Domestic

Summary

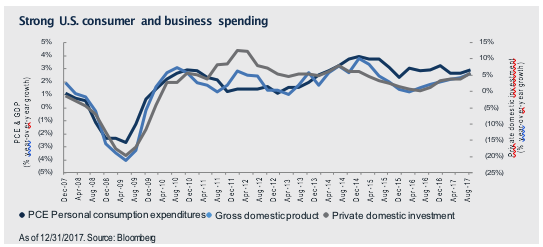

Consumer spending and business fixed investment remained strong, pointing to continued domestic economic growth. Notably, business fixed investment growth, represented by private domestic investment, accelerated to 5.4% year-over- year growth in the fourth quarter of 2017, from a low of 0.71% in the third quarter of 2016 (see chart below). Elevated consumer and business confidence surveys also support continued domestic economic growth. The Conference Board Consumer Confidence Index reached 130.0 in February 2018, a level not seen since December 2000. Likewise, the NFIB Small Business Optimism Index increased to 107.6 in February 2018, beating all previous readings except for the reported record high of 108.0 in September 1983. The elevated levels of these surveys underscore the strength behind both consumer and business activity.

Inflation remains benign with the U.S. Personal Consumption Expenditure Core Price Index sitting at 1.60%, well below the Federal Reserve’s stated inflation growth target of 2%. While we believe that inflation will likely move modestly higher over time, we expect that near-term data will continue to reflect subdued inflation.

Outlook

We anticipate that the U.S. GDP growth will continue and may accelerate further due to easier fiscal policies and global economic tailwinds. We currently estimate that U.S. GDP will grow 2.5%-3.0% in 2018; a rate which compares favorably with the 2.6% growth that the economy experienced in 2017.

The Federal Reserve continues to fulfill its dual mandate of full employment and stable prices. In that regard, we believe that slack in the labor force continues, although reported unemployment could fall further. Regardless, the unemployment rate has now held steady at 4.1% since October 2017, yet wage pressures remain very subdued. Labor force slack and lack of significant wage pressure should allow the Federal Reserve to avoid pursuing an overly aggressive rate hike path. We expect inflation to trend higher, although there remains significant question as to whether the stated target of 2% inflation will be reached this year.

International

Summary

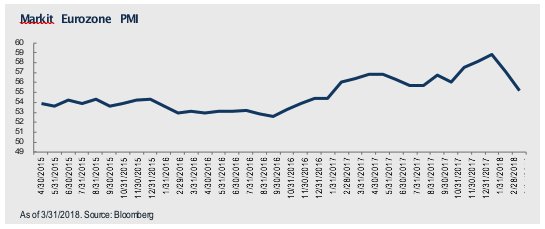

Despite the recent volatility in global equity markets, economies worldwide continue to grow at a healthy pace. However, we observe that economic growth may be moderating in some regions, especially in Europe, although the ECB continues to express confidence in the continuation of a healthy European economic expansion. Both the OECD and the IMF recently forecasted a slight acceleration in 2018 worldwide economic growth to +3.9%. The lack of significant headline inflation in the face of a broad global economic recovery has allowed interest rates to increase at a moderate pace. European interest rates in particular remain historically low, largely because of the influence of the ECB’s bond buying program. Surprisingly, in the face of record employment, wage growth has so far remained moderate. Lack of inflation pressure has also kept global yields muted for now, and the U.S. 10-year Treasury Note yield failed to reach 3% in the first quarter 2018 (it peaked at 2.95% on February 21, 2018).

Global monetary policy remains stimulative, with central banks still in easing mode. The two large quantitative easing programs outside of the U.S., in Japan and Europe, remain in place for now. Global fiscal stimulus also recently picked up with the passage in the U.S. of the Consolidated Appropriations Act, 2018 (a.k.a., the 2018 omnibus spending bill) and the Tax Cuts and Jobs Act of 2017, which will likely boost capital spending in 2018. Despite fears about a global trade war and other political instabilities, the recent stock market correction represents a healthy and overdue reversion from high valuations. We believe that the muted reaction of the bond markets during the equity market sell-off likely indicates that the volatility is temporary.

As noted above, we observe some weakness in recent European business confidence surveys. Notably, because of the structure of the eurozone as a whole and the restrictions imposed by the Stability and Growth Act, it is more difficult for governments there to implement timely fiscal stimulus through policy changes. If a European economic slowdown gathers momentum, it could weaken our global economic outlook. In addition, an economic slowdown in Europe may also exacerbate the fundamental political and social stresses that exist within the EU itself. Indeed, we note recent election results in Italy and Hungary, which on balance elected anti-EU parties to power.

Outlook

The positive fundamental outlook for global growth offsets lingering concerns regarding the length of the present cycle and we continue to anticipate higher global growth for 2018. U.S. corporate earnings reports for the first quarter of 2018 will likely reflect healthy fundamentals and provide incremental support to our favorable global economic outlook. The U.S. economic recovery is in its ninth year, which is extended by historical standards and has influenced economic growth worldwide. However, some analysts point out that the average rate of economic growth over this period has been half the rate of previous expansions, suggesting that the current cycle may continue.

We remain positive regarding global economic conditions and only somewhat concerned that a significant acceleration could put upward pressure on long-term U.S. rates. In the present recovery, the Federal Reserve has generally led the rest of the world, acting first to remove quantitative easing and raising short-term interest rates.

Currencies and commodities

Commodity price increases generally moderated in the first quarter of 2018, as the U.S. dollar traded in a relatively narrow range. We expect commodity prices to increase gradually, supported by growing global industrial production. Moderate commodity price increases are unlikely to push headline inflation significantly higher given the excess of global production capacity. The U.S. dollar may be vulnerable to widening budget and trade deficits in the near term. The U.S. trade deficit will likely worsen in the short term if the U.S. economy continues to accelerate, regardless of any trade negotiation outcomes.

Sector analysis

U.S. interest rates

The yield curve initially steepened in the first quarter of 2018. However, subsequent trading contributed to an overall flattening of the curve as the spread between 2-year and 10-year U.S. Treasury Notes declined 5 bps to 47 bps. As the Federal Reserve continued its tightening program, the front end of the curve rose as 2-year U.S. Treasury Note yields climbed 38 bps in the period. However, yields on 10-year U.S. Treasury Notes increased only 33 bps in the period, allowing the curve to flatten but remain upward sloping. The 10-year U.S. Treasury Note yield ended the period at 2.74% and not surprisingly failed to reach the psychologically important level of 3%. As the economy continues to improve, we believe that the Federal Reserve will raise rates two more times this year.

Securitized products

Financial market volatility in the first quarter created modestly negative excess returns for the securitized products sectors relative to U.S. Treasuries. Agency MBS comprised the worst performing securitized products category, lagging U.S. Treasuries by 39 bps, while CMBS and ABS underperformed by 6 bps and 19 bps, respectively. We maintained our defensive strategy within MBS and CMBS primarily due to historically rich valuations. With improving economic growth and healthy labor markets, the fundamentals for residential housing, commercial real estate, and consumer finance remain supportive of the securitized sectors.

Investment grade credit

Investment grade credit struggled during much of the first quarter of 2018, underperforming U.S. Treasuries by 66 bps, with short maturity, financials, and AA and A rated credit experiencing the most relative credit spread widening. Valuations remain stretched and reside only 21 bps wide of the cyclical tight, but roughly 100 bps tighter than the cyclical wide. Demand technicals deteriorated recently due to a decline in retail inflows, as well as a decline in foreign demand, partially as a result of both increased currency hedging costs and favorable competing investment alternatives. Additionally, technical demand for short maturity credit plummeted due to evaporating demand from corporations repatriating overseas cash. New issue supply remains high and we expect it to increase versus 2017 because of increased M&A activity, despite the positive effects of tax repatriation. Further, we expect overall cross-asset-class supply to increase materially in the second half of 2018, due to the tapering of Federal Reserve quantitative easing. Topline fundamentals continue to improve, largely as a result of improving economic growth and favorable corporate tax reform. However, the effects of tariffs and a trade war with China, should it materialize, represent a potential earnings headwind for many industries and companies. In addition, we believe that much of any earnings benefit from lower tax rates will accrue primarily to equity holders, leaving credit metrics stretched.

High yield

Equity market volatility, rising rates, and trade war headlines posed challenges for the U.S. high yield market in the first quarter, as the Bloomberg Barclays U.S. Corporate High Yield Index returned -0.86%, its worst quarterly total return since 2015. After touching a 10-year low of 311 bps in late January, spreads ended the quarter 11 bps wider at 354 bps. CCCs outperformed during the quarter, providing a positive total return of 0.30%, while the rate back-up hurt BBs in particular (BBs and Bs returned -1.60% and -0.55%, respectively). Two of last year’s hardest hit industry sectors, wirelines and retail, outperformed in the first quarter of 2018, returning 1.00% and 0.93%, respectively. Conversely, higher-rated sectors that started with tight spreads tended to underperform, including restaurants, wireless, and banking, which returned -2.75%, -2.50% and -2.49%, respectively. Technicals remain challenged by six consecutive months of retail outflows, although new issue supply comprises mostly refinancings. Fundamentals remained a bright spot, with favorable leverage and EBITDA growth trends continuing in the fourth quarter of 2017 the latest reported period.

Leveraged loans

Leveraged loans outperformed high yield bonds for the second consecutive quarter with a return of 1.58%, as measured by the Credit Suisse Leveraged Loan Index, versus -0.86% for the HY Index. They shrugged off recent volatility thanks to strong technicals and solid performance by lower-rated tiers. Gains in the period were led by a 3.25% total return for retail, 2.72% for energy, and metals & mining with a return of 2.61%, while consumer durables returned -0.61% as the lone negative returning industry. With rates moving higher, retail loan funds are once again experiencing inflows, which combined with firm CLO demand, have created a strong technical backdrop to the market. Rising LIBOR continues to push average yields higher and, despite the recent high yield sell-off, loans still look attractive on a relative value basis.

Non-dollar

The U.S. Federal Reserve is clearly ahead of the rest of the world in its monetary policy cycle. This has made nominal U.S. interest rates more attractive globally. As a result, we currently see little value in non-U.S. bonds. Ultimately, we expect U.S. inflation to return and push long-term rates higher. In that event, non-U.S. bonds could become attractive as a defensive sector for some strategies. We expect the U.S. dollar to weaken as the country’s twin deficits (i.e., a combined budget and trade imbalance) continue to climb.

Disclaimers

This report is prepared for informational purposes only. It does not consider the specific investment objective, financial situation or particular needs of any recipient. Tortoise is not soliciting any action based on this report, and the report is not to be construed as an offer to sell or solicit investment management or any other services. The information and opinions contained herein have been compiled or arrived at based on information obtained from sources believed to be reliable and in good faith, but we do not represent that it is accurate or complete and it should not be relied upon as such. Opinions expressed are our current opinions as of the date appearing on the material only and are subject to change without notice. Index returns do not reflect the effect of management fees. No part of this publication may be copied, photocopied or duplicated in any form or by any means without Tortoise’s prior written consent.

Past performance is no guarantee of future results.

© 2018 Tortoise

Read more commentaries by Tortoise