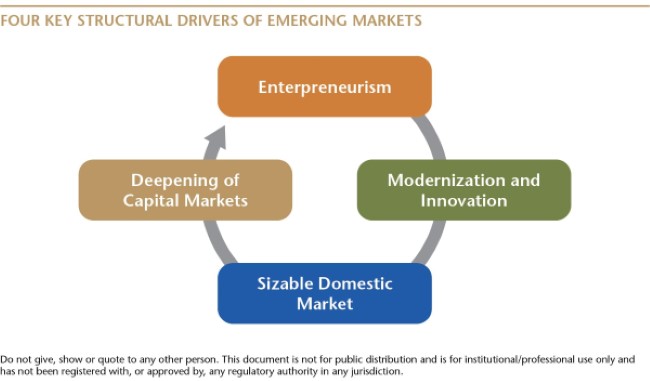

What are the structural drivers of the emerging markets for small companies?

The emerging markets small company investment universe has changed significantly over the past two decades. Today, we see the market as being driven by four key drivers:

- Modernization and Innovation: The emerging markets universe has undergone significant transformation over the last two decades and today emerging market companies are among the most innovative in the world. In aggregate, the biggest five emerging market countries spend on research and development is over 80% of the aggregate spend of the world’s largest developed markets. That spend has led to the strong development of intellectual property (IP) heavy industries like technology and health care. Looking ahead, we believe innovation will continue to be one of the major economic growth drivers and value creators in emerging markets. We believe the next 30 years of growth will be driven by growth in productivity via technology growth and improvement in efficiency as income surpasses major inflection point—US$10,000 per capita

- Sizable Domestic Markets: Emerging markets are home to some of the most populous and also some of the fastest growing countries in the world and therefore also home to some of the biggest, fastest growing and resilient middle classes. We believe small companies provide direct access to higher-growth domestic consumption sectors that typically cater to this fast growing and resilient middle class. By virtue of being local to these markets they are better able to understand local tastes, evolving trends and more nimbly launch and upgrade products and services that appeal to local markets.

- Deepening of Capital Markets: Emerging markets are increasingly home to large pools of savings and capital that are able to fund innovative and fast growing companies. Therefore emerging markets in general—and Asia in particular—have had a thriving IPO market in recent years. Importantly, the universe has also deepened, with small companies now operating across all key sectors within the emerging markets.

- Entrepreneurism: Aided by strong national research and development spend, sizeable and growing domestic consumer base and deepening capital access, entrepreneurism is thriving in emerging markets. Small companies, particularly in Asia, have been central to their economies. In fact, many small companies in Asia have contributed to economies being able to transition from the low value-added model to a higher-value added economy. They have had success in wide ranging areas such as biotechnology, software, internet, manufacturing and automation in the recent years. On the consumer products and services side, given their better understanding of consumer needs, tastes and preferences, small companies have become brands in their own right, which leads to more sustainable returns on equity and returns to shareholders, making small companies an attractive investment proposition.

What differentiates the Matthews Emerging Markets Small Companies Fund from its peer group?

Our deep Asia expertise—For 30 years, Matthews Asia has invested in the markets that represent approximately 75% of the MSCI Emerging Market Small Cap Index. In particular, we have a deep understanding and long track record of investing in small-cap companies and we believe we have a proven investment process, which seeks to identify good quality companies and management teams with strong ESG profiles and reasonable valuations. We believe this provides a good opportunity to apply our knowledge and experience of researching and investing in these types of companies to markets outside of Asia. We believe that the ascendance of Asia, and the long-term potential of China in particular, makes it increasingly important for emerging market investors to have an investment manager with deep experience of the Asia region.

Domestic consumption focus—Our investment approach has typically focused on finding attractive companies that are benefiting from consumption-led growth. Rising wealth and consumption in emerging markets have resulted in a growth in consumer-orientated businesses—particularly led by Asia—creating opportunities in many sectors such as IT, communications and health care. Consequently, to some degree, the economies within the emerging markets outside of Asia have become less cyclical and more consumer-driven.

ESG—The unavailability of ESG data among emerging markets companies in general and among small cap companies in particular is well known. Another well-known issue is that of lack of consistent application of ESG analysis principles leading to very divergent ESG ratings from various data providers on a given company. We rely on our own ESG process and on our very extensive on-the-ground research capabilities to gather ESG data and conduct ESG due-diligence. We believe this ability differentiates us from our peer group.

High active share—Importantly, we build portfolios that look very different from our benchmark and generate high active share, offering investors true diversification and attractive long-term growth potential.

Who is managing the Matthews Emerging Markets Small Companies Fund?

Vivek Tanneeru is the Lead Manager and Robert Harvey, CFA, and Jeremy Sutch, CFA, are Co-managers of the Matthews Emerging Markets Small Companies Fund. As Lead Manager, Vivek is fully responsible for investment decisions, including initiating, adding to or reducing current holdings. However, investment ideas and holdings are deliberated and developed in a highly collaborative manner.

The Matthews Emerging Markets Small Companies team also collaborates closely with the Matthews Emerging Markets Equity team and meets regularly, but informally discusses and shares research ideas. The team also collaborates with the Matthews China Small Companies team and regularly meets to stimulate cross-team idea generation and expand our body of research related to China, an important market in emerging markets.

The team also leverages the full resources of the broader 40-person Matthews Asia investment team and their expertise of investing across the Asia region.

What experience does Matthews Asia and the portfolio management team have investing in small-caps and emerging markets?

Small and mid-cap companies have always been core allocations within all our portfolios since the inception of the firm and we have managed a dedicated Asia Small Companies strategy since 2008 and dedicated China Small Companies strategy since 2011.

Our deep understanding of the diversity of the economies in Asia is an expertise that we can bring to broader emerging markets which have similar economic characteristics. For example, in Asia we find economies that range from small frontier to large developed, to those running account surpluses to those in deficit or where populations are growing or getting smaller. These same dynamics exist across the spectrum of emerging markets. We believe we have the resources, expertise and long-term focus to manage the increasingly complex characteristics of an Asia-focused emerging market universe.

We believe our proven investment process, which seeks to identify good quality companies and management teams and reasonable valuations, is one that can be applied equally as well to markets outside of Asia. In general, quality businesses tend to exhibit similar characteristics across geographies, including being cash-generative, having strong growth prospects, low levels of leverage and strong business moats that support margin growth and profitability. The ability to work in different markets and cultures is a factor in Asia as much as it in other emerging markets.

The Matthews Emerging Markets Small Companies Fund portfolio team has significant experience investing in emerging markets and in small to mid-cap companies. Lead Manager Vivek Tanneeru has spent his entire 16-year career focused on Asia and the emerging markets, including as an Investment Manager on the Global Emerging Markets team of Pictet Asset Management in London. Vivek has always managed portfolios that had significant allocation to small and mid-cap companies. Robert Harvey has over 27 years industry experience and has spent his entire career focused on Asia and the emerging markets. Jeremy Sutch has 27 years industry experience and has spent most of his career focused on small- to mid-cap companies.

- Vivek Tanneeru—Prior to joining Matthews Asia in 2011, Vivek was an Investment Manager on the Global Emerging Markets team of Pictet Asset Management in London. While at Pictet, he also worked on the firm’s Global Equities team, managing Japan and Asia ex-Japan markets. Vivek is also the Lead Manager on the Matthews Asia ESG strategy. He has an MBA from the London Business School and he is fluent in Hindi and Telugu.

- Robert Harvey, CFA,—Prior to joining Matthews Asia in 2012, he was a Senior Portfolio Manager at PXP Vietnam Asset Management from 2009 to 2012, where he focused on Vietnamese equities. Previously, he was a Portfolio Manager on the Global Emerging Markets team at F&C Asset Management in London from 2003 to 2009. Robert started his investment career in 1994 as an Assistant Equity Portfolio Manager with the Standard Bank of South Africa’s asset management division. He received a Bachelor of Commerce in Accountancy and Commercial Law from Rhodes University in South Africa and a Bachelor of Accounting Science in Advanced Management Accounting, Taxation and Auditing at the University of South Africa.

- Jeremy Sutch, CFA,–Prior to joining the firm in 2015, he was Director and Global Head of Emerging Companies at Standard Chartered Bank in Hong Kong from 2012 to 2015, responsible for the fundamental analysis of companies in Asia, with a particular focus on small- and mid-capitalization companies. From 2009 to 2012, he was Managing Director at MJP Capital in Hong Kong, which he co-founded. His prior experience has included managing small-cap equities at Indus Capital Advisors and serving as Head of Hong Kong Research for ABN AMRO Asia Securities. Jeremy earned an M.A. in French and History from the University of Edinburgh.

While our small companies strategies have had their own portfolio managers, analysts across the firm who work on all-cap regional or single-country strategies have always dedicated meaningful time to uncovering, assessing, and monitoring small-cap holdings. Our regional strategies in particular have significant allocations to small and mid-sized companies and our research efforts and idea generation extends across the investment team as opposed to being centralized within the two small-cap strategies.

What is the expected exposure to Asia in the Matthews Emerging Markets Small Companies Fund?

Asia is by far the largest single regional allocation of the Fund and a reflection of where the team believes the majority of the best-quality growth companies can be found. Currently the Fund has an overweight in Asia (including through companies domiciled elsewhere that have substantial ties back to Asia) compared to the benchmark but that can change based on the opportunity set composition as well as valuations through time.

What is the investment philosophy that underpins the Matthews Emerging Markets Small Companies Fund?

We believe small companies in emerging markets provide direct access to the region’s higher-growth domestic consumption sectors that cater to a fast growing and resilient middle class. Small companies provide an opportunity to invest in emerging markets’ and Asia’s innovation edge and partner with minority shareholder-friendly entrepreneurs at early stages. This can be achieved by tapping innovative companies with an ability to compound growth over the long term at an early stage by researching and investing in high quality companies (including at IPO and also pre-IPO stages, where possible) with particular focus on IP-driven sectors such as technology and health care.

The Matthews Emerging Markets Small Companies Fund is designed to round out exposure for investors who aim to be diversified across the emerging market equity landscape. Its core philosophy is that small companies in the emerging markets are well-positioned to take advantage of important trends in domestic demand and are nimble enough to react quickly to the region’s changing consumption patterns. Through our in-house research process to identify inefficiently priced opportunities, P/E expansion potential, and rigorous on-the-ground research and due diligence, the actively managed Fund aims to identify well-managed companies in the early stages of growth with the ability to compound in size over a multiyear time horizon.

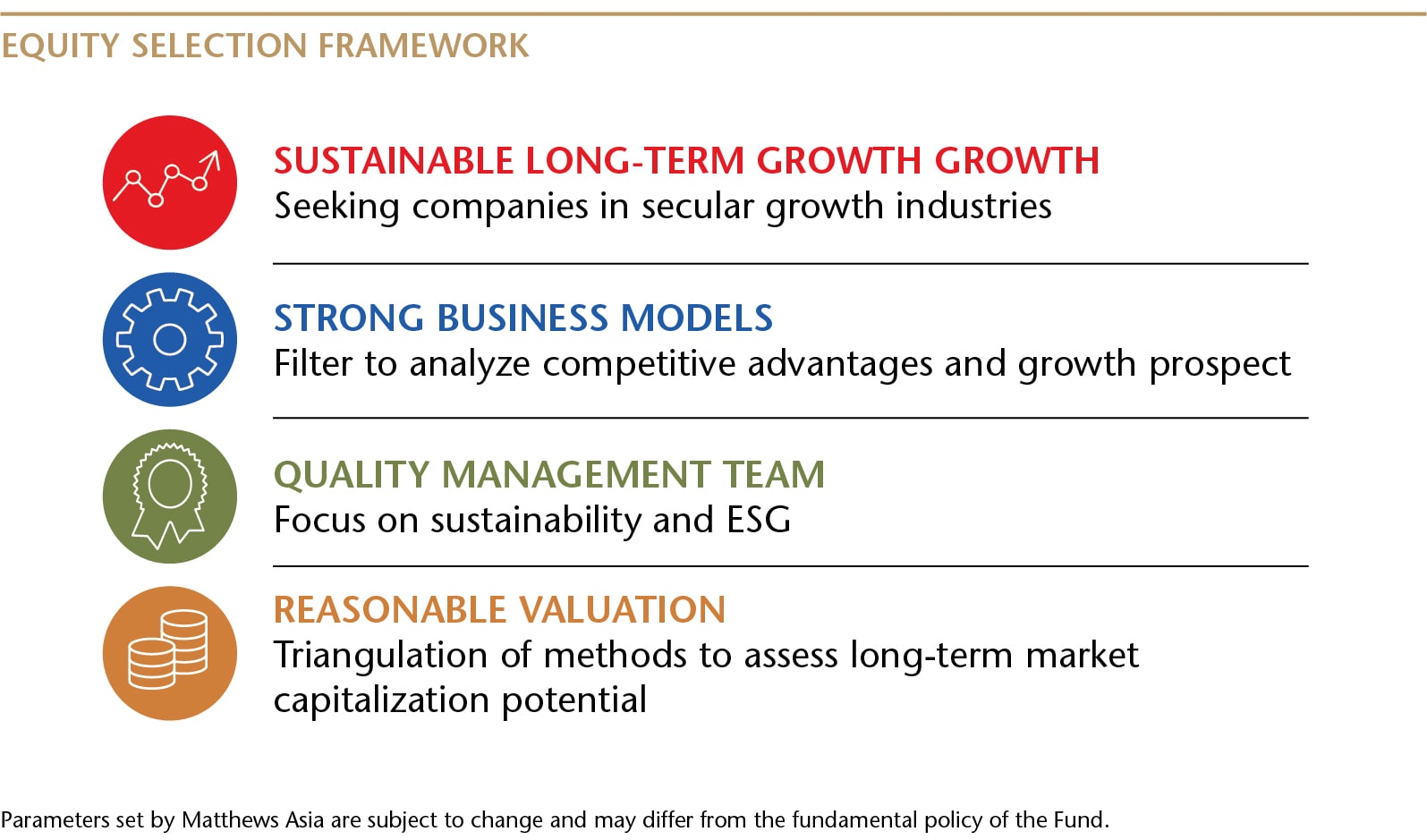

What is your investment approach?

The Matthews Emerging Small Companies Fund team believes the key to successful small-cap investing is to identify companies with a favorable combination of sustainable long-term growth prospects, strong business models, quality management teams and reasonable valuations. To accomplish this, the team relies on a bottom-up, fundamental investment process. Because emerging markets small-cap stocks tend to be under-researched by analysts, the team believes they are often priced at a discount to their large-cap peers.

How do you generate ideas?

The investment universe for the Fund is comprised of companies located in the emerging markets. Prior to applying any specific market-cap screen, there are 30,700+ listed securities in the investment universe. The universe is narrowed to approximately 11,200 companies by applying a minimum US$100 million market cap and a maximum US$5 billion market cap, or a maximum of the market cap of the largest company included in the Fund’s benchmark (the MSCI Emerging Markets Small Cap Index).

The resulting group represents the broadest notion of the “investable universe” for the Fund.

From here, the team uses a series of screens to help isolate sustainable, operational improvements in companies that are distinct from cyclical changes. These include screens driven by important fundamental factors, such as growth rates, cash flow generation, return on equity and return on invested capital. Next, members of the Emerging Markets Small Companies Fund team and other members of the broader investment team meet to determine whether a company merits further due diligence. At this point, the actionable investment universe is narrowed to several hundred companies for potential inclusion in the portfolio.

On the ground research and due-diligence is an important component of research process and also an important source of ideas, as are cross pollination of ideas within the broader investment team as well as IPO opportunities.

What types of companies do you look for?

Within the actionable investment universe, the Matthews Emerging Markets Small Companies portfolio team works to identify companies with high-quality business models and management teams, as well as inefficiently priced opportunities and the potential for P/E multiple expansion. The following factors are considered as part of this analysis:

|

Sustainability of return profile and growth prospects • Identification of competitive advantage, market structure and long‐term growth prospects • Preference for domestically oriented revenue stream |

Quality management teams • Understanding of their background and motivations • Consistency between commitments and actions |

|

Appropriate capital allocation and sound capital structure • Sensible deployment of cash flow and CapEx spending • Generally avoid companies with highly levered balance sheets • Preference for low financial leverage when a firm has significant operating leverage |

Strong ESG standards • Understanding of incentive structures for senior management • Interest alignment with minority shareholders • Transparency and discipline |

How important is meeting with company management?

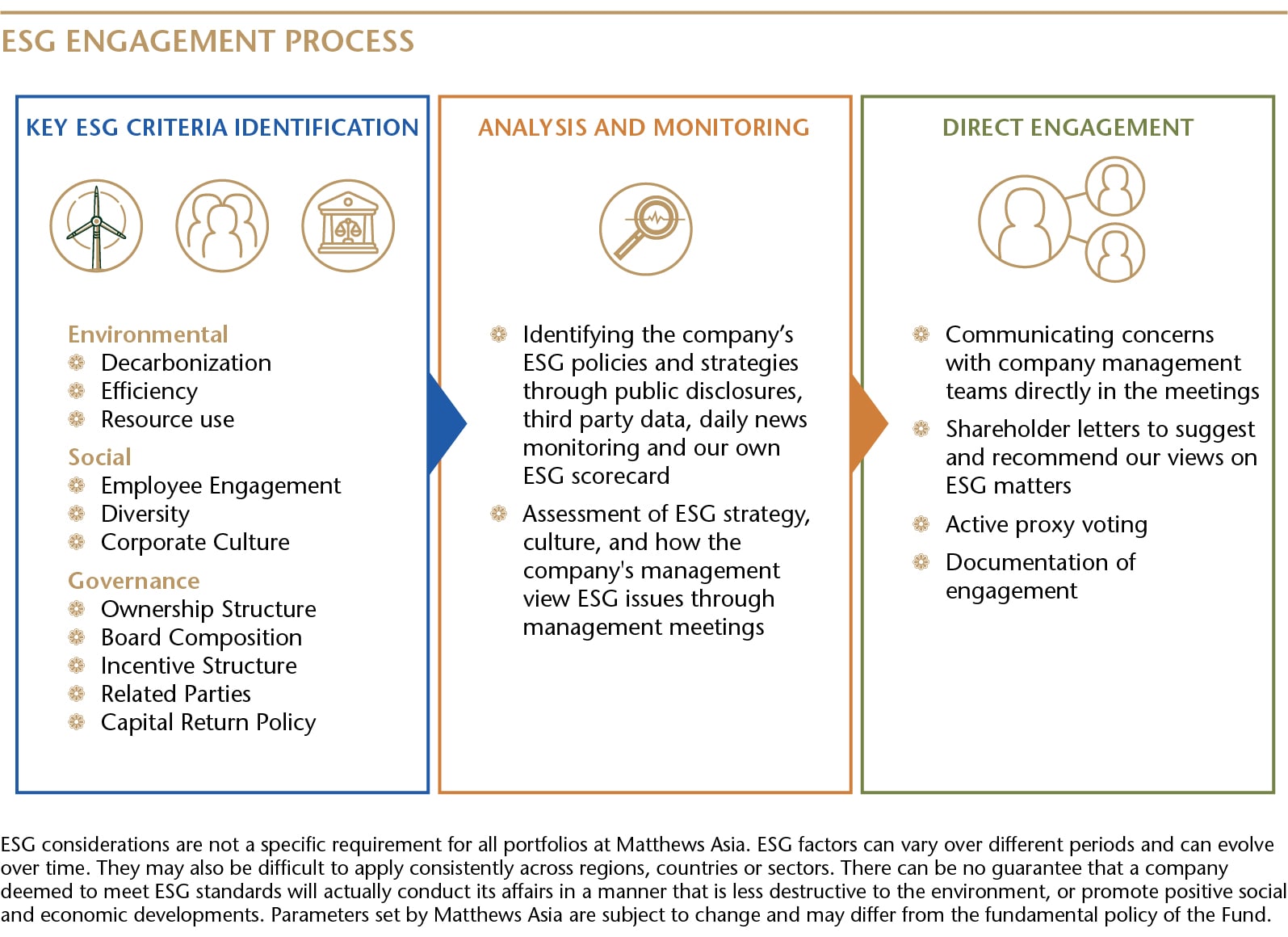

The team prioritizes meeting with company management before investing in order to make qualitative and quantitative assessments of a company’s operations and integrity. Across the broader investment team, Matthews Asia conducted more than 3,600 company meetings in 2020.

When assessing company management, the team evaluates whether companies have both the aspiration as well as the financial ability to implement their growth strategies. The team favors management teams that demonstrate discipline in capital allocation and, hence, deliver the potential to compound the size of the business over time without excessive reliance on external capital. The team tends to avoid complicated corporate ownership structures where there is a risk of conflicts of interest and related party transactions.

Given the long-term holding periods, company visits and meetings are an essential part of the investment process. They give us better insight into a company’s business model and growth prospects as well as management’s thoughts on business strategy and capital allocation. The meetings also provide a good opportunity for us to gain a greater understanding of the management team and their intentions for the company. These on-the-ground meetings are important as companies in emerging and frontier markets are substantially smaller, less liquid and more volatile than securities markets in more developed markets.

A lot of emphasis is also placed on developing a 360-degree view on a company by also meeting company’s competitors (both listed and unlisted), suppliers, customers, distributors and regulators. Often research also involves visiting companies, R&D facilities, factories, distribution centers etc.

A first meeting with a new company will provide an opportunity to (1) understand the firm’s management strategy, track record and long-term business prospects, and (2) do a preliminary assessment of the company’s ESG practices. It is vital the team develops a positive view of ESG practices before investing in a company. We believe that by investing in quality companies we have the potential to yield strong returns with a lower risk of permanent loss of capital. Once the company is in the portfolio, we continue to maintain regular meetings with the team to ensure that we continue to have confidence in both the business and its management team.

The current COVID-19 pandemic has limited the amount of travel that our analysts and portfolio managers can do to see companies. However, we do have colleagues in China, Hong Kong, and Singapore, who are able to relay to us how people are dealing with the pandemic there and across the region. Having gone into the crisis and lockdowns earlier than the U.S., these geographies are also emerging earlier. We are still able to do a large volume of company meetings—by audio and video conference calls. The investment team has had easy access to executives of portfolio holdings and non-portfolio holdings. Such access enables us to both monitor companies that are in our portfolios and search for new opportunities. The investment team is conducting 15-20 meetings a day on average across the team, starting early in the morning and continuing late into the night, to catch the working day in Asia and Central, Eastern Europe and Middle East/North Africa. These meetings provide information, the salient points of which we can share at a daily investment team meeting and in innumerable emails and phone calls between team members. Traders, too, have been able to execute trades with minimal disruption to normal working life.

How do you construct your portfolio?

The Matthews Emerging Markets Small Companies Fund seeks to identify companies in emerging markets that are in the early stages of growth that have the ability to compound growth over the long-term, with market capitalization no higher than the greater of US$5 billion or the market capitalization of the largest company in the Funds’ benchmark. We apply an unconstrained and benchmark agnostic approach in terms of country, sector and company allocations, and exposures are a by-product of bottom-up security selection.

New positions will be modestly sized but expected to be at least 0.75% of the portfolio. Typical position size will be between 1% to 5% and is guided by several factors, such as liquidity, track record, management quality, corporate governance standards, ESG risk exposure and mitigation, valuation and conviction in corporate fundamentals. The holdings in the Fund will generally have a long-term investment horizon and the portfolio will hold 40 – 80 names.

When do you decide to sell a company?

Although the team seeks to develop the conviction to invest in companies over a multiyear horizon, several factors may result in selling a company, including a broken investment thesis or material ESG issues. Additionally, the Fund’s portfolio managers typically sell out of a position when a company moves well above that of the largest market cap company for a period of time; this discipline ensures the Fund adheres to its small cap focus.

The team constantly monitors valuations in the context of growth expectations and typically will trim positions where valuations have risen significantly, rather than sell a holding outright. Generally, the Fund’s long-term investment horizon is expected to result in low portfolio turnover.

How does the Fund approach risk management?

Risk management is integral to the team’s efforts to ensure and improve the Fund’s performance and is embedded into the team’s investment process. The team manages the risks of investing in small companies through its knowledge of the markets and the intensive research conducted on the companies in which it invests. The team investigates management backgrounds and incentives, validates products carefully, and avoids related party transactions and serial acquirers that destroy value. In addition, the team carefully considers the size of each position and monitors overall sector and country exposure in the portfolio to ensure diversification and manage liquidity. Sharp currency devaluation can lead to capital loss for a U.S. Dollar investor, so we also monitor currency outlook of the countries we are invested in closely.

Matthews Asia has developed a rigorous and tested approach to risk management with three levels:

- Portfolio Level—through the in-depth company due diligence process performed by our Investment professionals and their continuing focus on avoiding permanent impairment of capital

- Matthews Asia CIO Level—through oversight and review of the portfolio to help ensure consistency with the investment goals and objectives and a review of portfolio risk and liquidity

- Matthews Asia Enterprise Level—through independent risk and compliance monitoring performed by our Control Side functions (Legal, Investment Risk, Compliance, Operations/IT, Fund Admin and Finance) and our Governance process which was designed to ensure that all significant risks are escalated to and discussed with senior management

How is ESG integrated into the investment process?

Our primary focus for this Fund is to analyze material environmental, social and governance risks a portfolio company faces and try to mitigate those risks by a combination of position sizing, active engagement and proxy voting process. We also, to a certain extent, invest in the opportunities created by changing regulatory landscape and consumer preferences when it comes to ESG. We will use third-party data, where available, as an input into our ESG analysis but use our own in-house process to incorporate ESG.

You should carefully consider the investment objectives, risks, charges and expenses of the Matthews Asia Funds before making an investment decision. A prospectus or summary prospectus with this and other information about the Funds may be obtained by visiting matthewsasia.com. Please read the prospectus carefully before investing as it explains the risks associated with investing in international and emerging markets.

Investing in international and emerging markets, including frontier markets, may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Investing in small- and mid-size companies is more risky than investing in larger companies as they may be more volatile and less liquid than large companies. In addition, single-country and sector funds may be subject to a higher degree of market risk than diversified funds because of concentration in a specific industry, sector or geographic location. Additionally investing in emerging and frontier securities involves different and greater risks, as these countries are substantially smaller, less liquid and more volatile than securities markets in more developed countries. Pandemics and other public health emergencies can result in market volatility and have an adverse impact on the value of an investment in the fund. Less developed countries and their health systems may be more vulnerable to these impacts all of which could be significant and result in losses.

The views and information discussed in this report are as of the date of publication, are subject to change and may not reflect current views. The views expressed are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific investment vehicles.

The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information. Matthews International Capital Management, LLC is the advisor to the Matthews Asia Funds.

Matthews Asia is the brand for Matthews International Capital Management and its direct and indirect subsidiaries.

The MSCI Emerging Markets Index captures large and mid cap representation across 26 Emerging Markets (EM) countries. With 1,404 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Emerging Markets Small Cap Index is a free float adjusted market capitalization weighted index designed to measure the performance of small cap stocks in 27 emerging market countries.

The views and information discussed in this report are as of the date of publication, are subject to change and may not reflect current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. Investment involves risk. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Investing in small- and mid-size companies is more risky and volatile than investing in large companies as they may be more volatile and less liquid than larger companies. Past performance is no guarantee of future results. The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits