Italy may have a government, but the country's problems haven't gone away. That's a worry for the eurozone.

Italy has a new government. For now, crisis has been averted. But that doesn’t mean the political and market turmoil is over. Like a virus, the threat of a eurozone break-up triggered by Italy will linger for years to come. And this risk is likely to remain factored into asset prices.

With the agreement of a coalition between the populist Northern League and Five Star Alliance, the febrile mood that infected Italian politics and markets has suddenly cooled. Now that talk of anti-euro policies is no longer making headlines, investors are able to turn their focus back to some of Italy’s more positive fundamentals. After years of stagnation, the economy is growing at more than 1 percent in inflation adjusted terms. The current account is showing a surplus of more than 2 percent of GDP. As is the fiscal balance, once adjusted for the economic cycle and interest costs.

Reforms to the labour market and other areas of the economy are being implemented.

Italy’s debt profile is also not quite as troubling as the headlines suggest. The average duration of Italian government’s liabilities has lengthened, while domestic investors hold the lion’s share of this debt.

Finally, membership of the euro is popular among Italians – the latest survey shows 70 percent support.

Italy, then, is no Greece. But over the long run, that’s precisely its problem. It would be too big to save if its debts became unsustainable. And there remains a residual risk that the euro zone’s third largest economy will end up triggering a breakup of the euro – whether by design or accident.

In part that’s because the Italian economy is still uncompetitive relative to the single currency’s other big hitters. Italy also has among the lowest ratios of working age to total population of all major developed countries, at under 65 percent compared to an average of 66.4 percent for the OECD overall. And with a low birth-rate and aging population – 21 percent of Italians are over 65 – that proportion will only get worse. Italy has one of the world’s worst labour productivity rates and only Greece has lower GDP per hour worked in the OECD. Our fair value estimates suggest that were Italy to adopt a new, floating currency, it would immediately have to devalue by up to 30 percent to regain lost competitiveness.

Meanwhile, the rise of populism has in large part been a reaction to a flood of migrants and asylum seekers from Africa and the Levant. These factors are likely to set Italy’s new government on a collision course with the European Commission. With domestic growth prospects relatively poor, it wants to pump the economy with a big fiscal spending programme, which means government budget deficits. The latest estimates are for an additional EUR120bn of spending, which is around 7 percent of GDP.

This would necessitate EC approval – which is unlikely to be forthcoming given that Italy already has Europe’s highest debt to GDP ratio of over 130 percent. Brussels – and most crucially Germany – is unlikely to tolerate deficits incompatible with the stability of Italy's debt to GDP ratio. Any drop in the country's primary surplus below around 0.6 percent from the current 1.9 percent is like to contravene the EU's fiscal compact. At the same time, the new Italian coalition will want the rest of the EU to take a bigger share of the migrant burden. This too is likely to be fraught, not least because the likes of Germany have also tilted towards populism in response to their own immigration problems.

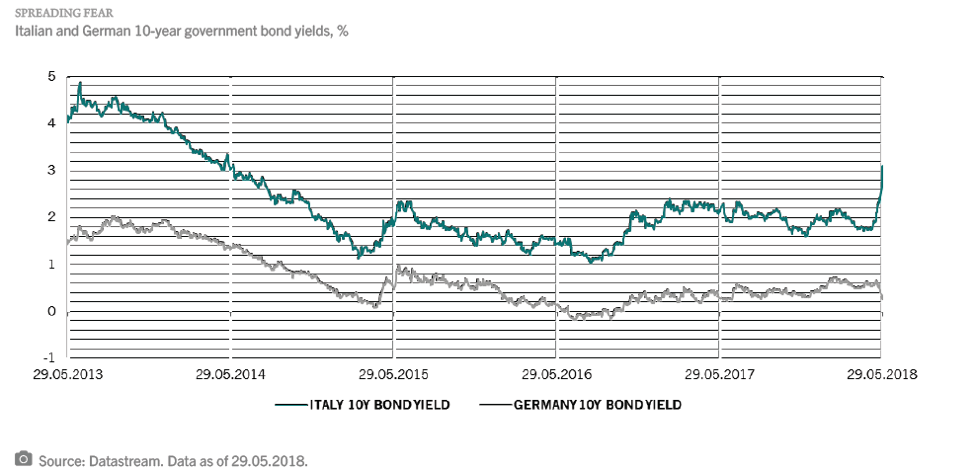

The upshot is that the market is unlikely to return to previous complacency. As recently as April, bond investors were assigning virtually zero risk to breakup of the eurozone. By May 29, the gap in yields between Italian government bonds (BTPs) and their German equivalents had widened to effectively discount a one in five chance that Italy would leave the euro, according to our proprietary model. That may still only have been half the 40 percent probability reached during the 2011-12 crisis, but it was significant. And though it’s shrunk with the subsequent rally, the risk won’t disappear altogether – the current spread is just over 200 basis points, leaving the probability of Italiexit at around 5 percent.

Because Italian banks, while well capitalized, have large holdings of Italian government bonds, even this gauge might underestimate the potential for eurozone fragmentation. According to the Bank for International Settlements, BTPs account for 20 percent of Italian bank assets. That’s among the highest levels in the world.

Our estimates suggest that every 100 basis point widening in the BTP/Bund yield spread reduces Italian banks’ capital by 30 basis points. A 300 basis point widening could begin to cause the sector serious discomfort, not least because sovereign bond losses could spark deposit outflows and make it difficult for banks to sell on non-performing loans.

Whatever happens, a lasting Pax Romana seems unlikely.

© Pictet Asset Management

© Pictet Asset Management

Read more commentaries by Pictet Asset Management