Amid fears of escalating trade tensions, the yuan’s sharp depreciation against the dollar last month has spooked some investors who see similarities with China’s currency devaluation in 2015, an episode that prompted capital outflows and roiled markets worldwide. Yet despite the similarities, differences in the macroeconomic backdrop suggest the global repercussions will be more limited this time.

Similarities

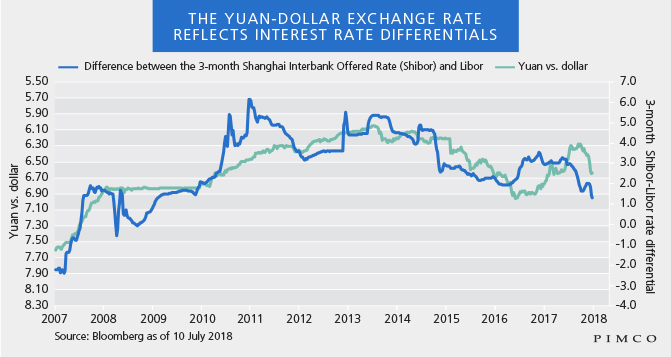

Both episodes shocked markets. Over the past 12 months, the yuan had fallen against the dollar but at a relatively stable pace. Yet in the three-week span following the Federal Reserve’s 13 June interest rate hike and subsequent dovish moves from the People’s Bank of China (PBOC), the yuan plunged as much as 5.0%. The devaluation on 11 August 2015 was even more abrupt: The yuan dropped by 2% in a single day as markets reacted to the unexpected de-pegging of the Chinese currency from the U.S. dollar (see chart).

The yuan’s decline in both cases also reflected worsening macroeconomic pressures. Three years ago, it was the crash of China’s A share market and cascading margin liquidation that compounded acute growth-deflation pressure. The recent move reflects escalating trade tensions with the U.S. and policy-induced domestic debt deleveraging.

Finally, both episodes occurred when the yuan was slightly overvalued. Interest rate differentials between the yuan and dollar were narrowing when the PBOC eased policy on 25 June by cutting banks’ required reserve ratio. Meanwhile, the Federal Reserve remains on its tightening path.

Differences

The key difference between the episodes, of course, is trade relations with the U.S. On 5 July, Washington imposed 25% tariffs on an initial $34 billion of merchandise, prompting an immediate tit-for-tat response from Beijing. We estimate U.S. tariffs will trim 10-20 basis points off Chinese GDP. The threat of 10% tariffs on an additional $200 billion of Chinese goods could inflict further damage.

Although the PBOC has categorically ruled out using foreign exchange policy as a trade tactic, a more market-driven exchange rate will inevitably reflect negative fundamentals. For instance, a trade compromise between Beijing and Washington, should we see one, would almost certainly entail a sizable reduction in China’s $300 billion surplus. (China’s current account has shrunk to near zero, a sharp drop from 2.7% of GDP in 2015.)