Recent market volatility suggests that investors are questioning whether the post-crisis subpar pace of economic growth, which we dubbed The New Normal, is subsiding, to be replaced by more traditional late-cycle outcomes – in particular faster inflation and tighter monetary policy.

We believe that U.S. economic growth will likely accelerate to 2.5% or so this year, and that faster growth along with high levels of resource utilization – i.e., tight labor markets – will boost inflation and compel the Federal Reserve to implement more rate hikes than are currently priced in by the fixed income market. We would not, however, dismiss either The New Normal or The New Neutral, our term for an era of low global policy rates, just yet.

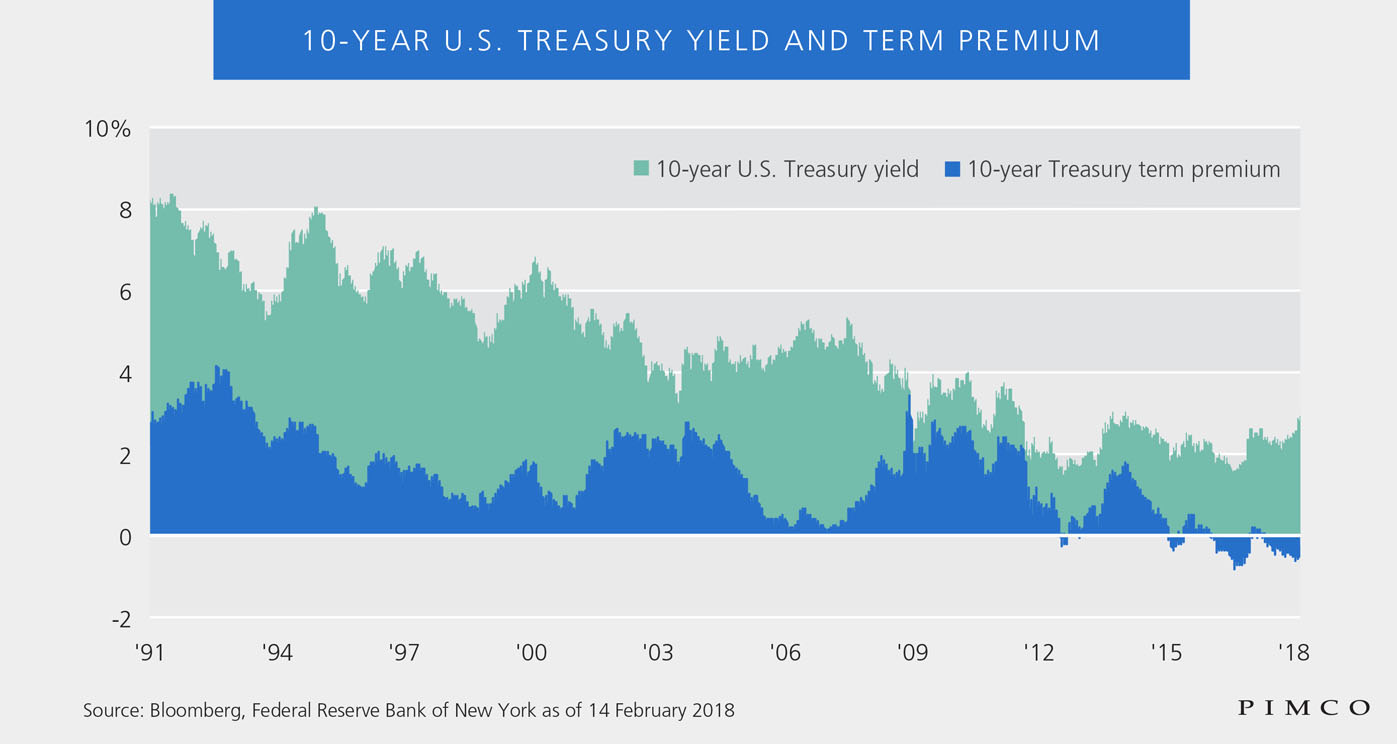

That said, we are mindful of the impact that a rising U.S. budget deficit and fading Federal Reserve support may have on market interest rates, and we believe it is an important factor to consider when constructing a fixed income portfolio. For example, we would expect investors to demand increased compensation for future risks, as reflected in term premiums for U.S. Treasuries as shown historically in Figure 1.

Nevertheless, we believe powerful forces are working against a permanent increase in the trajectory of economic growth in the U.S., including the aging population, productivity trends, sovereign indebtedness, credit growth, and an imbalance between savings and investments.

Moreover, many nations, and in particular those within the eurozone, remain several years behind the U.S. in their economic cycles, which will limit the extent to which global central banks can move away from their extraordinary monetary accommodation.

Therefore, absent a permanent increase in the trajectory of U.S. economic growth and a faster reversal of monetary accommodation abroad, market interest rates are more likely to be contained than break significantly higher.

We suggest bond investors consider the following action plan:

- Neutralize equity risk by holding core bond strategies tied to the Bloomberg Barclays U.S. Aggregate Index, which today yields about 3%. Income and unconstrained strategiess tend to be good diversifiers, too. Think more about prudent portfolio construction than about where U.S. rate increases will stop.

- Be forward-looking about equity and credit beta. Think ahead, and gear investment portfolios to handle stress. Be a liquidity provider today, not a taker – reduce risk.

- Don’t worry too much about rising rates – they have already moved a lot and likely won’t rise much more. Higher rates while potentially painful in the short-run are good for bond investors in the long run. It’s simple math. It does not necessarily need to be a reason to stop investing. Don’t try and market-time the diversification benefits of bonds. Maintaining a hedge against risk is important!

Finally, recognize that in today’s $110 trillion global bond market there are a multitude of differences among bonds and therefore many potential sources of attractive returns, many having little reliance upon the macro situation. There are also many moving parts, making this is a great time for active management.

Tony Crescenzi is a market strategist, portfolio manager and contributor to the PIMCO Blog.

DISCLOSURES

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Management risk is the risk that the investment techniques and risk analyses applied by an investment manager will not produce the desired results, and that certain policies or developments may affect the investment techniques available to the manager in connection with managing the strategy. Diversification does not ensure against loss. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

© PIMCO

© PIMCO

Read more commentaries by PIMCO