Sustainable economic growth comes from building institutions and developing economies that allow companies to generate greater gains from capital and labor. On the capital side of the equation, Asia's deepening financial markets and growing adoption of capital-light business models enable businesses to use assets more efficiently. On the labor side of the equation, Asia's workforce benefits from rising education levels and growing entrepreneurial spirit, helping to make the most of its existing human talent. The marriage of the productivity gains between capital and labor has resulted in regional growth rates that are likely to continue to outpace the U.S., Europe and Latin America.

Economists use Total Factor Productivity (TFP) to measure increases in economic growth not attributed to higher inputs in the volume of capital and labor. Accordingly, higher TFP reflects better use of capital and labor, as opposed to simply more capital and labor. The Asian Productivity Organization, which tracks economic data globally, reports that the U.S. generated average annual TFP growth of 0.8% over a recent 46-year period from 1970 to 20161. In comparison, roughly half of all Asian economies generated higher TFP growth than the U.S. during the same period, according to the group's research. Turning to Asia's largest economy, China generated average annual TFP growth of roughly 3% over the same period, meaning that China has consistently generated higher economic output with existing resources.

Notably, TFP comes from the private sector and represents the collective efficiency of individual companies (and their human capital) within a broader economy. From a bottom-up research perspective, we find that companies driving Asia's productivity boom include software makers, online platforms and cloud storage providers for small and medium-sized enterprises. As active portfolio managers, we also see opportunities in companies that invest heavily in R&D and compete on intellectual property and brand differentiation and awareness.

Small Companies Signal a Healthy Ecosystem

Small companies serve a vital function in entrepreneurial economies by feeding creativity, new ideas and innovative services into domestic and regional markets. The entrepreneurs running small companies in Asia today are very different than earlier generations of business owners, both in terms of human capital and financial capital. Asia's productivity boom allows small companies to do more with less, as labor and capital come together in interesting new ways.

Human capital—representing the skills, knowledge, networks and backgrounds of entrepreneurs—is a major driver for the growth and success of small companies. Many entrepreneurs are highly educated, have hands-on experience running prior businesses and are primed to take advantage of increased digital and physical connectivity throughout the region. What's more, entrepreneurs often bring knowledge and business acumen acquired from previously working for global multinationals.

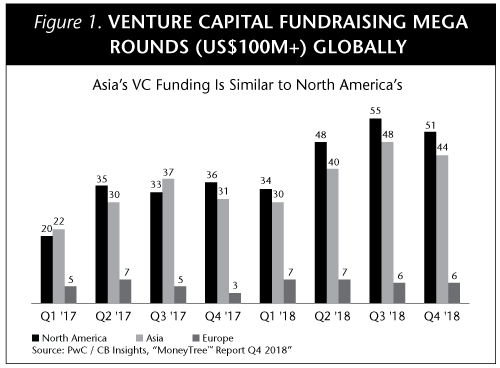

To match this influx of human talent, we see more sources of long-term financing for smaller companies, including venture capital. (See Figure 1.) Venture capital firms from Japan, South Korea and China are making significant investments in start-ups across the region. Venture capital tends to be focused on innovation, rather than manufacturing. Venture capital also tends to be “stickier,” meaning it is earmarked for long-term investment.

Software is a good example of a business solution that can help drive productivity. Business-to-business software companies often specialize in meeting the needs of specific industries, such as health care, real estate or accounting. Because decision-making is more data driven, small companies can better allocate resources when using software. When businesses run more efficiently and can generate more business with their current resources, the added GDP growth isn't coming from building bridges or airports, examples of classic infrastructure investments. Rather, extra growth comes from maximizing human talent and allowing businesses to do more with smaller teams.

Small companies are a vital part of Asia's economic engine. Productivity gains powered by small companies throughout the region create interesting opportunities for investors looking to capture Asia's growth. We believe Asia's smaller companies offer attractive return potential, while offering investors the opportunity to gain highly differentiated portfolio exposures.

Lydia So, CFA

Portfolio Manager

Matthews Asia

Innovative Companies Invest in R&D for Growth

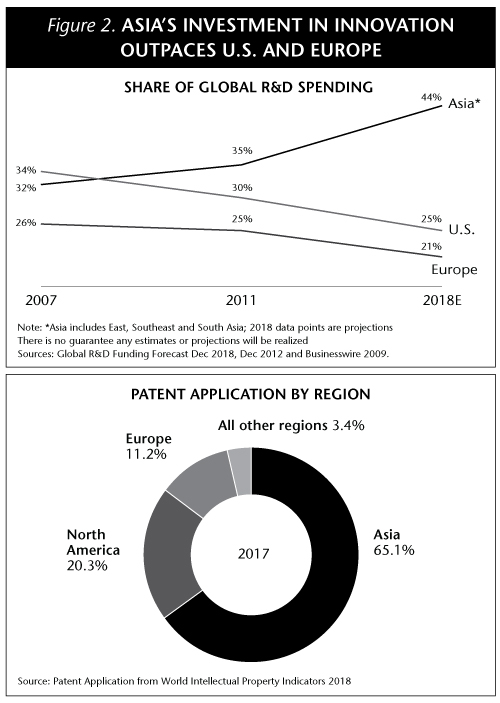

Innovation continues to be a major driver of economic growth, as Asian companies currently spend more on R&D than their peers in the U.S. and Europe. (See Figure 2.) Increased R&D spending is a logical investment for companies with a rapidly growing customer base and a need to differentiate themselves from competitors. As labor costs continue to rise across many parts of Asia, there is also organic demand for technology solutions designed to improve productivity. Factory automation is becoming more common. Digital platforms use artificial intelligence to suggest purchases for consumers. People purchase and access entertainment via mobile devices. All of this allows companies to become more productive.

Innovative companies in Asia drive productivity gains, as well as benefit from them. When conducting bottom-up research into these companies, an important factor to consider is a company's research & development (R&D) spending. We believe measuring a firm's spending on R&D relative to total revenue can be an important indicator of its long-term growth potential. We also find that examining the proportion of revenue from new products can reveal a company's level of success in generating marketable intellectual property. When a company has higher revenue from new products, its R&D investments have generated an attractive payoff.

When identifying investment opportunities, we search for companies with structural opportunities for growth. In the health care sector, for example, doctors and health care providers deliver medical consultations via mobile phones. The opportunity is structural because demand for health care services naturally rises as incomes rise for the middle class. Delivering consultations via mobile phone is an effective way to increase access to care for patients who may not live close to a hospital. Offering mobile consultations is a productivity enhancer because a doctor can see more patients in a day. Innovative companies can create more profitable business models through investments in R&D.

By 2030, Asia's middle class is expected to fuel about US$36.6 trillion in annual purchases, compared to US$12.5 trillion for Europe and $6.7 trillion for North America.2 As Asian consumers enjoy rising disposable income levels, we expect to see changes in consumption patterns and behavior in which discretionary items would take a larger portion of spending than basic necessities. With Asia's fast-changing consumer market expected to be larger than North America and Europe combined, continued innovation creates new markets and improves productivity. Rising efficiency is an important driver of Asia's growth.

Michael J. Oh, CFA

Portfolio Manager

Matthews Asia

Sustaining Productivity Growth

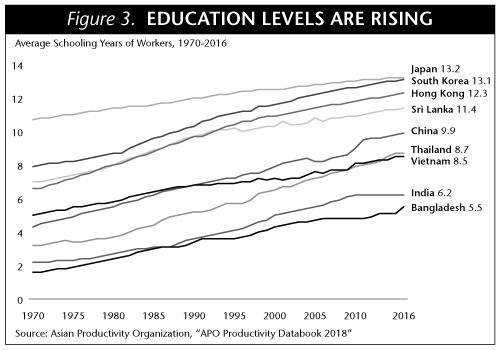

Productivity has two inputs—labor and capital. Sustaining productivity gains requires advancing the knowledge and skill of the region's labor pool, as well as improving how businesses deploy and reinvest capital. Looking at labor trends, education levels in Asia have been steadily rising for the past three decades. Even within advanced economies in Asia, such as Japan and South Korea, families continue to invest in more years of education for younger family members. (See Figure 3.) Turning to capital allocation, the trends are also encouraging. Rising investment in R&D, improvements in the quality of company boards and a greater emphasis on corporate governance and shareholder rights continue to generate gains in capital efficiency.

Value Investors Add Tech to the Mix

When bad news happens to good companies, value investors look to buy quality growth stocks at a discount. In Asia, many of these investment opportunities originate with companies employing capital-light business models that in turn help drive the region's productivity gains. This is particularly true in the technology sector, where digital platforms are creating virtual marketplaces that require no brick and mortar walls and no clerks or cashiers.

As a big part of Asia's investment universe, the technology sector is a growing part of how value investors tap into the growth potential of the region. Marquee tech stocks in Asia rarely are inexpensive, but we are prepared to buy when valuations are attractive. A value framework, backed by fundamental research and careful security selection, can be a useful tool for identifying attractive long-term growth opportunities. To avoid overpaying for technology stocks, we assign a fixed, discounted purchase price for each technology company in our universe that would trigger a potential buying opportunity should a company's stock price fall to that level.

A good example of how Asia's tech companies are fueling productivity gains are digital payment systems. Digital payments help reduce friction when consumers make purchases, facilitating a greater number of transactions and helping to generate higher economic growth. The volume of digital transactions across Asia today simply could not be handled using cash. Digital payments benefit the business-to-consumer segment, as well as business-to-business service providers. Micro-merchants, including businesses with only one or two employees, can pay their vendors with mobile payments, improving the ease of doing business.

A key difference between the region's current business leaders versus earlier generations is that newer business models tend to be capital-light. In the past, to make a huge impact on society, you needed a lot of capital and many employees, such as with steel mills, railroads or cement plants. Today, Asia's economies have moved from physical to digital infrastructure. A company with only a few thousand employees can become a dominant player in its industry. Technology companies benefiting from Asia's productivity growth are increasingly becoming part of the investment mix across the style spectrum, including value-oriented investment approaches.

Beini Zhou, CFA

Portfolio Manager

Matthews Asia

1 Source: Asian Productivity Organization, “APO Productivity Databook 2018”

2 Source: Homi Kharas, 2017, The Unprecedented Expansion of the Global Middle Class: An Update

The views and information discussed in this report are as of the date of publication, are subject to change and may not reflect current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. Investment involves risk. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Past performance is no guarantee of future results. The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information.

© Matthews Asia

© Matthews Asia

More Fixed Income Topics >