THE DEFAULT-RECOVERY RELATIONSHIP

The well-documented inverse correlation between the default rate and the recovery rate amplifies the importance of changes in the default statistics. Simply put, a higher default rate assumption translates into both a higher probability of default and a lower recovery rate, which leads to a higher loss given default and, presumably, a higher required credit spread for a particular credit and category of credits.

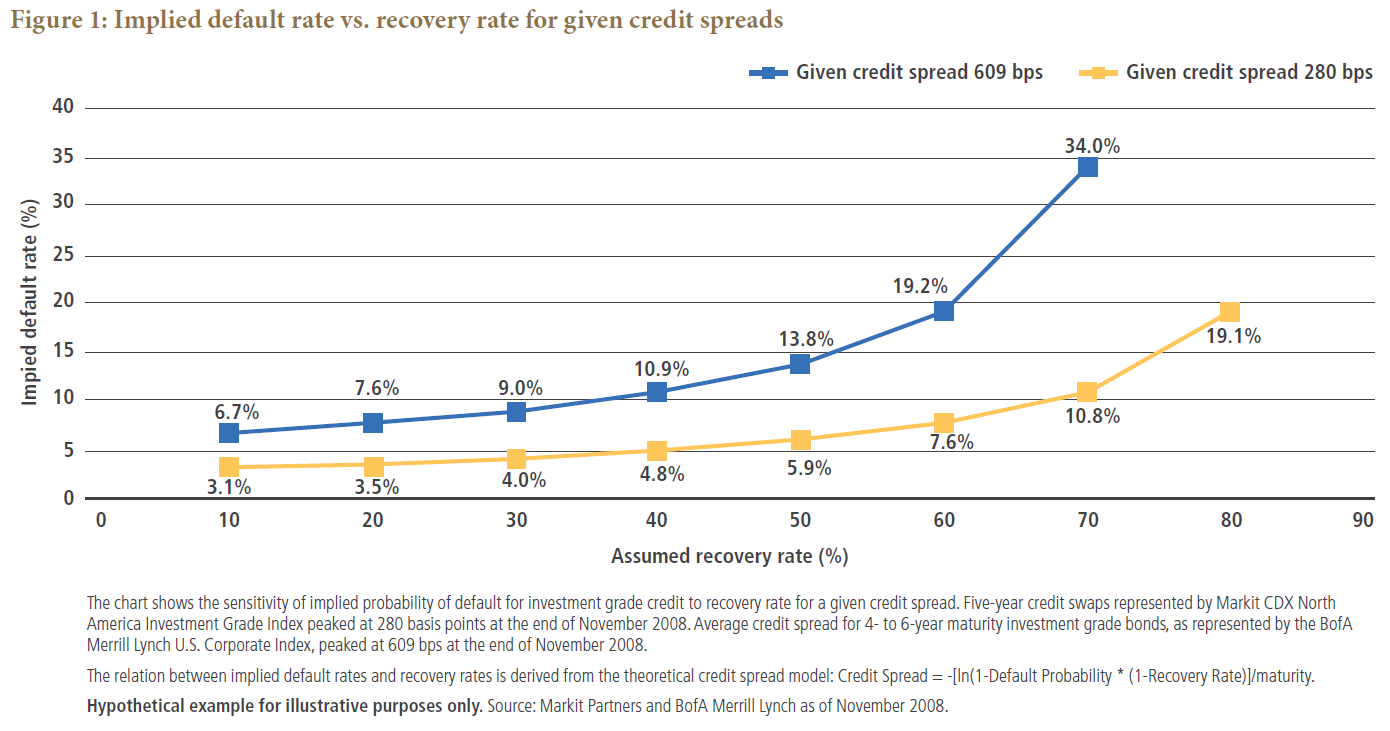

In Figure 1, we illustrate the mathematical relation of the default rate and the recovery rate given a credit spread. We use the peak 2008 spread of 280 basis points for five-year credit default swaps represented by the Markit CDX North America Investment Grade Index and 609 basis points for the cash market represented by the BofA Merrill Lynch U.S. Corporate Index and impute the implied default rates with different recovery rate assumptions, assuming no liquidity premium. (We would expect the liquidity premium to be high when default rates are high and when recovery rates are low).

DECONSTRUCTING CREDIT SPREADS

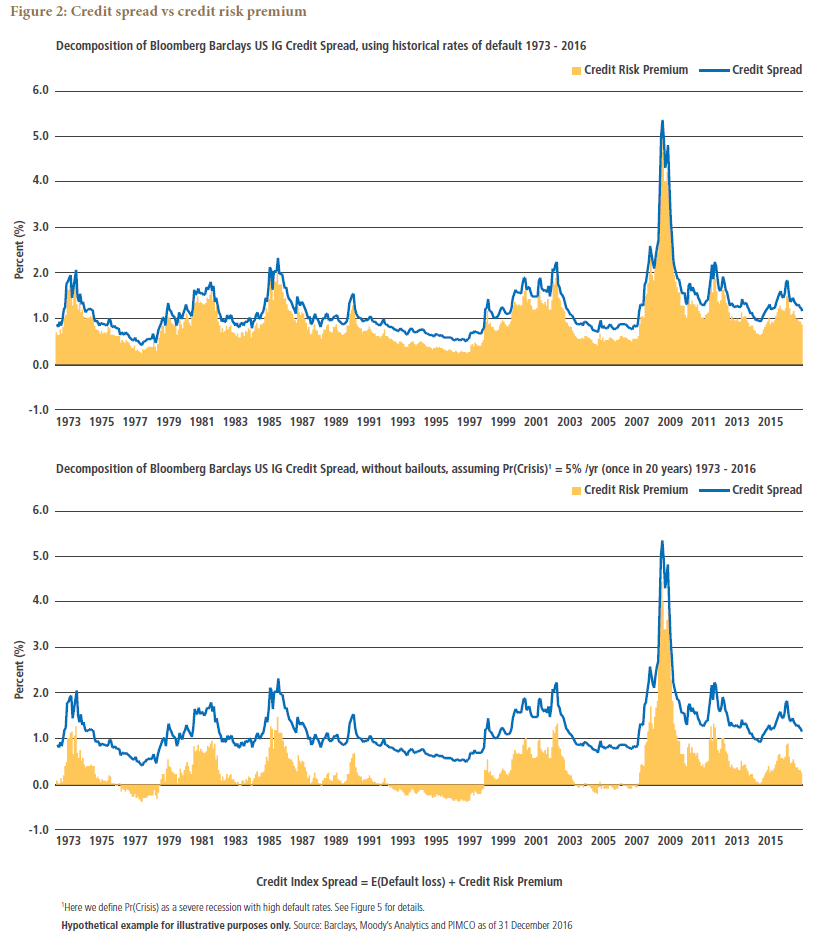

A considerable body of research exists dissecting market credit spreads. The research almost universally concludes that investors are consistently overcompensated for default risk given the default statistics. The models observe yields on corporate bonds and subtract the presumed “default-free” matched maturity Treasury yield, resulting in a credit yield spread. The spread is then compared to the probabilistic calculated spread (as shown in Figure 1). The observed credit spread varies over time and is almost always greater than the calculated spread. As shown in Figure 2, most of the researchers attribute the excess spread to a time/state varying liquidity premium. However, we will see that PIMCO default-adjusted bankruptcy statistics meaningfully change the “yield premium” conclusion.

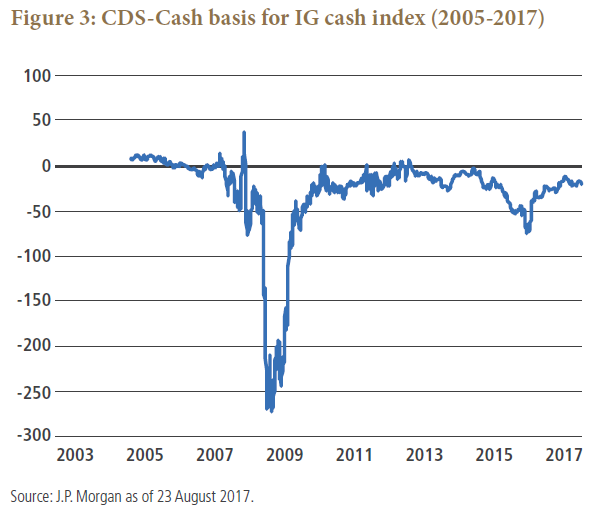

A historical time series of the CDS/cash index basis is shown in Figure 3. Setting aside differences between composition of indexes and margin requirements, spreads between the cash index and the derivative CDS contract should be close to zero in well-functioning liquid markets. (There is a slight clientele effect biasing the results to a more positive basis because there are more investors in the cash bond market than in the derivatives market.) A negative basis is indicative of a less liquid market. It represents a market within which the less liquid cash bond is valued at a discount to its derivative counterpart.

At PIMCO, we examine the market for options on equities to bring volatility measures – including equity volatility skew – into the spread analysis. The result, in our view, is a substantially more accurate analysis of spread attribution and a residual spread that we label a liquidity premium. In other similar research, Benzschawel and Assing postulate that the credit spread is compensation for default plus credit spread volatility. They say, “Credit spreads, on average, are linear functions of spread volatility on logarithmic axes.” They refer to the credit spread volatility compensation as “credit risk premium.” In any case, we can clearly understand the importance of the default statistics to credit market research and to real money investing.

FLAWED STATISTICS

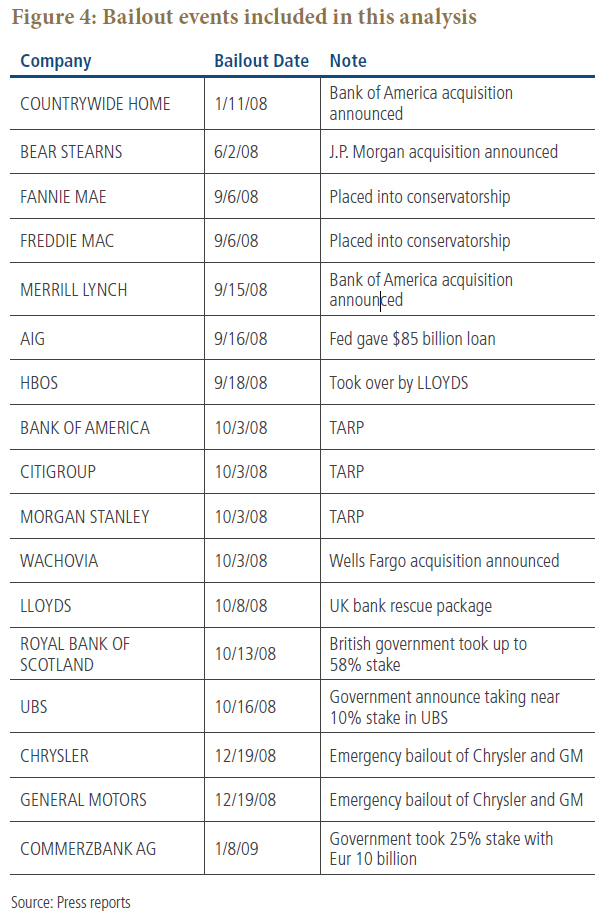

We believe the published default statistics tend to be misleading and understate the risk associated with credit investments. Our belief incorporates the extent of government involvement in the credit market. Government bailouts of private companies have occurred occasionally, including Penn Central Railroad (1970), Lockheed (1971), Franklin National Bank (1974), New York City (1975) and Chrysler (1980). However, these earlier government bailouts were never as great as those in 2008: Figure 4 shows companies that received direct government support, including Fannie Mae and Freddie Mac. Absent such support, all of the companies listed were likely bankrupt, and such bankruptcies likely would have resulted in many more corporate (and possibly municipal) bankruptcies and a substantially lower recovery rate on the assets of the affected companies.

Regarding Fannie Mae, it’s worth noting these words in its bond debenture prospectus: “The Debt Securities, together with the interest thereon, are not guaranteed by the United States and do not constitute a debt or obligation of the United States or of any agency or instrumentality thereof other than Fannie Mae.” Yet, with a stroke of the pen, all Fannie Mae and Freddie Mac debt became an obligation of the U.S. government.

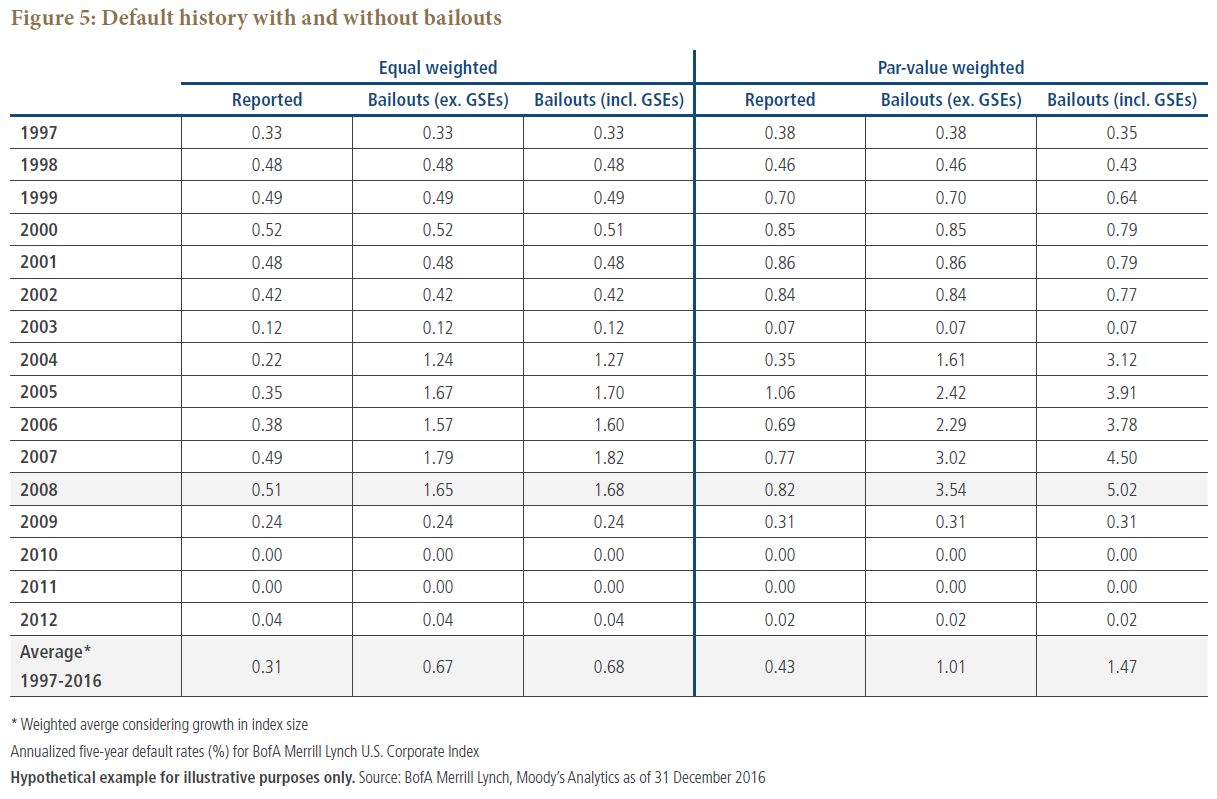

In our analysis, we have adjusted the reported default statistics to include these “bankrupt” entities. It is not possible to calculate the corresponding recovery rate. However, we believe recovery rates would be much lower than reported, and our adjustments are a more realistic indicator of embedded default risk in a capitalistic economy. In Figure 5 we see that during the five years beginning in 2008 the par value weighted annualized five-year default rate, including Fannie Mae and Freddie Mac, increases sixfold from 0.82% to 5.0%. This is clearly a most substantial modification. Even if we exclude the two mortgage companies, the default rate increases by four times (to 3.5% per year). The average annualized five-year default rate for the 1997-2016 period increases by more than three times, from 0.4% to 1.5%. The importance of the difference cannot be overstated, and the implications for investment analysis and decision making are profound. Again, these revised statistics should be considered optimistic because they are void of second- and third-round bankruptcies that almost certainly would have resulted, biasing the default rate much higher and the recovery rate much lower.

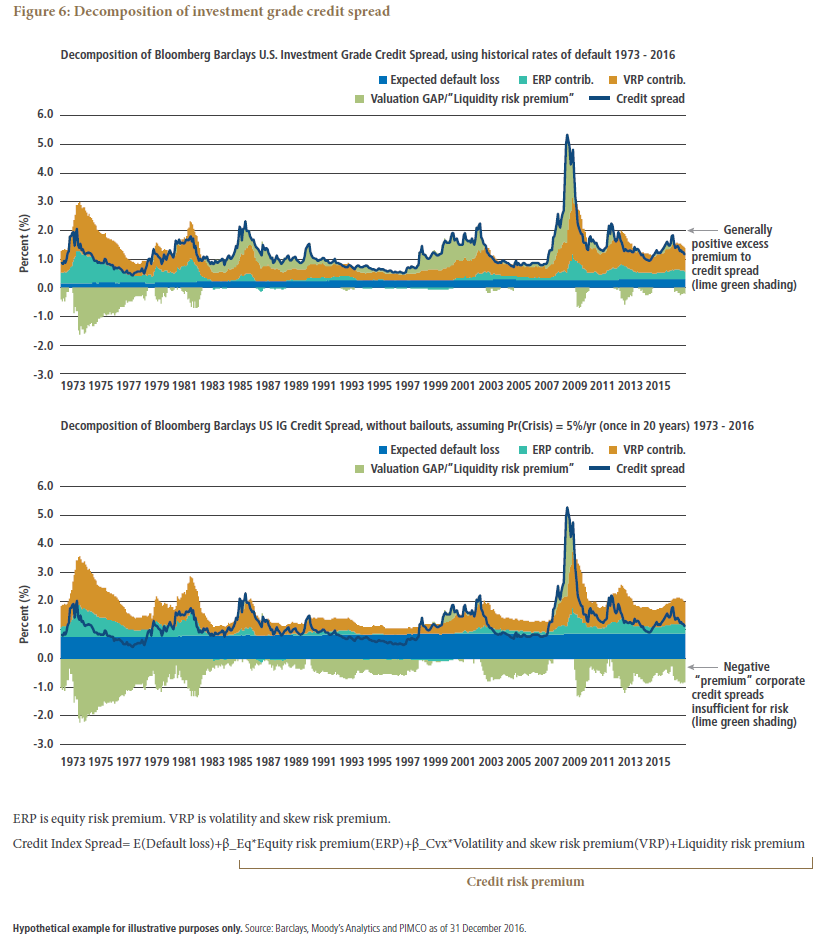

We then recalculate the post 2008 “liquidity premium” using the revised, understated, yet more accurate default statistics (see Figure 6). We observe the variability of the contribution of the risk components through time. We see the “cheapness” of credit (as denoted by lime green shading above the “0” line) when reported default data is used and the overvaluation of credit (lime green shading below the “0” line) when our bankruptcy-adjusted data is used. Using our revised default data, we demonstrate – contrary to most other research on credit spreads – that investors have not been, and are not being, adequately compensated for expected loss of principal – if government support is withdrawn from calculations. While this is a hypothetical exercise, our long-term outlook recognizes the likelihood that central bank intervention will wane over the next few years, and it is also plausible that voters have less appetite for bailouts.

Our conclusion is consistent with Sharpe Ratio data for the period January 1973 – July 2017. Sharpe Ratios for U.S. IG credit spreads (represented by the Bloomberg Barclays U.S. Investment Grade Index), U.S. equities (represented by the S&P 500 Index) and the U.S. 10-year Treasury note were 0.16, 0.35 and 0.27, respectively, indicating poor compensation relative to the volatility of return for corporate bonds even with the bailouts.

We apply the revised statistics to the leverage of hedge funds and to the insurance industry as examples of the implications of the revised data on leveraged credit risk. Our adjusted default statistics imply at least a one notch rating decline to all ratings categories. Although this is our internal analysis, if our findings were applied broadly, we believe they would result in substantial changes in the financial services industry. Our findings, for example, suggest roughly 40% greater capital requirements may be required for credit hedge funds (based on increased collateral haircuts). For the insurance industry, the hypothetical credit rating changes imply a need for a de-risking of credit given current industry capitalization. Our analysis also suggests the risk associated with credit in investors’ portfolios is substantially greater than currently perceived and, as a result, the systemic risk to the macro economy is also greater than perceived.

We have long believed that prudent credit investing does not simply rely on the ratings provided by agencies – we carefully scrutinize bonds on a case-by-case basis. Certainly now is a good time for a reminder of this best practice, since there is substantial uncertainty about policy shifts on the horizon.

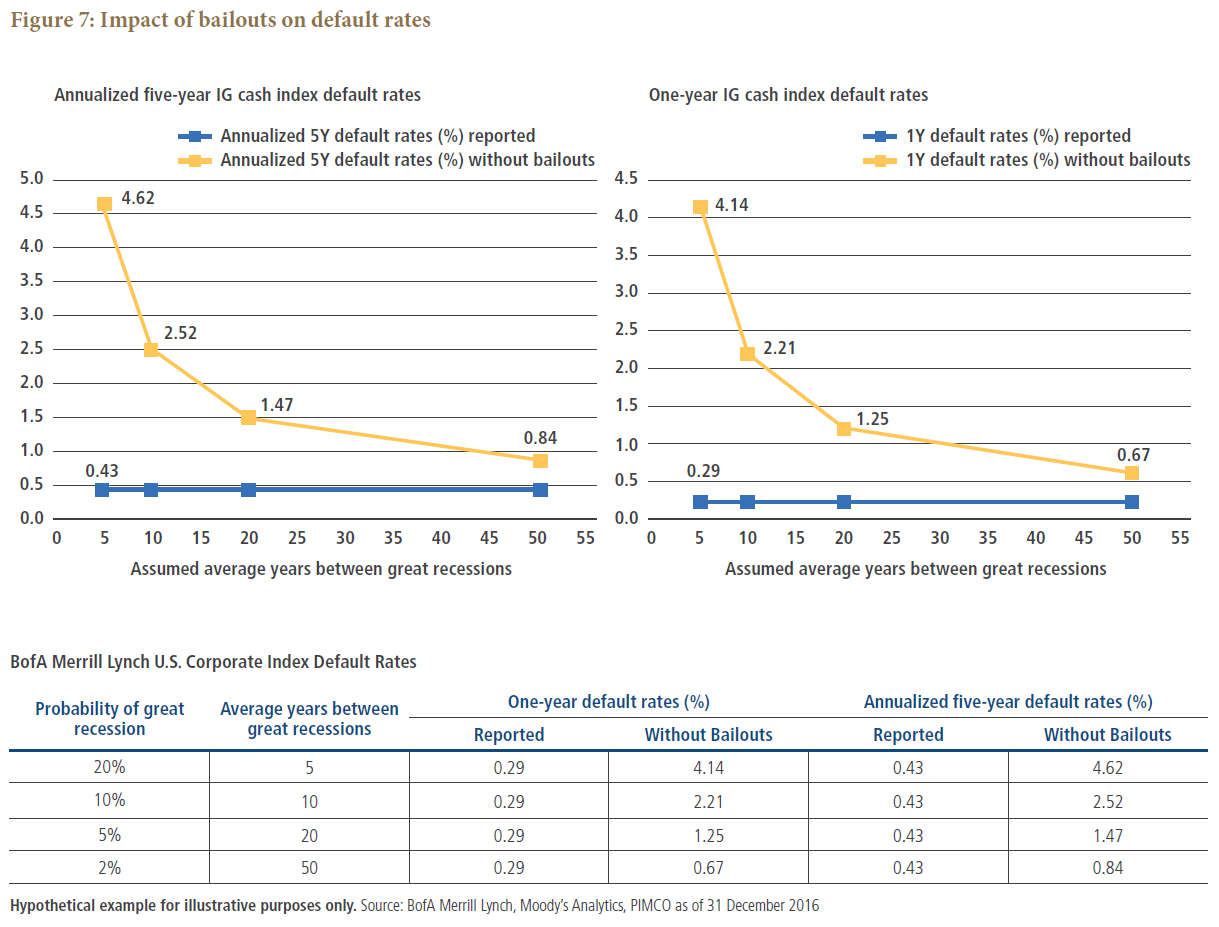

Investors in credit products may be wondering what to believe and what to expect in the months and years ahead. The European Central Bank (ECB) owns billions of euros’ worth of corporate bonds, the Bank of Japan (BOJ) owns billions of yen of corporate bonds and equities, the Swiss National Bank (SNB) owns billions of Swiss francs in equities. Globally, central banks have socialized substantial portions of the financial markets. As such, perhaps investors should believe the reported “government supported” default statistics, perhaps not. Should an investor treat the 2008 episode as a 5, 10, 20, 30, or 50 year event? See Figure 7 for input on the default rates for various event periods.

Absent the context of the bailout inputs, the currently reported default statistics are misleading. Much less clear is the importance to investment portfolios of the revised “shadow” statistics presented herein. This lack of clarity is due to the persistence of central banks’ intrusions into the financial markets and policymakers’ concern for “financial conditions” and the associated wealth effects. The quantitative easing policies directly support financial conditions and have served to finance government budget deficits and private debt at very low interest rates. U.S. government debt has increased from $8.7 trillion in 2007 to $20 trillion at year-end 2016. The corresponding amounts for U.S. corporate debt are $4.1 trillion and $7.7 trillion. Both government and corporate debt in the U.S. essentially doubled while the U.S. nominal GDP increased by only 30%. Based on the increased debt, we would suggest that the financial system is more fragile, more prone to increases in the failure rates of the private economy. However, because the fragility is so great and because of the mediocre growth rates experienced since 2007, we expect a complete withdrawal of policy support unlikely. You make the call – weakening macro debt fundamentals or persistent “free” policy support – as to which debt default statistics are applicable for the future.

Special thanks to Ravi Mattu and Shisheng Qu of PIMCO Analytics Group for their help with this paper.

SELECTED BIBLIOGRAPHY

- Mora N, “What Determines Creditor Recovery Rates?” Economic Review, Second Quarter 2012, Kansas City Federal Reserve Bank

- Chan-Lau J, 2006, “Market-Based Estimation of Default Probabilities and Its Application to Financial Market Surveillance,” IMF Working Paper

- Longstaff F, Mithal S, Neis E, 2005, “Corporate Yield Spreads: Default Risk or Liquidity? New Evidence from the Credit Default Swap Market,” Journal of Finance

- Giesecke K, Longstaff F, Schaefer S, Strebulaev I, 2011, 2011, “Corporate Bond Default Risk: A 150-Year Perspective,” Journal of Financial Economics 102

- Chen H, Cui R, He Z, Milbradt K, 2016, “Quantifying Liquidity and Default Risks of Corporate Bonds over the Business Cycle,” MIT Sloan School and NBER

This paper contains hypothetical analysis. Hypothetical and simulated examples have many inherent limitations and are generally prepared with the benefit of hindsight. There are frequently sharp differences between simulated results and the actual results. There are numerous factors related to the markets in general or the implementation of any specific investment strategy, which cannot be fully accounted for in the preparation of simulated results and all of which can adversely affect actual results. No guarantee is being made that the stated results will be achieved.

Charts are provided for illustrative purposes and are not indicative of the past or future performance of any PIMCO product. It is not possible to invest directly in an unmanaged index.

All investments contain risk and may lose value. Investors should consult their investment professional prior to making an investment decision.

References to specific issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold securities of those issuers. PIMCO products and strategies may or may not include the securities of the issuers referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

© PIMCO

© PIMCO

Read more commentaries by PIMCO