As a new year approaches, we naturally start thinking of the future and asking ourselves: “How might things be different?” I often think that a little strange—what makes January so different from December? To anticipate change, we have to look out a little further than a few months. More of the same is always a good first estimate. But who can bear to even think that way this year? Not me, for sure. And to be honest, this year there is more reason to think that even in the short term there could be some pretty significant changes in Asia and emerging capital markets.

Let’s start with the U.S. presidential election. We have had a chance to see some of President-Elect Biden’s early appointments and his mindset is clear—he will draw from academia and on people with experience. This suggests that he wants to set a tone that is more similar to that of the Obama administration. People with these backgrounds are not likely to pursue confrontational policy with China. Rather, they may try to work with or persuade China. They will not easily distill down all of America’s perceived problems to “the trade deficit” but likely have a more nuanced approach to economic relations and bilateral trade. Indeed, the incoming Biden administration seems to show a desire to mend fences with Europe—one relationship that was a casualty of the past four years. Why is this important for Asia? Well, it strongly suggests that the policy toward China will change, that the new administration sees trade not as a war but as an exchange. The shift of U.S.–China frictions may move from dollars and cents to human rights issues and diplomacy. Europe is by no means anti-China; indeed parts of Europe have benefited from Chinese infrastructure spending. Europe’s own inability to harness its fiscal power to help weaker states gave China a diplomatic advantage in places like Italy and Greece. European countries are not as implacably opposed to a strong China.

More important than trade will be understanding China’s domestic demands because that is what drives its economy. Human rights may become more prevalent as a concern in international relations across the pacific. This has certainly been a theme of the U.S. democratic party in the past and was an area sometimes ignored in recent years. China can be very prickly on this issue. The Hong Kong Security Laws are probably not open for debate, after all. In addition, I suspect the treatment of the Uighur ethnic group in the Northwest of the country is not going to be open for discussion either. However, China will be more receptive to other issues of human rights—housing, health care, the environment. These issues are becoming increasingly important to its people, who have enough material possessions to care now about quality of life issues. China can surely be pressed on its global responsibilities in this sense because it sees them as being in its own self-interest. This means we can expect more regulation and legislation to limit environmental damage and to improve access to health care solutions for the majority of the population. Some of these will increase risks to business and may reduce profitability; others will be opportunities for businesses to facilitate social aims profitably. Furthermore, it may not be just China taking its cue from the West. For China has itself done more to try and lean against income inequality over the past decade. Perhaps the U.S. and Europe may pursue some of China’s minimum wage policies? Overall, these areas, whilst they pose diplomatic problems of their own, are less directly aimed at causing economic disruption. Moreover, a greater focus on spreading further the benefits of a wealthy society argues for further development of capital markets and corporate governance that will increase the opportunity set for us, too.

Social and environmental issues are also coming to the fore when investing in China, Asia and many of the emerging markets. This is not primarily because of demand from Western investors, as one might suspect. Rather, the demands are coming from the citizens of these countries themselves. Having grown from subsistence levels of development to the middle class, people value a clean environment, better health, a feeling of social justice. We are seeing this in regulations to develop health care systems, in policies to deal with income inequality, and even in government action to deal with monopoly power in new industries. Populations as well are seeking the same kind of financial freedom that we enjoy in the U.S. and Europe: this means developing trust in capital markets and pushing for better corporate governance. Some markets, such as some of the developed markets of Asia (Hong Kong, Singapore, Japan) have made great efforts in this regard. In Latin America, too. Markets like China have perhaps the furthest to go in this regard, but also the most to benefit as they seek a firm foundation for the development of insurance and pension systems as well as a way to maintain growth in the economy at higher levels of consumption and less investment.

Weaker Dollar Favors Developing Economies

Then there is the virus and potential vaccines that may be available very soon. And whilst there may be areas of life that have forever changed due to the lockdown—online shopping has become a natural reflex in our house—surely a return to greater normality is in the offing. That would mean reflation, a lowering of perceived risk, a return to more normal yields on long-term bonds. All of this would seem to point to a weaker U.S. dollar and, in the short term, at least favor emerging markets.

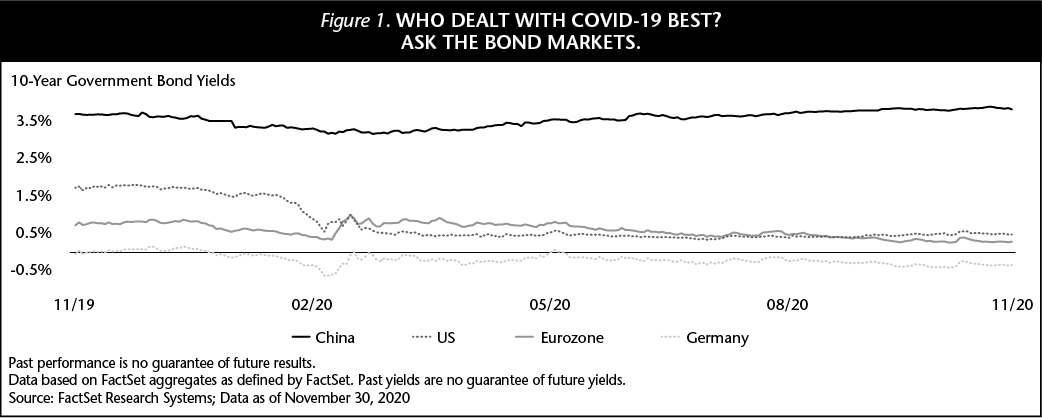

In any reflationary cycle, the more vulnerable and depressed emerging markets would likely bounce back first, leading me to think that it is the non-Asia countries that may do best in the immediate recovery. However, they have become such a small part of the universe that a more sustained recovery in emerging markets ultimately must mean strong performance across a broad swathe of countries, mostly in Asia. In this respect, China still seems well placed, mostly because it has the most realistic looking bond yields and its equity market valuations, though high, are at least based on normal discount rates. But the rest of the emerging markets have been hit harder by the virus—think of the economic relief that Brazil and India will experience as the pandemic recedes. And as world trade gets back to something like normality, too, the buildout of manufacturing bases across ASEAN and central Asia will continue and bring much needed succor to these economies, too.

I believe, therefore, that the recovery is likely to broaden the rally in the markets—from the online and virtual businesses to those most affected by lockdown to be sure. The rally may also broaden to performance beyond China and North Asia into the rest of the region, as well as into Latin America and Eastern Europe. I expect, too, that smaller companies, having suffered relative to large caps for much of the past decade, will fare better. All of these changes would suggest an improved performance by stocks that have perhaps until now enjoyed neither short-term momentum nor heady valuations. We may even see some so-called junk rallies, as the most depressed of businesses have their last hurrah.

V Is for Vaccine

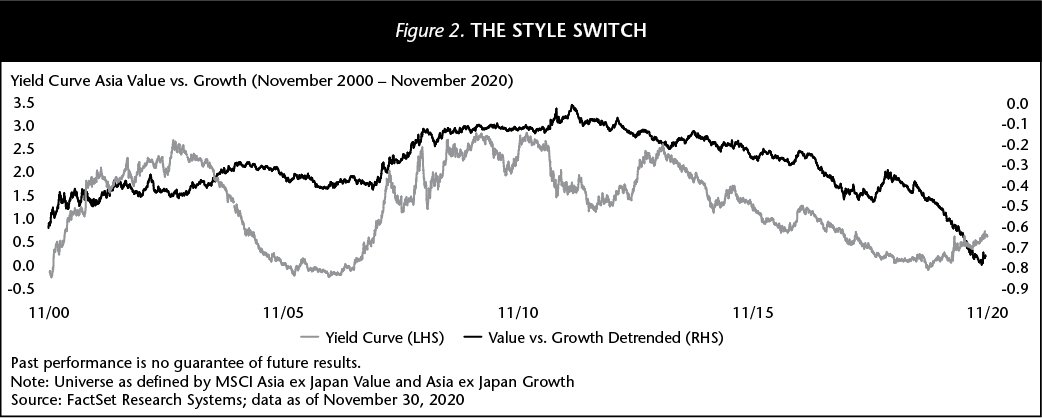

If we are moving to a more reflationary scenario, a stronger recovery, and a weaker dollar, I would be tempted to think the steepening of the yield curve could persist yet further. Historically, a sustained change in the yield curve has led to style rotations, with value stocks rallying. This may give rise to some “junk” rallies—highly indebted companies and highly cyclical businesses can sometimes rally strongly, but the life may soon go out of them again. “Time in the market” is more important than “timing the market” and that argues for a focus on sustainable growth. Nevertheless, a broadening of the recovery in the economy is often accompanied by a broadening of the market—a chance for small and mid-cap companies to reverse their underperformance of a decade and often argues for a greater focus on growth at a reasonable price.

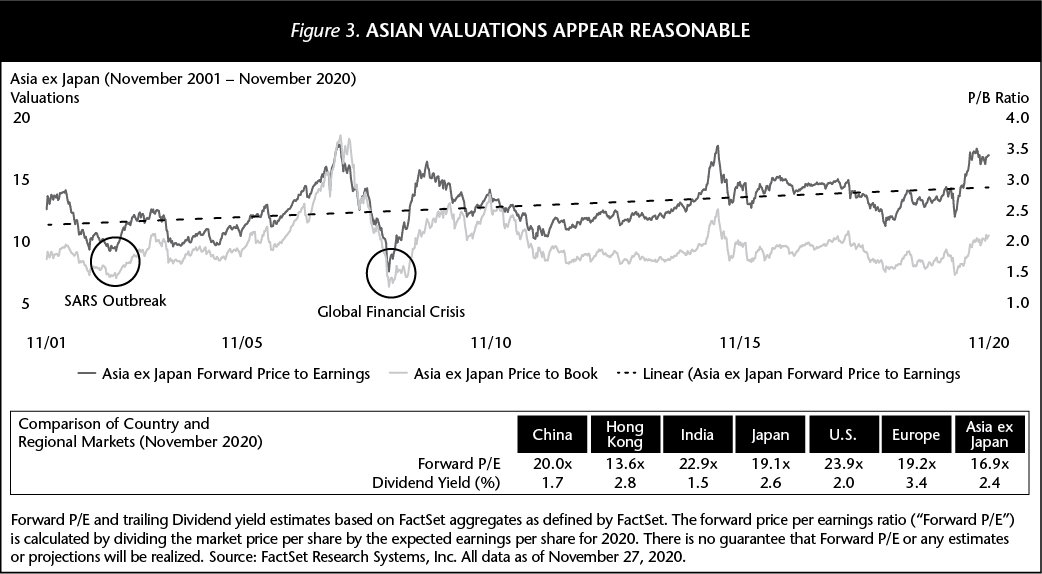

Vaccines are important, but vaccines cannot drive growth long term on their own. As we look past the pandemic, we believe it is valuable to reflect on what continues to make Asia the economic hub of emerging markets. Rising incomes, a universal desire for a better quality of life accompanied by predictable upgrades in consumer purchases, the continued opening of financial markets to foreign capital and a stronger social fabric due to a greater share of profits for workers all contribute to Asia’s long-term growth potential. Asia’s growth potential is measurable. As we look at total factor productivity across Asia, we see a consistent trend upwards. What’s more, equity valuations in Asia are less stretched than in the U.S., where market participants seem to expect a more robust and sustained recovery than we can find clear evidence for.

If low rates boost asset prices, from stocks to houses, a bigger question facing allocators is simply: where can investors still put money for long-term growth? As for overall valuations, whilst Asia is no longer cheaper than Europe and the discount relative to the U.S. may have narrowed somewhat, the reliability of the near-term recovery in earnings is greater. I would also argue that, at the beginning of 2020, we were expecting the reflationary environment in Asia to be more favorable to short-term earnings growth. After a year best forgotten, that still seems the case, so I anticipate faster earnings acceleration in Asia than in much of the rest of the world.

So, as we look to the new year, perhaps more reason to hope that tailwinds may favor emerging markets. As we consider changes in the political and economic environment, we do not see a need to make drastic changes in the portfolios we manage on behalf of clients. For there is still reason to think that businesses at the forefront of health care and the virtual economy will continue to do well. Rather, we must just be careful not to overlook some of the businesses that have struggled more recently and to be wary of valuations. In addition, in an environment of continued capital market development, we must continue to take advantage of the new investment opportunities that the markets are creating among newly listed businesses that are taking advantage of some of the long-term trends we see.

Important Information

The views and information discussed in this report are as of the date of publication, are subject to change and may not reflect current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. Investment involves risk. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Past performance is no guarantee of future results. The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information.