Back in 2014, PIMCO developed the concept of The New Neutral as a secular framework for interest rates. After the financial crisis, the global economy entered a new regime in which the equilibrium (i.e., neutral or natural) policy rates needed to ensure trend growth and at-target inflation would be much lower than their historical levels. In the U.S. specifically, we argued that the real neutral policy rate would likely be close to zero, implying a nominal rate close to 2% (for details, see “Navigating The New Neutral”). This concept of much lower equilibrium rates has described the macro landscape well in recent years, as markets progressively priced in a shallower path of rate increases and a lower peak for policy rates.

With global growth having been steady for several years, and inflation on a gradual upward path, many investors are raising questions about the appropriate level, path and destination of monetary policy. In the U.S., for example, one may wonder whether an economy that grows around 4% in nominal terms for a sustained period warrants an equilibrium nominal policy rate of around 2%.

While we will dive deeper into this question at PIMCO’s upcoming Secular Forum in May, we believe The New Neutral remains a valid anchor for interest rates over the medium term. The key drivers of low equilibrium rates – including demographic trends and the high level of leverage in the global economy – have not substantially changed:

-

Global demographics. A fall in fertility rates and higher life expectancy will lead to an overall aging population and slower working-age population growth. These weak demographics lower neutral rates through several channels: Slower population growth weakens labor force growth and in turn potential; a shrinking population lowers economy-wide investment in capital, weakening growth potential; higher life expectancy raises people’s ex ante desire to save. Against this, an expected drop in the global dependency ratio (the ratio of non-working-age to working-age population) should lower saving ratios, but this is likely to be a super-secular rather than secular demographic shift.

-

High debt across public and private sectors. High debt pushes down the neutral rate by increasing economic agents’ ex ante desire to save, given the focus on debt reduction; by raising the economy’s sensitivity to monetary policy and in particular to interest rate increases; and by tying the hands of central banks, which need to take debt sustainability into account when setting monetary policy.

In this piece, we focus on the second driver – high debt – in examining recent global trends and how they inform PIMCO’s New Neutral and broader investment views.

Global debt still on the rise

In order to gauge developments in global debt, we review data from the Bank for International Settlements (BIS). The BIS compiles data on a quarterly basis for more than 40 different economies, ensuring consistency in the approach for measuring debt across countries.

The main variables we focus on here are the total level of debt in the nonfinancial sector (comprising households, nonfinancial corporates and government) and the level of private nonfinancial debt (comprising households and nonfinancial corporates), both measured as a share of GDP. Financial instruments included in debt measures are bank loans and debt securities (plus currency and deposits in the case of government debt). A review of these aggregates across regions reveals the following trends:

-

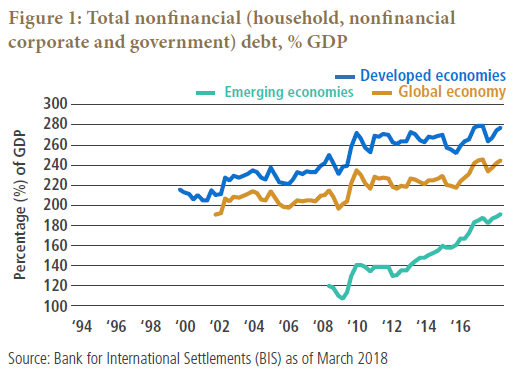

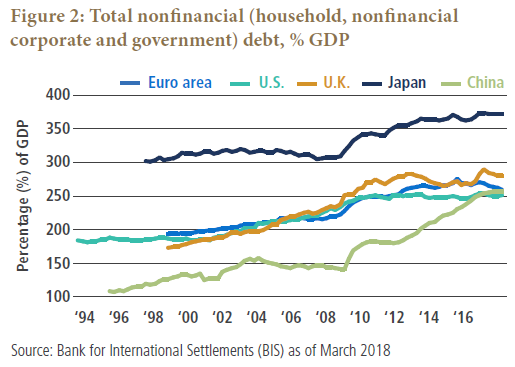

Total nonfinancial debt (Figures 1 and 2) has kept rising globally in recent years, from just over 200% of global GDP in the years preceding 2008 to over 240% currently. Debt increased across both developed market (DM) and emerging market (EM) economies, with the increase across EM countries proving particularly steep: from around 120% of GDP in 2008 to around 190% currently. The key driver of the rise in EM debt has been China, where total debt rose by a staggering 110 percentage points of GDP, from around 150% in 2008 to nearly 260% today. Across DM countries, debt has been rising across most major economic areas (eurozone, Japan, U.K.), and has been broadly stable at a high level in the U.S.

-

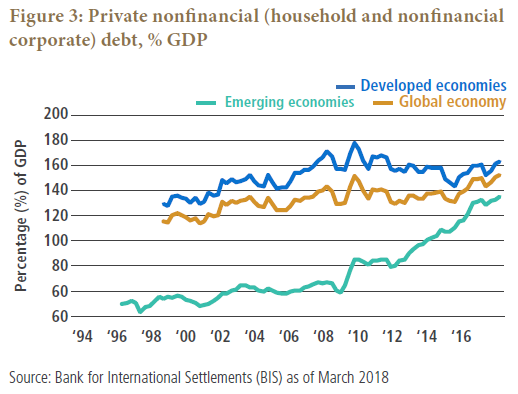

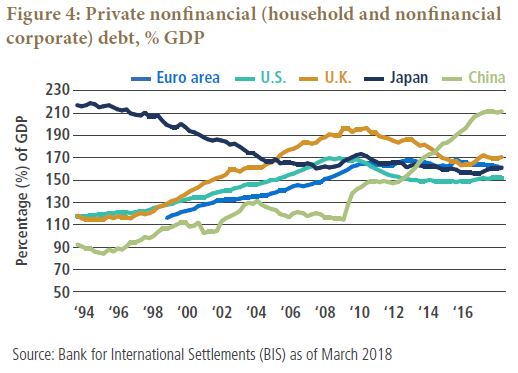

Private nonfinancial debt (Figures 3 and 4), an important aggregate when it comes to monetary policy transmission, has also risen globally at the margin, from around 140% of GDP in 2008 to nearly 160% currently. Private debt is rising steeply in EM countries (with China leading the way). Within the DM complex, private debt has been reduced in the U.S. and U.K. and remained largely stable at a high level across the eurozone and Japan.

Overall, not only has the debt overhang from the credit expansion in the run-up to the financial crisis not been corrected, but it has arguably gotten worse. This is not to say that there haven’t been pockets of improvement: There has been meaningful deleveraging in the U.S. household sector, and progress in deleveraging across the private nonfinancial sector in the U.K. and in parts of the eurozone. But debt overall (both total and private) has continued to rise globally, with a particularly steep increase seen in EM countries.

Falling debt service ratios: a partial, contingent saving grace

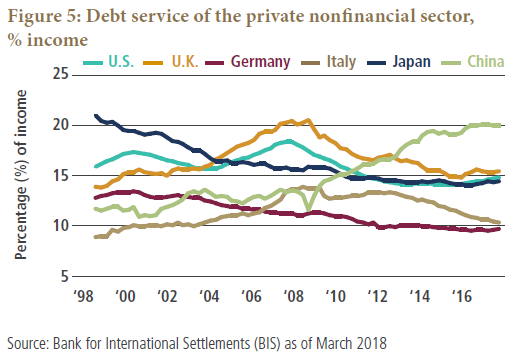

An encouraging aspect to consider is that debt service ratios (defined by the BIS as interest expenses and amortizations as a share of income) have generally come down across the DM in recent years. The fall in service ratios has been linked in part to the exceptional easing of monetary policy, alongside generally compressed credit spreads.

While this development is positive overall for the health of the global economy, it is only a partial and contingent saving grace, for two reasons (see Figure 5). First, the picture is quite different across the EM complex, where private debt service ratios (calculated once again by the BIS) have been rising in several countries, most importantly in China. Second, the persistence of low debt service ratios is dependent on interest rates remaining low, reasserting the relevance of our New Neutral view, and making a return to “old normal” levels of rates very unlikely.

Risk of debt bubbles and bursts mostly concentrated in the EM complex

Having established that debt remains high and dependent on low rates for its affordability, it is worth asking whether there are fragilities building globally that could trigger a new banking or financial crisis.

One way to assess financial fragilities is to look at how debt has developed relative to recent historical trends. For monitoring potential bubbles, this metric is informative since a relatively low level of debt can still pose challenges if it has experienced a steep increase over a short period of time. Similarly, a high level of debt need not signal a bubble if it has been maintained for a long period of time.

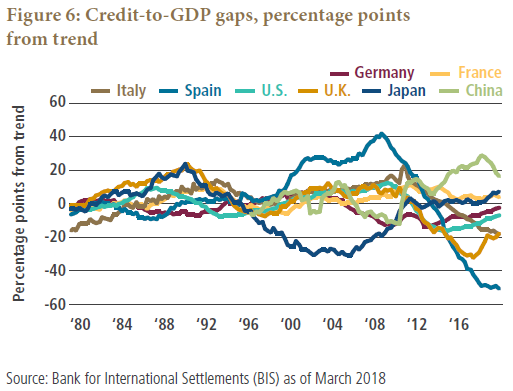

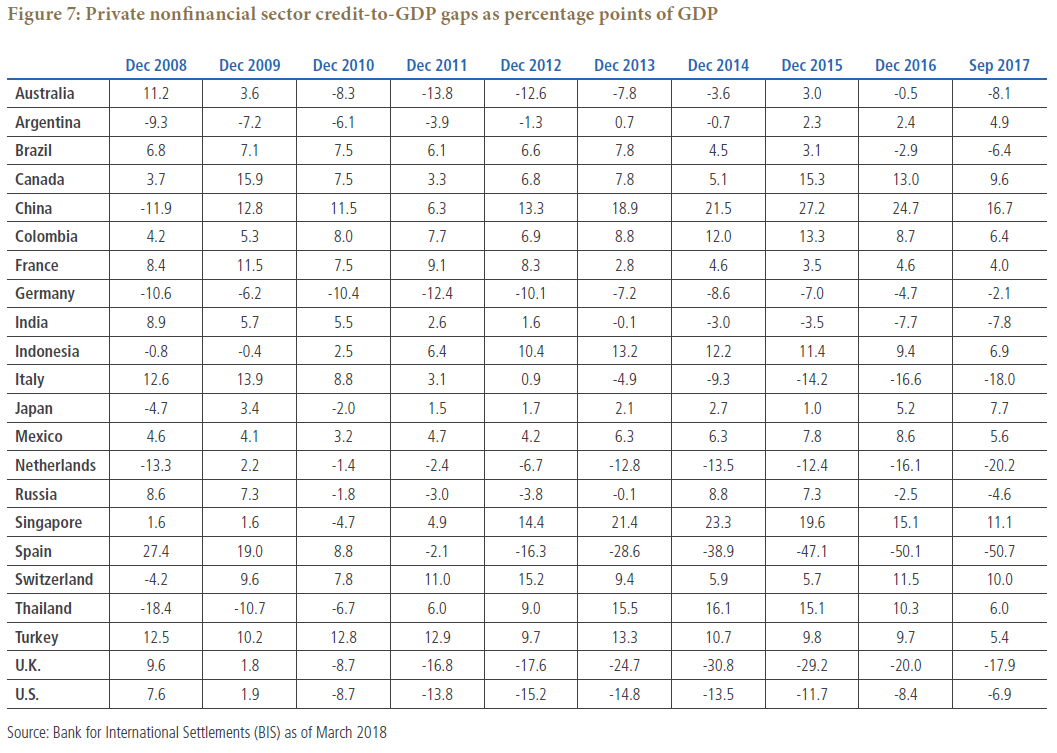

BIS data (once again) are useful for this analysis. In an effort to monitor banking sector risks, the BIS creates credit-to-GDP gap measures. These gaps represent the difference between household and nonfinancial corporate debt as a percentage of GDP in a given country and its recent trend, where the trend is calculated using the Hodrick-Prescott filter statistical methodology.

According to these data (see Figures 6 and 7), credit-to-GDP gaps are close to zero or negative across most DM countries, with the exception of France, Canada, Japan and Switzerland. The picture is quite different in EM, where many more countries have positive (and generally larger) gaps, including China, Hong Kong, Indonesia, Singapore, Mexico, Malaysia, Turkey and Thailand.

The gap of over 16% GDP in China is of particular concern given its economy’s global influence. Against that, note that a good portion of the rise in nonfinancial corporate debt in China has been driven by state-owned enterprises, which can likely count on the backing of the cash-rich sovereign.

Overall, the data suggest that risks of bursting debt bubbles look contained in DM countries, but that there are several hotspots that warrant close monitoring in the EM complex.

Benchmarking interest rates for government debt sustainability

As mentioned above, one of the ways in which debt affects equilibrium policy rates is through central banks taking debt sustainability into account when setting monetary policy.

To benchmark this view, we can run a mathematical exercise to derive the interest rates required in the future to stabilize government debt/GDP ratios at current levels. We use a simple debt/GDP dynamic equation:

Δ debt = ( i − g ) x debt − pb

“Debt” is government debt/GDP (“Δ” being the change in this variable), “i” is the average nominal interest rate paid on debt, “g” is nominal GDP growth and “pb” is the government’s primary balance (i.e., the budget balance excluding interest payments) measured as a share of GDP.

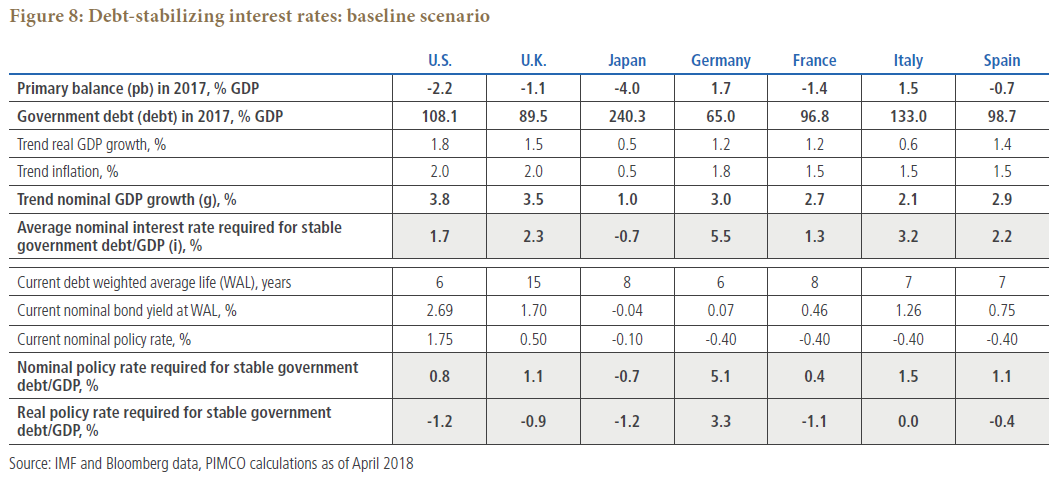

In the exercise, we then find the level of “i” that is required for “Δ debt” to be equal to zero, assuming that the primary balance is unchanged going forward from its 2017 level (latest data available); that real GDP growth and inflation move in line with trend (where trend estimates are PIMCO’s); and taking today’s level of “debt” as the starting point (see Figure 8 below for more details).

Next, we convert the interest rate paid on debt into a policy rate by looking at the current spread between government bond yields with maturities in line with the current debt stock’s weighted average life (six years in the U.S., for example) and the current policy rate. This effectively assumes that the shape of the yield curve does not change going forward (note that a rise in term premia, which are currently very depressed, would further lower the level of policy rates required to stabilize debt).

What we find is that average nominal borrowing rates consistent with a stable government debt/GDP ratio are 1.7% in the U.S., 2.3% in the U.K., −0.7% in Japan, 5.5% in Germany, 1.3% in France, 3.2% in Italy and 2.2% in Spain (see Figure 8; these are average rates across existing maturities). When we translate these into nominal policy rates, central bank rates consistent with government debt stability are in the order of 1% in the U.S. and the U.K., −0.5% in Japan, 5% in Germany, 0.5% in France, 1.5% in Italy and 1% in Spain (for the eurozone, there’s only one policy rate set by the European Central Bank, and the weakest links should be considered most relevant in the analysis). Overall, the analysis suggests that policy rates need to remain very low to ensure that already high government debt/GDP ratios don’t increase further.

Focusing on the U.S. specifically, this analysis suggests the nominal policy rate consistent with debt stability needs to be around 1% in nominal terms, or −1% real (somewhere below our New Neutral estimates of around 2% nominal, 0% real).

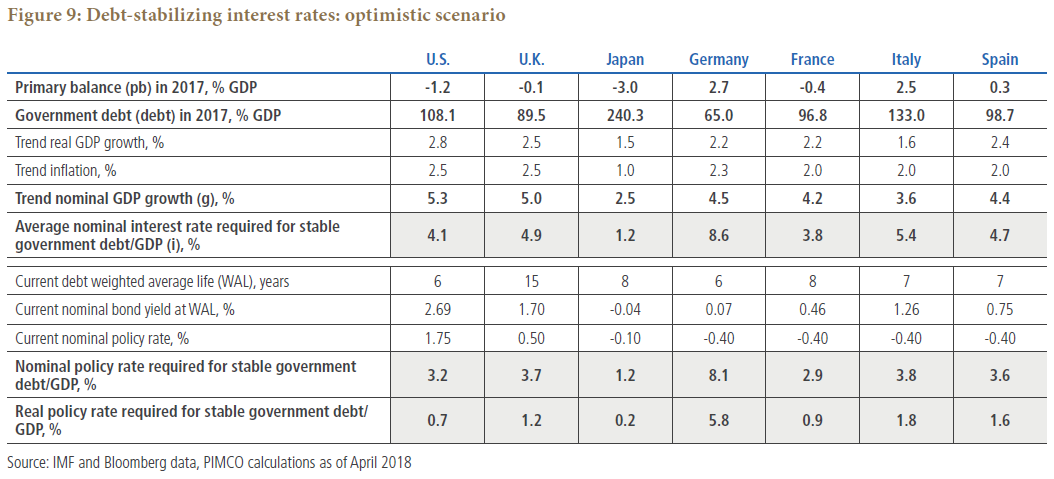

Interestingly, when we shock our exercise to include somewhat more optimistic macro assumptions (+1.0 percentage point on trend growth, +0.5 percentage point on trend inflation, and +1.0 percentage point on the primary balance – see Figure 9), we find that the U.S. policy rate consistent with debt stability increases but, at around 3% nominal and 1% real, it remains very low. This conclusion is similar for other countries, where rates consistent with stable government debt also remain low in the optimistic scenario.

While this analysis is partial in that it addresses only one aspect in which debt affects equilibrium rates (government debt sustainability) and does not allow for the possibility that debt could be allowed to increase somewhat further ahead, it highlights an important factor behind the need to keep rates low.

Conclusions and investment implications

The global economy remains highly levered, and sensitive to interest rate movements. Debt sustainability hinges on low debt service ratios, which in turn are predicated on persistently low interest rates. This will constrain central bank efforts to normalize rates and continue to lend support to our New Neutral view.

The persistence of The New Neutral has important implications. U.S. Treasury and German Bund yields can be volatile over the business cycle but, in a New Neutral world, duration valuations are likely to remain anchored. This suggests limited upside on Treasury yields ahead from these levels.

For risk assets, a key consequence of The New Neutral is that it tends to raise their net present value via a low long-term discount rate on cash flows. This would suggest that valuations may be less stretched than they appear. In this context, it is also encouraging that risks of financial bubbles bursting in developed markets in the near term look relatively low. That said, leverage hotspots in the EM complex continue to warrant close monitoring.

© PIMCO

Read more commentaries by PIMCO