In the world

The convoy of developed world central banks reducing accommodation appeared to gather steam. The Fed confirmed its plans to begin unwinding its balance sheet in October by very gradually reducing reinvestments of U.S. Treasuries and mortgage-backed securities from maturing securities and paydowns; all but four of the 12 Federal Open Markets Committee (FOMC) members also forecast one more rate hike before the end of 2017. The widely followed “dot plot” projections from the committee were more hawkish than anticipated in light of the tepid outlook for inflation. The Bank of Canada continued on its path of policy normalization with its second rate hike of the year in response to broadening growth. Across the Atlantic, the Bank of England surprised with hawkish rhetoric, saying that a rate increase was “likely to be appropriate over the coming months.” Meanwhile, ECB policymakers raised their growth forecasts to the highest levels since 2007, and President Mario Draghi indicated that a decision about tapering its quantitative easing (QE) program in the eurozone would likely be made in October.

Global political developments continued to capture headlines. Following the detonation of another bomb by North Korea, the U.N. adopted tougher sanctions, and tensions escalated as the U.S. sent warplanes to the edge of the country’s airspace. As President Trump dealt with the growing threat from North Korea, more natural disasters struck North America: On the heels of Hurricane Harvey, Irma and Maria wreaked havoc in the Caribbean and Puerto Rico, and earthquakes took a toll on Mexico. Tied to relief funds for states affected by Harvey, a deal struck by President Trump with congressional Democrats raised the debt ceiling and funded the government until December. On the policy front, several key Republican senators – dubbed the “Big Six” – unveiled their long-awaited tax proposal, which sought to simplify the bracket system and lower the corporate tax rate. Elsewhere, elections and referendums drew attention: German Chancellor Angela Merkel’s party saw its lowest share of the vote since 1949 as the populist AfD party secured surprising gains; tensions heightened ahead of Catalonia’s independence referendum (declared illegal by the Spanish government); and Japanese Prime Minister Shinzo Abe dissolved Parliament and called a snap election in October following a recent recovery in public support. Lastly, S&P downgraded its long-term sovereign credit rating for China, citing rising economic risks stemming from unsustainable credit growth.

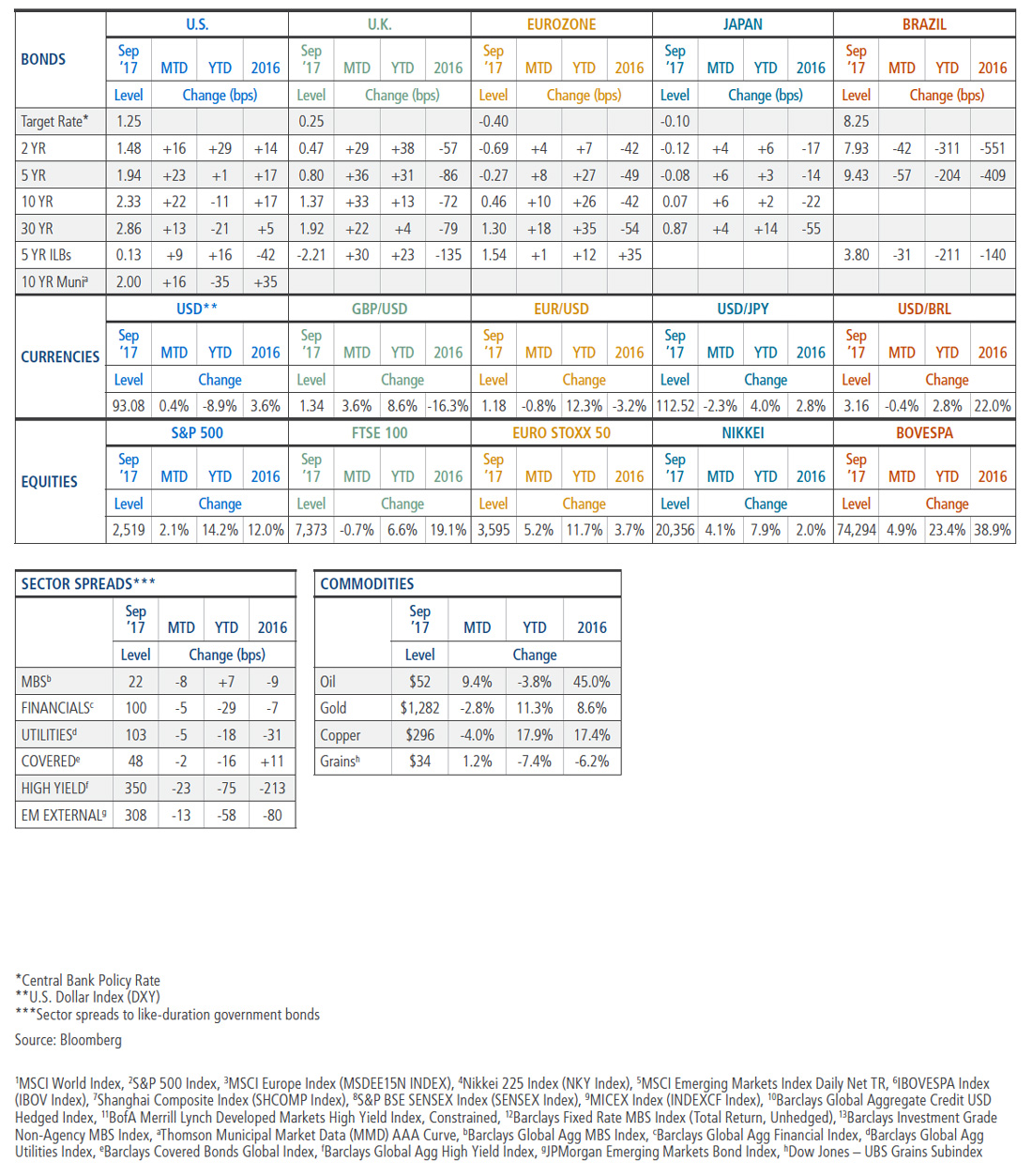

Interest rates moved higher on the hawkish tilt in central bank rhetoric while equities gained on generally positive economic data. Yields jumped the most in the U.K. after the Bank of England signaled a rate increase in coming months, with its benchmark 10-year rate increasing 33 basis points (bps). The rise in Canada’s 10-year yield was not far behind at 25 bps after the central bank hiked rates for the second time this year. Along similar lines, the hawkish perception of the Fed’s statement after its September meeting contributed to yields moving higher in the U.S. Expectations of another rate hike in December increased, but investors appeared to shrug off the Fed’s announcement that it would begin unwinding its balance sheet in October, as the well-telegraphed plan was largely in line with expectations. In addition, the fresh tax plan from Congressional Republicans, which included a proposal to cut corporate taxes from 35% to 20%, boosted equities late in the month and strengthened the U.S. dollar. Despite the political headlines in Germany and Spain, equities also marched higher in Europe in response to solid economic data and an upgrade to the ECB’s 2017 growth forecast for the region.

Smoke Signals

While the Bank of England (BoE) held the policy rate steady at 0.25% at its September Monetary Policy Committee (MPC) meeting, a majority of members signaled a desire to tighten policy ”in the coming months.” The hint of a sooner-than-expected rate rise caused U.K. interest rates to spike and the British pound to strengthen. The shift in rhetoric has been attributed to inflation, which remains above the central bank’s 2% target: Prices rose 2.9% in August from the prior year, and the BoE expects an increase to 3% by October. Barring a significant deterioration in economic data, investors now widely expect the BoE to raise rates at its November meeting.

In the markets

The Resurgent Right

Germany bucked the trend of receding populist movements throughout Europe, as its far-right AfD party won a better-than-expected 12% of the vote in September’s federal elections. Despite never having previously held seats in the legislature, the AfD became the body’s third-most powerful party, taking 94 seats. Riding a wave of anti-immigrant sentiment, the far-right party’s populist rhetoric seemed to resonate across former industrial regions that have faced higher levels of unemployment in recent years. While Angela Merkel won a fourth (and final) term as chancellor, her party’s weakest showing since 1949 means tough negotiations to form a governing coalition must now follow.

EQUITIES

Developed market stocks1 returned 2.2% despite escalating tension between the U.S. and North Korea and a hawkish shift in tone from major central banks. In fact, U.S. equities2 surged to all-time highs, returning 2.1% and capping their longest monthly winning streak since 1959. The “reflation trade”– buying equities in anticipation of pro-growth policies – showed signs of life in the lead-up to the Republicans’ tax reform plan released at the end of the month. European stocks3 returned 3.9%, posting their strongest month of 2017, underpinned by generally solid fundamentals. In Japan,4 equities returned 4.2% and also delivered their best month of the year on improving growth, positive sentiment and a weaker yen.

In emerging markets,5 stocks fell 0.4% despite relatively stable global market conditions and a strong technical backdrop. In Brazil,6 stocks rallied 4.9% on optimism that embroiled President Michel Temer could still pass growth-oriented reforms. China’s sovereign credit rating was downgraded by Standard & Poor’s, and its equities7 fell 0.3%. Indian stocks8 fell 1.3% as rising tension with North Korea weighed on markets. Higher oil prices helped Russian stocks9 notch their fourth consecutive month of gains to return 3.0%.

DEVELOPED MARKET DEBT

Even as geopolitical tensions built and political turmoil continued in the U.S., interest rates in developed regions generally moved higher, mainly because global central banks shifted toward less accommodative policy stances. The shift higher was led by the U.K., where the 10-year rate rose 33 basis points (bps) and the Bank of England (BoE) suggested that tightening would likely occur in the coming months. The Bank of Canada raised its policy rate for the second time this year, which contributed to 10-year yields rising 25 bps to 2.10%. The perception of a hawkish leaning at the September Federal Reserve meeting helped push U.S. 10-year yields up 22 bps to end the month at 2.33%. In addition, German 10-year rates rose 10 bps.

INFLATION-LINKED DEBT

Global inflation-linked bonds (ILBs) declined across major markets but generally outperformed comparable nominal bonds as a sharp rise in crude oil prices boosted inflation expectations. In the U.S., Treasury Inflation-Protected Securities (TIPS) posted losses amid a sharp rise in rates as the Fed unveiled its plans to reduce its balance sheet and reiterated the likelihood of another rate hike this year. Breakeven inflation (BEI) rates were supported by the jump in crude oil futures and a stronger-than-expected Consumer Price Index (CPI), which

broke a string of five consecutive downside surprises. U.K. index-linked gilts also fell sharply for the month in tandem with nominal gilts based on the relatively hawkish tone from the Bank of England’s meeting minutes. U.K. inflation expectations moved higher, due in part to an upside surprise in the Retail Price Index (RPI), which posted its highest annual rate since early 2012.

CREDIT

Global investment grade credit spreads10 tightened 6 bps, outperforming like-duration global government bonds by 0.6% in September. The long-awaited proposal for corporate tax reform, as well as slower new U.S. issuance compared to the heavy supply in August, helped spreads tighten during the month. Strong global investor demand for high quality income also continued to support U.S. credit overall.

Global high yield bonds11 shrugged off a sharp increase in government rates through September and instead took their cue from the strong returns in stocks and a six-month high for oil prices. The momentum resulted in the sixth consecutive month of positive returns for the asset class, which was up 0.9% for the month and 7.2% year-to-date. With Treasury bond rates higher and speculative grade yields lower, spreads declined by about 30 bps.

EMERGING MARKET DEBT

Local and external emerging market debt went their separate ways in September. Local currency debt posted negative returns on the month as EM index yields followed developed market yields higher on the hawkish turns by several global central banks. EM currencies were also weaker, as higher-than-expected inflation in the U.S. prompted the dollar to strengthen. Brazilian local rates were a notable outperformer, with inflation slowing to its lowest point since 2015. External sovereign debt finished the month flat because spread tightening was offset by the move higher in underlying U.S. Treasury yields, although lower-duration external corporate bonds posted positive returns with similar levels of spread tightening.

MORTGAGE-BACKED SECURITIES

Agency MBS12 returned -0.22% and outperformed like-duration Treasuries by 35 bps. As widely anticipated, the Fed announced it will begin reducing the size of its balance sheet in October. As interest rates increased and refinancing concerns abated, higher coupons outperformed lower coupons, and 30-year MBS outperformed 15-year MBS. Ginnie Mae MBS also outperformed conventional MBS, aided by Senator Elizabeth Warren’s letter to Ginnie Mae and the agency’s ongoing efforts to crack down on aggressive marketing of mortgage refinancing to veterans. Gross MBS issuance declined 4.7% from August, while prepayment speeds increased 10%. Non-agency MBS prices generally rose and spreads relative to swap rates tightened amid continued strength in the U.S. housing market. Non-agency commercial MBS13 returned -0.94% and underperformed like-duration Treasuries by 6 bps.

MUNICIPAL BONDS

Municipals posted negative returns in September: The Bloomberg Barclays Municipal Bond Index returned -0.51%, bringing year-to-date returns to 4.66%. Muni rates moved higher with Treasury yields across the curve, coming under pressure from the Fed’s formal announcement about reducing its balance sheet and more hawkish outlook than markets had anticipated. However, there were also positive developments: Municipal mutual fund demand remained strong, with $1 billion in inflows during the month, bringing year-to-date inflows to $10 billion. In addition, the long-awaited Republican tax reform proposal was in line with market expectations. The release also removed some uncertainties, although the final version of the tax plan will likely be considerably different from the proposal. Puerto Rico securities fell; the impact of two recent hurricanes was expected to extend the island’s bankruptcy process and reduce available funds to creditors.

CURRENCIES

After geopolitical tensions pushed the U.S. dollar to its weakest level since early 2015, the currency reversed course and rose nearly 3% off the low by the end of the month. This appreciation was driven in part by increased market expectations of a Fed rate hike in December as well as proposed tax reform in the U.S. Elsewhere in the G10, the British pound rose as the BoE shifted to a hawkish tone and negotiations between the European Union (EU) and U.K. somewhat reduced the probability of a hard Brexit. North Korean missile activity paradoxically drove safe-haven investors into the Japanese yen at the beginning of the month, but the Fed’s statement, coupled with Prime Minister Shinzo Abe’s decision to call a snap election, resulted in a reversal of those gains.

COMMODITIES

Commodity sectors posted mixed returns. The petroleum complex gained as investors continued to price in a realization that supplies are tightening. Crude oil prices rallied on the back of stronger demand forecasts and talk that OPEC could extend its production deal. In contrast, natural gas dipped on higher inventories. In grains, wheat was supported by both market technicals and lower stock forecasts from the USDA, and soybeans gained on the back of strong export demand. Sugar fell into negative territory as the EU completed the termination of its 50-year sugar quota, increasing the potential for production in the region. Industrial metals were broadly down for the month: Nickel prices pulled back substantially after an August rally. Gold also posted losses when the Fed nodded to the possibility of a third rate hike this year, which pushed U.S. real yields higher.

Outlook

Based on PIMCO’s cyclical outlook from September 2017.

PIMCO expects world GDP growth in 2018 to remain steady at 2.75%–3.25%, unchanged from 2017. Overall, we see a low near-term risk of recession, a moderate pickup in underlying inflation in the advanced economies, mildly supportive fiscal policies and only a gradual removal of accommodative central bank policy. However, we do see risks that could upset the calm: the aging U.S. expansion, the coming end of central bank balance sheet expansion and China’s course following its 19th National Communist Party Congress in October.

In the U.S., we see growth below consensus at 1.75%–2.25% in 2018, albeit still above trend, as the U.S. expansion matures and slack in the labor market keeps eroding. The disappearing slack should make it difficult to sustain the current pace of job and output growth, and we also don’t expect a significant acceleration of productivity growth. We forecast core inflation to increase to 2% over the course of 2018, with some upward pressure on wages. The Fed will likely continue along its trajectory of gradual tightening with two or three rate hikes between now and the end of 2018.

For the eurozone, we expect growth will be in a range of 1.75%‒2.25% in 2018, significantly above trend. A key risk for the outlook is the Italian elections in the first half of 2018, although the political risk looks more contained than earlier this year, as the euroskeptical parties have toned down their rhetoric. We think core inflation will make only moderate progress toward the European Central Bank’s (ECB) target of “below but close to 2%” and forecast inflation in a range of 1.0%–1.5% for 2018. The ECB is likely to gradually taper its bond purchases over 2018 and keep policy rates at record lows until well into 2019.

In the U.K., we expect growth to be in the range of 1.25%–1.75% for the balance of 2017 and into early 2018. Our base case is that a transitional arrangement will smooth the U.K.’s separation from the European Union and that growth will reaccelerate as business confidence picks up. We see inflation returning to the 2% target by the end of 2018, earlier than consensus and the Bank of England (BoE) expect. Our forecast calls for the BoE to start raising interest rates in 2018, with one or two hikes, although there is a risk of a hike in 2017.

Japan’s GDP growth is expected to moderate somewhat to 0.75%–1.25% in 2018 but remain above trend, reflecting ongoing fiscal and monetary support as well as decent global growth. We think inflation will creep up toward 1% over the next year as wage growth accelerates, but the 2% inflation target is likely to remain out of reach. A key swing factor will be the political future of Prime Minister Shinzo Abe and the succession of BOJ governor Haruhiko Kuroda. We expect the Bank of Japan (BOJ) to nudge its yield target for 10-year Japanese government bonds 20 to 30 basis points higher from the current 0% in the second half of 2018.

In China, we expect growth to decelerate in 2018 from the current 6.6% pace. Our wide forecast range of 5.5%–6.5% reflects uncertainty about the leadership’s prospective stance on financial stability, deleveraging and economic growth following the Party Congress. If the leadership continues to focus on suppressing volatility, growth could hold up at higher levels, but if policy pivots, the changes could weigh heavily on growth and lead to greater tolerance for a depreciating Chinese yuan.

In the emerging markets (EM) of Brazil, Russia, India and Mexico, we expect growth to rise to 4% in 2018, slightly above consensus, as recoveries in Brazil and Russia become more entrenched. Overall, most emerging economies are at a different stage of the economic cycle than developed economies and should still benefit from relatively easy global policy conditions. We expect continued disinflation, with headline CPIs falling to around 4.2% in 2018.

In sight

Now Hiring: Fed Governors

On 6 September, Stanley Fischer unexpectedly announced his retirement as Vice Chairman of the U.S. Federal Reserve. His departure leaves just three seats filled on the Fed’s seven-member Board of Governors, all of whom are voting members of the Federal Open Markets Committee (FOMC). The five remaining voting members are presidents of regional reserve banks, including New York (a permanent member) and four others who serve one-year terms on a rotating basis. The unusually high number of Board vacancies (the highest in history), combined with Chair Yellen’s four-year term expiring in 2018, leaves the future composition and direction of the Fed uncertain.

While not official, the Trump administration appeared to narrow its list of candidates for the next Fed Chair to five individuals: current Chair Janet Yellen; Director of the National Economic Council Gary Cohn; former Fed Governor Kevin Warsh; current Fed Governor Jerome Powell; and Stanford economist John Taylor. The president’s upcoming appointment will be closely watched, as the next chair’s approach to monetary policy will have vast implications for the path of policy rates and the broader economy.

Appendix

© PIMCO

Read more commentaries by PIMCO