Like much of 2017, politics remained keenly in focus at the end of the year. Tax reform took center stage in the U.S., and President Trump wrapped up this major legislative victory just in time for the holidays. The sweeping tax overhaul moved quickly through both chambers of Congress after the House and Senate drafted amended versions from the separate ones each had previously passed. Notably, the final vote came on the heels of a closely watched special election for a Senate seat in the state of Alabama, which resulted in a surprise victory for the opposition Democrats and narrowed Republican control of the Senate to just two votes. In Europe, Brexit negotiations cleared a major hurdle; the UK and the European Union agreed to a preliminary deal that covered financial terms, citizenship rights and the border with Ireland, allowing negotiations to enter the next phase. Catalonia was in the headlines again: In a regional election, parties advocating for independence from Spain won a majority of seats. Elsewhere, the African National Congress (ANC), South Africa’s dominant political party, elected Cyril Ramaphosa as its new leader in a sharp rebuke to President Jacob Zuma.

Global growth momentum continued to pick up in December. Citing sound economic footing, the Federal Reserve, as expected, increased its policy rate by a quarter point – its third hike in 2017. Fed officials raised their outlook for growth in 2018, but stuck with forecasts of three rate increases in 2018 amid below-target inflation. At her final press conference as Fed Chair, Janet Yellen also highlighted the broader labor outlook, following a stronger-than-expected payrolls report in November (228,000 jobs added), and said the U.S. is “in the vicinity of full employment.” Business optimism ended the year on a high note, with global manufacturing Purchasing Managers’ Indices (PMIs) climbing to their highest level since 2011. The euro area was a particularly bright spot: The region’s survey reached a record 60.6, supported by robust expansion in new orders, output and employment. In a further sign of improvement, Portugal’s sovereign credit rating was upgraded two notches to investment grade by Fitch, marking a significant milestone in the periphery’s continuing recovery. Lastly, Japan’s manufacturing PMI increased to its highest level since 2014 as output growth quickened and accumulating backlogs spurred hiring. Still, the Bank of Japan maintained its ultra-accommodative policy in the face of stubbornly low inflation, despite growing speculation that it may raise its yield-curve target.

Higher valuations on risk assets and flatter yield curves in December reflected the prevalent trends of 2017. Front-end rates moved higher across developed market yield curves, most notably in the U.S. as the Fed raised interest rates, though long-term rates fell slightly. This flattening U.S. curve garnered more attention in December when the spread between short- and long-term yields narrowed to its tightest level since 2007. In South Africa, the rand surged by almost 11% against the U.S. dollar on rising optimism that newly elected ANC head Cyril Ramaphosa would eventually replace Jacob Zuma as president and initiate much needed reform. In risk assets, the S&P 500 ended the month higher to deliver the first full year of positive monthly returns since the inception of the total return index; emerging market stocks gained nearly 4% over the month, lifting 2017 gains to over 37%; and high yield credit spreads tightened to pre-financial-crisis levels. All of this transpired while the U.S. 10-year Treasury yield ended the month – and the year – virtually unchanged.

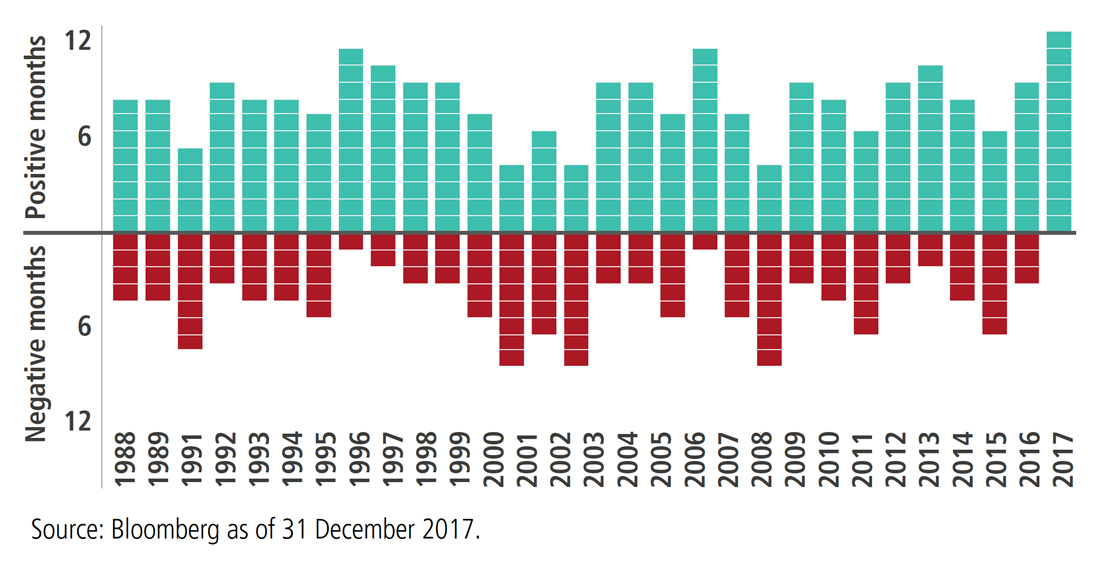

A streak like no other Spurred by the passage of U.S. tax reform, the S&P 500 rallied 1.1% in December, bringing its total return for 2017 to 21.8%. Remarkably, 2017 was the first calendar year without a single negative month since the S&P 500’s total return index incepted in 1988. What’s more, positive monthly returns actually began in November 2016, and the 14-month streak is the longest in index history. Contributing to the steady rally was a surprising lack of volatility: The CBOE’s Volatility Index (VIX) recorded 45 of its 50 lowest closes in history over 2017, including the lowest of 9.1 in November.

Market snapshot

EQUITIES

Generally strong fundamentals boosted investors’ appetite for risk, and developed market stocks1 returned 1.4%. In the U.S.,2 stocks rallied 1.1% as tax reform took center stage and Congress passed the Tax Cuts and Jobs Act. The new law takes effect in 2018 and reduces the statutory corporate tax rate from 35% to 21%, among other provisions, a boon to domestically oriented U.S. companies. European3 and Japanese4equities joined Wall Street in the rally, rising 0.8% and 0.3%, respectively.

In emerging markets,5 a bright macro picture and strong demand drove stocks to return 3.6%. In Brazil,6improving sentiment and rising industrial metal prices helped lift stocks to a 6.2% return. Stocks in India7rose 2.7% after Prime Minister Narendra Modi’s ruling Bharatiya Janata Party narrowly won a key assembly election in the state of Gujarat. Russian equities8 gained 1.1% amid higher crude oil prices. Chinese stocks,9 however, fell 0.3% as continued efforts to deleverage the economy weighed on risk assets.

DEVELOPED MARKET DEBT

Developed market yield curves continued to flatten in December as front-end rates broadly moved higher. In the U.S., the Fed hiked its policy rate for the third time in 2017, helping push two-year Treasury yields 10 bps higher. Even as highly anticipated tax legislation passed, the U.S. 10-year yield was little changed and ended the year at 2.41%. Yields in the eurozone moved higher thanks to several reports showing strengthening growth, falling unemployment and rising consumer confidence. The notable exception to rising yields was in the UK, where yields across the curve fell after more progress in Brexit negotiations; the UK 10-year rate ended the month 14 bps lower at 1.19%.

INFLATION-LINKED DEBT

Global inflation-linked bonds (ILBs) gained and outperformed comparable nominal bonds across the major markets in December. In the U.S., real yields moved lower; this reversed the yield curve flattening trend of the previous two months even as the trend continued for nominal bonds and the Federal Reserve raised rates. Breakeven inflation rates (BEI) rose on the back of surging oil prices, despite a disappointing November inflation report. In the UK, index-linked gilts gained as the Bank of England left monetary policy unchanged and unveiled plans to allow EU banks to operate under existing rules after Brexit. UK breakeven inflation rates ended the month flat, paring early losses from a weak Retail Price Index reading. In Japan, inflation-linked bonds edged higher after a strong Consumer Price Index report.

CREDIT

Global investment grade credit10 spreads tightened three basis points (bps) in December, due in part to lighter-than-expected issuance and a positive reaction to the final U.S. tax reform bill. The sector outperformed like-duration global government bonds by 0.29% during the month; positive returns continued to be driven by low volatility, broadly supportive fundamentals and a strong technical backdrop.

Following a difficult month in November, global high yield bonds11 posted a modest, but positive, return to finish the year up 0.26% in December. Income carried the weight as prices were slightly lower. Spreads widened slightly as investors digested the passage of the U.S. tax bill, the Fed’s rate hike, multi-year highs in oil prices and a typical seasonal slowdown in activity.

EMERGING MARKET DEBT

Emerging market (EM) debt ended a strong year on a high note, with both external and local debt posting positive returns in December. Local debt performance was driven by a move lower in index yields and by the appreciation of EM currencies versus the U.S. dollar, while external debt performance was driven largely by yield, with spreads tightening modestly. South African risk assets notably outperformed in local and external markets, as market participants responded positively to Cyril Ramaphosa’s election as president of the African National Congress. Mexican assets lagged external and local benchmarks as allegations of corruption against PRI (Partido Revolucionario Institucional) officials appeared to hinder the ruling party’s chances of defeating populist candidate Andrés Manuel López Obrador in Mexico’s upcoming presidential elections.

MORTGAGE-BACKED SECURITIES

Agency MBS12 returned 0.33% and outperformed like-duration Treasuries by 16 bps. Low interest-rate volatility and slow prepayment speeds continued to support the sector, but the flattening of the yield curve weighed on 15-year MBS, which underperformed 30-year MBS. Additionally, the markets reacted negatively to Ginnie Mae’s plan to contain prepayments on certain VA (Veterans Affairs) loans, causing Ginnie Mae MBS to materially underperform conventional MBS. Gross MBS issuance decreased 9% in December, while prepayment speeds fell 10%. Non-agency residential MBS spreads were generally unchanged, while non-agency commercial MBS13 returned 0.28% and outperformed like-duration Treasuries by 20 bps.

MUNICIPAL BONDS

Municipals posted positive returns in December and outperformed U.S. Treasuries. The Bloomberg Barclays Municipal Bond Index returned 1.05% during the month, bringing 2017 returns to 5.45%. Long and intermediate maturities outperformed the front end as the yield curve continued to flatten. Municipal bond mutual fund demand was mixed in December, but inflows ended 2017 modestly positive at $11.3 billion. The comprehensive tax reform bill passed by Congress in December and due to take effect in 2018 led to a spike in supply: A record $64 billion in muni bonds were brought to market, beating the previous record of $55 billion set in December 1985.

CURRENCIES

Tax reform provided a modest tailwind to the U.S. dollar in December, but weaker-than-expected core inflation and average hourly earnings data eroded the dollar’s gains over the month. The soft finish to the year left the dollar weaker against every other G10 currency in 2017. The weakening U.S. dollar and higher metals prices helped lift the Australian and New Zealand dollars, reversing their recent declines. Despite the quickening pace of Brexit negotiations, the British pound ended the month almost flat while the euro capped off a strong year with another solid month against the backdrop of dollar weakness.

COMMODITIES

December was a positive month for commodities, with energy and metals driving most of the gains. Rising geopolitical risk in Iran and Nigeria and pipeline outages in the North Sea and Libya supported crude oil prices. In addition, larger-than-expected drawdowns in U.S. inventories and new lows in OPEC output created positive sentiment. In contrast, natural gas prices fell for most of the month, despite the cold snap that hit the U.S. at year-end. Sector returns in agriculture were negative: Losses in soybeans, corn and wheat, which continued to face pressure from high inventories, overwhelmed gains in cotton and sugar. Within metals, industrials were broadly higher, supported by upbeat reports of industrial activity in China. In precious metals, gold gained as the dollar weakened and real yields fell.

Outlook

Based on PIMCO’s cyclical outlook from December 2017.

PIMCO expects world GDP growth to remain above trend at 3.0%‒3.5% in 2018, in a “Goldilocks” environment of synchronized global growth and low but gently rising inflation. Easier financial conditions, reflecting buoyant risk assets and low interest rates, and fiscal stimulus in several advanced economies imply near-term tailwinds. However, 2017–2018 could mark the peak for economic growth in this cycle, and with many markets already reflecting an optimistic outlook, we see risks ahead: U.S. fiscal stimulus late in the cycle leaves less room for stimulus in the next recession; inflation may well overshoot expectations in 2018 due to fiscal stimulus, rises in commodity prices and easy financial conditions; and the reduction of accommodative monetary policy by global central banks could pressure economies and asset markets, which have become accustomed to low interest rates.

In the U.S., we look for above-consensus growth of 2.25%–2.75% in 2018. Tax cuts and higher federal spending ‒ due to hurricane-related disaster relief and a likely rise in discretionary spending limits under an expected government funding compromise – should boost growth. With unemployment likely to drop below 4%, we expect some upward pressure on wages and consumer prices, and core inflation to rise above 2% over the course of 2018. Under new leadership, the Federal Reserve is expected to continue tightening gradually; our baseline forecast calls for three rate hikes this year.

For the eurozone, we expect growth will be in a range of 2.0%‒2.5% this year, significantly above trend. The expansion is now broad-based across the region, with growth momentum strong and financial conditions favorable. Core inflation, though, is expected to remain very low, creeping only marginally above 1% this year due to low wage pressures and the appreciation of the euro in 2017. We expect the European Central Bank to end its bond purchases in September, but we do not foresee a rate increase until mid-2019.

In the UK, we expect above-consensus growth in the range of 1.25%–1.75% in 2018. Our base case is that a deal for a transitional arrangement will be struck in the first half of this year, smoothing the UK’s separation from the European Union, and that growth will reaccelerate in the second half as business confidence and investment pick up. Inflation should fall back to the 2% target by year-end, with the effect of sterling’s depreciation in 2017 fading. The Bank of England will likely follow a very gradual path higher; we expect one to two hikes in 2018.

Japan’s GDP growth is expected to remain firm at 1.0%–1.5% in 2018, with risks tilted to the upside. Fiscal policy should remain supportive ahead of the planned value-added tax hike in 2019. With unemployment below 3% and job growth accelerating, we think inflation will move up gradually toward 1% over the year, but the 2% inflation target is likely to remain out of reach. We expect the Bank of Japan to aim to slow its balance sheet expansion and/or tweak its yield curve control policy so that the yield curve steepens this year.

In China, we expect a controlled deceleration in growth to 5.75%–6.75% this year. The authorities’ focus is likely to be on controlling financial excesses, particularly in the shadow banking system, and on some fiscal consolidation, chiefly by local governments. We expect inflation to accelerate to 2.5% on stronger core inflation and higher oil prices, inducing the People’s Bank of China to tighten policy by raising official interest rates, versus the consensus expectation of no hikes. We are broadly neutral on the yuan and expect exchange rate volatility to remain low.

In Brazil, Russia, India and Mexico, we expect growth to collectively rise to 4% in 2018, slightly above consensus, with modest upside risk from recoveries in Brazil and Russia. Emerging markets are catching up to the recovery in developed markets, with improving fundamentals and greater differentiation among countries. This recovery is likely to be shallower and slower than others, however; EM potential growth has fallen, and key political events are likely to keep investors cautious. We expect inflation to stabilize around 4.1%, also above consensus as most of the decline in EM inflation thus far appears cyclical rather than structural.

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk and liquidity risk. The value of most bonds and bond strategies is impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax; a strategy concentrating in a single or limited number of states is subject to greater risk of adverse economic conditions and regulatory changes. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation- Protected Securities (TIPS) are ILBs issued by the U.S. government. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. REITs are subject to risk, such as poor performance by the manager, adverse changes to tax laws or failure to qualify for tax-free pass-through of income. It is not possible to invest directly in an unmanaged index.

PIMCO does not provide legal or tax advice. Please consult your tax and/or legal counsel for specific tax or legal questions and concerns. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Any tax statements contained herein are not intended or written to be used, and cannot be relied upon or used for the purpose of avoiding penalties imposed by the Internal Revenue Service or state and local tax authorities. Individuals should consult their own legal and tax counsel as to matters discussed herein and before entering into any estate planning, trust, investment, retirement, or insurance arrangement.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.