This isn't the time in the cycle to take excessive risk. The easy money has already been made. Astoria's 2019 playbook is as follows: late cycle economic forces + desynchronized global growth + a deteriorating earnings cycle = the need for more defensive posturing across stocks and bonds.

Astoria has been vocal about owning higher quality stocks in 2019. Why? Companies with above average ROE/ROA and increasing profitability should be rewarded in an environment when earnings are declining.

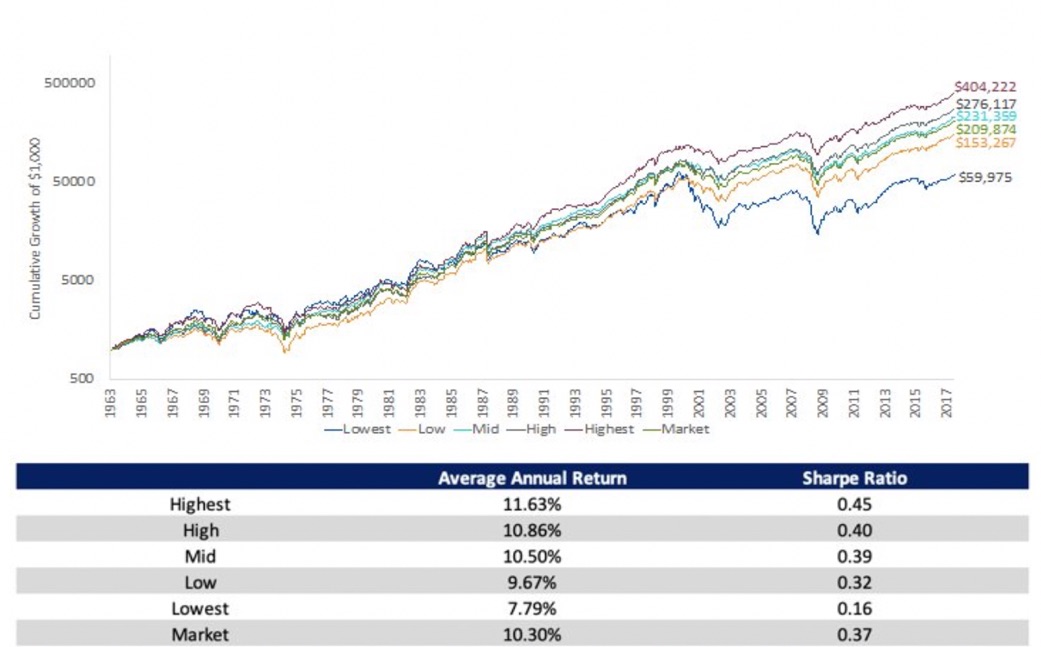

Second, higher quality stocks have historically outperformed lower quality stocks (see chart below). Since 1963, the highest quintile of U.S. profitable companies has returned 11.63 percent while the lowest quintile has returned 7.79 percent. Higher quality companies have also outperformed the market which returned 10.30 percent over this time-period.

Source: Kenneth French Data Library, with data as of 12/31/17, WisdomTree. Period based on the availability of operating profitability returns sorted into quintiles, beginning 6/30/63. The universe is U.S.-listed equities grouped based on operating profitability. Past performance is not indicative of future results. Sharpe Ratio: Measure of risk-adjusted return. Higher values indicate greater return per unit of risk, specifically standard deviation, which is viewed as being desirable.

There are some key differences amongst Quality ETFs. Utilizing quantitative portfolio construction tools and aggregating the underlying fundamentals to determine the optimal ETF for your portfolio is crucial.

The key message from Astoria is to pick high quality stocks with strong balance sheets which have demonstrated the ability to grow their earnings regardless of the prevailing macroeconomic conditions. We find that DGRW (WisdomTree US Quality Dividend Growth ETF) and QUAL (iShares Edge MSCI USA Quality Factor ETF) have relatively higher factor loadings and have more balanced sector weights compared to some of the other larger Quality ETFs.

2019: The Year of the Quality ETF?

We believe Quality ETFs will take in more assets than any other factor category in 2019.

As of mid February, U.S. listed Quality ETFs have taken in approximately two billion in assets. While this may not appear significant, the entire equity ETF universe has seen approximately $20 billion of outflows in 2019.

Astoria originally pegged quality as one of our key 2019 themes in our January 3rd blog and reiterated it our year ahead outlook on January 8th. We like high quality stocks for the following reasons:

- The earnings cycle is deteriorating and companies with above average ROE/ROA and increasing profitability are likely to be rewarded more on a relative basis.

- The quality factor has historically shown to be robust, pervasive, and has been persistent over time.

We believe 2019 will be more defensively driven due to global growth becoming more desynchronized, the earnings cycle is deteriorating, late cycle economic forces, and elevated macro risks (trade tariffs, Brexit, China slowdown, etc).

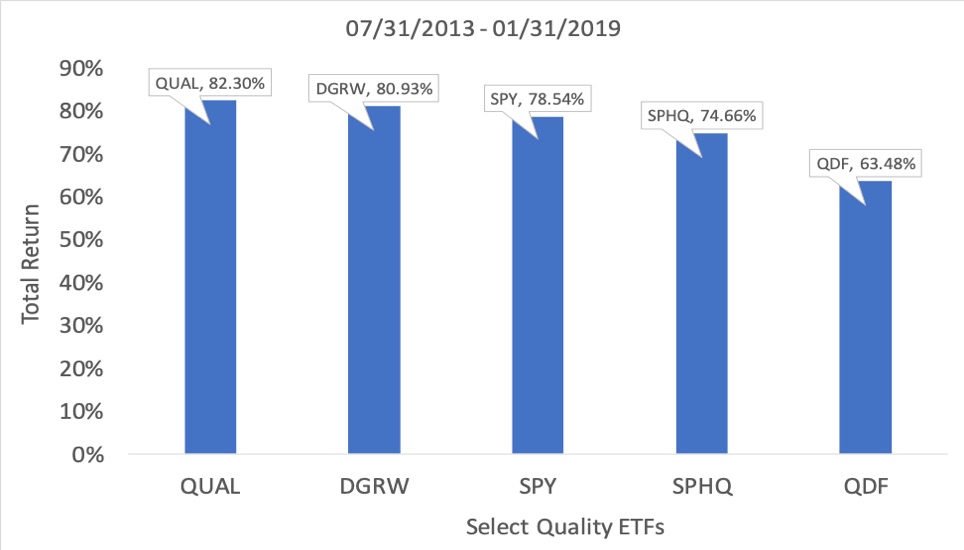

DGRW and QUAL Have Outperformed the S&P 500 Over the Past Five Years Despite a QE Induced Rally

Let’s dive deeper into the some of the larger Quality ETFs.

- 4 of the larger Quality ETFs have shown considerable performance differences over the past five years. This speaks to the point that not all Quality ETFs are created equal and investors need to understand the underlying index methodology and look at the portfolio’s risk characteristics.

- QUAL (iShares Edge MSCI USA Quality Factor ETF) and DGRW (WisdomTree US Quality Dividend Growth ETF) have done notably better than QDF (FlexShares Quality Dividend ETF) and SPHQ (Invesco S&P 500 Quality ETF) since July 2013.

Source: Bloomberg

- o Over the past 5 years, the U.S. economy has had varying periods of acceleration and slowdowns, but the general trend has been cyclicals outperforming defensives.

Source: Bloomberg

Not All Quality ETFs are Created Equal

As the Chief Investment Officer of Astoria, I have spent 20 years in the ETF ecosphere doing portfolio construction research, analyzing ETFs, and structuring portfolios for investors. Picking the right Quality ETF isn’t a trivial task.

Astoria has a unique value proposition in the ETF model portfolio space. We leverage extensive amounts of technology, software, and risk models to analyze the underlying ETF portfolio risk characteristics.

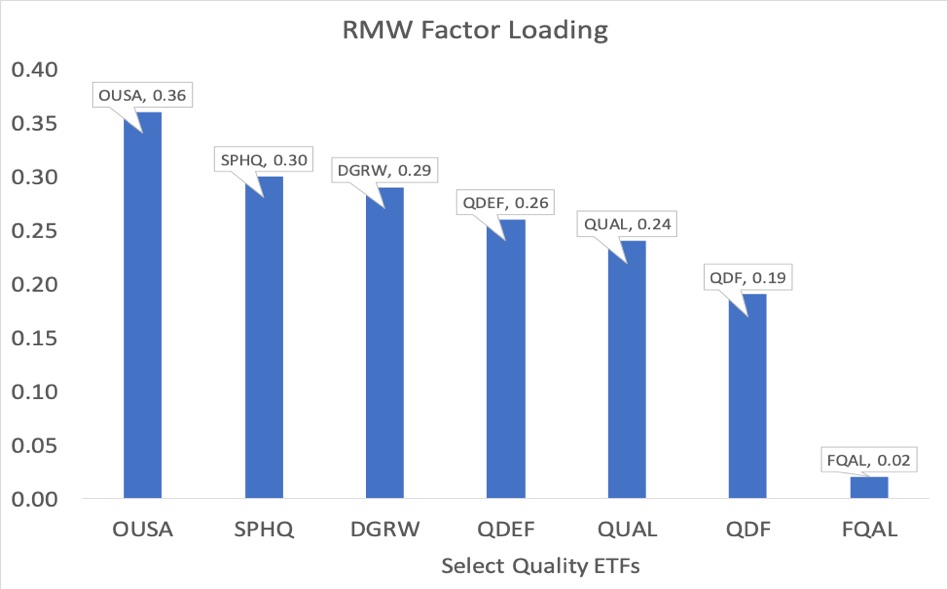

Amongst the two largest Quality ETFs, DGRW provides a slightly higher factor loading (RMW) compared to QUAL. There are two other ETFs, OUSA (O'Shares FTSE US Quality Dividend ETF) and SPHQ (Invesco S&P 500 Quality ETF), with a higher factor loading than DGRW.

Data Source: PortfolioVisualizer.com. (RMW) Robust Minus Weak: The profitability premium. Data retrieved on February 7th, 2019.

Below is a table showing the 5 factor loadings for the larger Quality ETFs.

Data source: Portfolio Visualizer. Data for DGRW, QUAL, QDF, SPHQ, and QDEF is based on the time period August 2013 through December 2018. Data for OUSA and FQAL is based on the time period October 2016 through December 2018.

Comparing the Two Largest Quality ETFs

DGRW (WisdomTree US Quality Dividend Growth ETF)

DGRW applies a quality and a growth screen when constructing the portfolio. In Astoria’s view, this is particularly attractive as we don’t necessarily think investors should be ignoring growth stocks but instead picking securities which have both growth and quality characteristics.

- The earnings growth ranking is 50 percent of the portfolio construction process and is derived from companies’ long-term earnings growth expectations.

- The quality ranking is the remaining 50 percent of the screening process and is split evenly between a three-year average return on assets (ROA) and the three-year average return on equity (ROE).

- DGRW removes companies with higher dividend yields. The logic here is that if companies are paying out more than they earn, companies may have to cut back their dividends in the future.

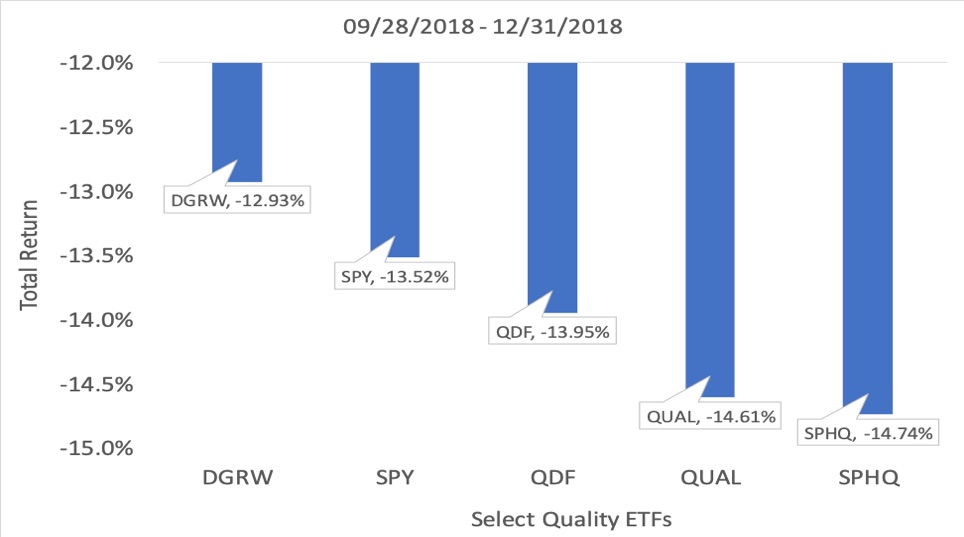

- During the heightened volatility of Q4 2018, DGRW outperformed the larger Quality ETFs between 100-180bps (see chart below).

Source: Bloomberg

- In our view, these are substantial return differences considering investors are quick to rotate amongst ETFs because of a few basis point difference in management fees.

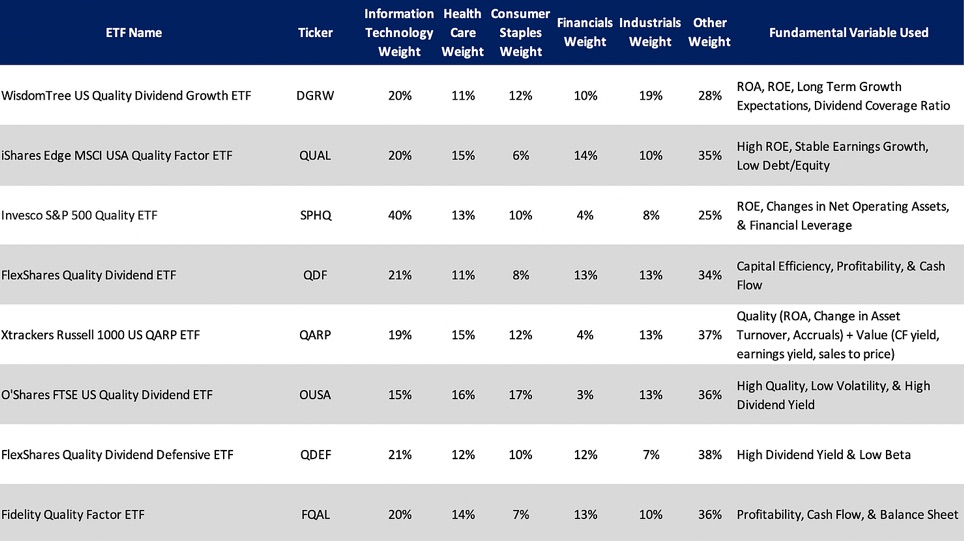

- DGRW’s top sector exposures are Information Technology (20 percent), Industrials (19 percent), and Consumer Staples (12 percent).

QUAL (iShares Edge MSCI USA Quality Factor)

- QUAL tracks an index of U.S. large and mid-cap stocks. The stocks are selected and weighted by high ROE, stable earnings growth and low debt/equity.

- In our view, QUAL also has a sound methodology and has been the clear leader so far with nine billion in assets in the Quality ETF space.

- QUAL tends to be more concentrated with only 120 stocks or so.

- There are some notable differences in the constituents and their weights for QUAL and DGRW so investors need to be comfortable with the portfolio risk characteristics when deciding between both ETFs.

- QUAL’s top sector exposures are Information Technology (20 percent), Health Care (15 percent), and Financials (14 percent).

In the table below, we highlight some of the fundamental variables and sector weights for select Quality ETFs. Some factor ETFs will incorporate a quality metric in their screening methodology, but the focus isn’t quality per se. We’ve skipped those for the time being.

Source: ETFAction.com. Refer to each of the ETF’s respective index methodology for more details.

Best, John Davi

Founder & CIO of Astoria

John Davi has 19 years of experience spanning across Macro ETF Strategy, Quantitative Research & Equity Derivatives. Prior to Astoria, John spent 8 years as the Head of Morgan Stanley’s Institutional ETF Content where he advised many of the world's leading investment management firms in macro / quantitative ETF portfolio construction and implementation. John spent 10 years at Merrill Lynch as an Equity Strategist. In 2017, John founded Astoria Portfolio Advisors, an investment management firm that specializes in Quantitatively driven and Cross Asset ETF portfolio management. Astoria’s competitive edge is our research, our deep portfolio construction background and our ETF product expertise.

You can reach John Davi at [email protected] or @AstoriaAdvisors. ETF holdings shown are for illustrative purposes only and are subject to change at any time. For full disclosure, please refer to our web site: www.astoriaadvisors.com/disclaimer.

© Astoria Portfolio Advisors

Read more commentaries by Astoria Portfolio Advisors