Introduction

Ever since the Financial Crisis of 2008, many hedge funds and other high-profile money managers have complained that their investment approaches and algorithms stopped working due to the extraordinary monetary stimulus introduced by the Federal Reserve Board and other major central banks in response to the Financial Crisis, leading to sub-par investment returns1. This extraordinary stimulus produced by the world’s major central banks helped to create multi-trillion-dollar central bank asset balances on their balance sheets, resulting in over one-third of the world’s government bonds yielding negative rates by the summer of 2016, conditions that are unprecedented. To invest successfully going forward, it will be imperative to understand just how this unprecedented stimulus has affected and distorted market prices of the major global asset classes. Without historical precedent, looking back through history will not provide sufficient insight to truly understand global capital market behavior post-Financial Crisis. Instead, a forward-looking methodology, multi-player game theory, has been explored and applied to provide a more relevant perspective on market behavior going forward.

When the military makes plans to defend against a potential attack or outbreak of war, if the nature of the war is unlike past conflicts, reliance on studies of historical wars will lead to insufficient preparation. Instead, they play war games, which constitute an application of multi-player game theory. They gather intelligence on the state of the potential battlefield, establishing the initial conditions for round #1 of their war game. Potential players likely to engage in the war are identified, and a gap analysis is performed comparing the current state of each player with their respective goals. The gaps help to determine initial moves by certain players as well as the likely reactions to these first moves by the other players involved. Round #1 is played which consists of a series of moves and reactions. Intelligence and judgement are used to determine how the battlefield had likely changed by the end of round #1, setting the initial conditions for round #2. In this manner, several rounds are played, allowing the military planners to gain insight into the counterintuitive behavior that results from the multitude of connections that occur during the game: 1) the affect that players have on each other; 2) the impact players have on the changing battlefield; and 3) the influence that battlefield changes have on each player. Successive war games are played with each game incorporating alternative assumptions and scenarios. In this manner, the military planners hope to gain far more insight into how to defend against the possible outcomes of the potential outbreak of war than might have been possible without playing the games. An analogous approach has been undertaken to determine how the global capital market battlefield has been impacted by the major central bank players since the Financial Crisis of 2008.

Prior to the Financial Crisis, central banks were far more focused on their own domestic goals and influenced far less by changes in capital market prices or by the actions of other central banks. The Federal Reserve Board was the first to introduce extraordinary experiments in monetary policy stimulus by applying quantitative easing concurrently with interest rate reductions to combat the deflationary and recessionary forces created during the Financial Crisis. Their strategy was to use quantitative easing as a mechanism for purchasing trillions of dollars’ worth of bonds, hoping that by elevating asset prices, animal spirits and the wealth effect would lead to a recovery in economic growth. In time, other major central banks followed suit, including the Bank of Japan, People’s Bank of China, the Bank of England and the European Central Bank. Consequently, the nonlinear dynamic system we call the global capital markets had become far more influenced by central bank monetary stimulus than ever before.

The purpose of this paper is to share the underlying principles and logic supporting a multi-player game-theoretic approach within a System Dynamics framework, which is employed to construct globally diversified portfolio strategies on behalf of clients.

Approach

A multi-player game-theoretic approach has been created to describe the impact that unprecedented central bank policies have had on the global capital markets. To guide investment decision making, this theory has been expressed in a computer-based mathematical model that employs a System Dynamics approach. We believe that quantitative models should not be used as a substitute for judgment, experience or logical thinking. Rather, such a model should reflect a synthesis and codification of a collective thinking on global capital market behavior and the influences of extraordinary monetary stimulus.

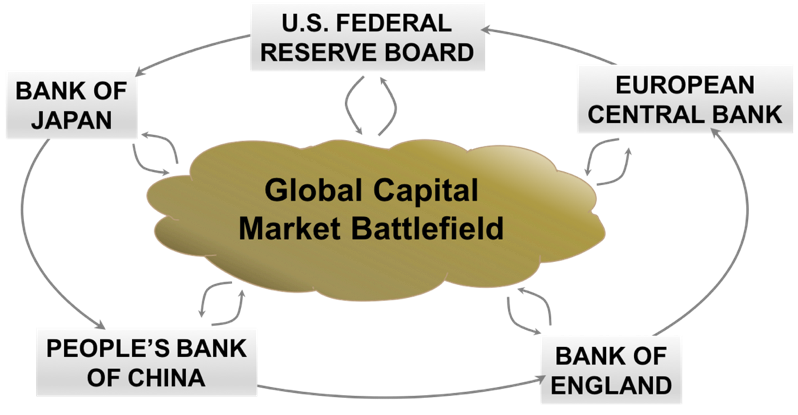

Using the language of game theory2, central banks’ impact on global capital asset prices can be viewed as a sequentially dynamic multi-player game with communication and an infinite horizon, combining elements of cooperation and conflict.

Fig. 1. A sequentially dynamic multi-player game with communication and an infinite horizon, combining elements of cooperation and conflict.

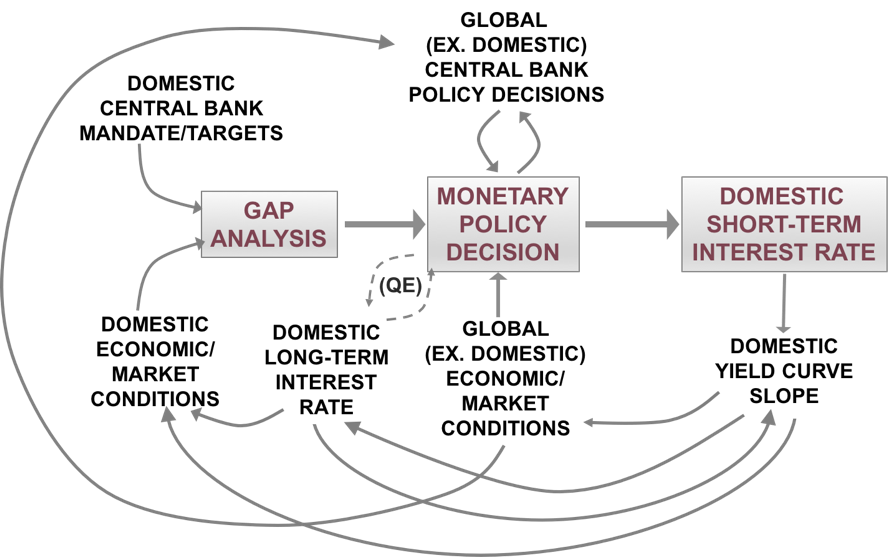

With rare exceptions, central banks announce their policy decisions according to an established schedule, resulting in an ordered sequence of policy decisions among the players. Central bankers meet frequently to cooperate on shared goals such as promoting greater global economic growth. Occasionally central banks have conflicts of interest, for example when one country attempts to increase economic growth at the expense of other countries via promoting the conditions for a competitive currency devaluation, potentially sparking a global currency war. The goal of a central bank’s decision is not to gain an immediate payoff but rather to narrow the gap in typically small increments between the central bank’s stated mandate (e.g. inflation, unemployment rate, economic growth targets) and its country’s current state of economic conditions.

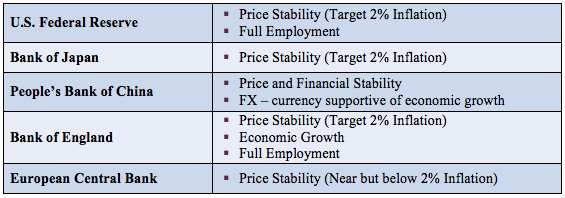

Fig. 2. Central Bank mandates.

While the objective of game-theoretic approaches is to solve for an equilibrium solution or solutions, the global capital markets, like nonlinear systems generally, rarely rest in a stable equilibrium state. Instead, global capital markets typically fluctuate between undervaluation and overvaluation in a perpetual state of disequilibrium. Therefore, rather than attempting to solve for equilibrium solutions that rarely exist in the real world of the global capital markets, we create a game using a System Dynamics framework that iterates through successive rounds seeking to incrementally narrow the gaps between each player and its goals during each round. Consequently, each central bank policy decision influences the other central banks as well as interest rates and currency values, which in turn influence equity, fixed income and real asset prices globally, which then feedback into subsequent central policy decisions.

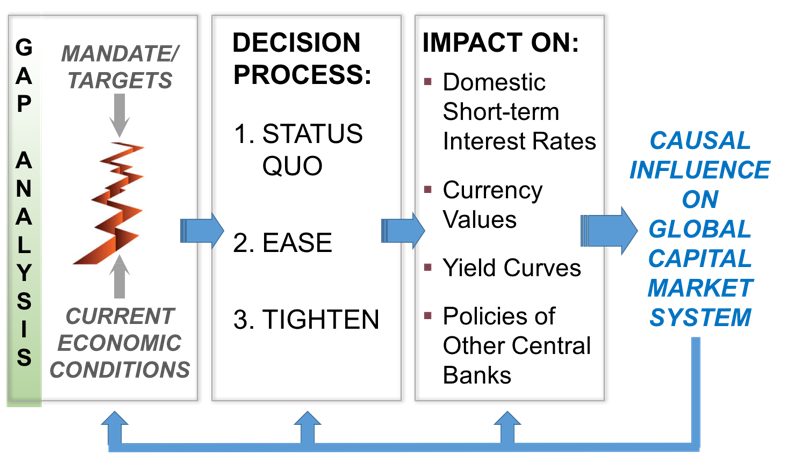

Fig. 3. Gap analysis for each Central Bank.

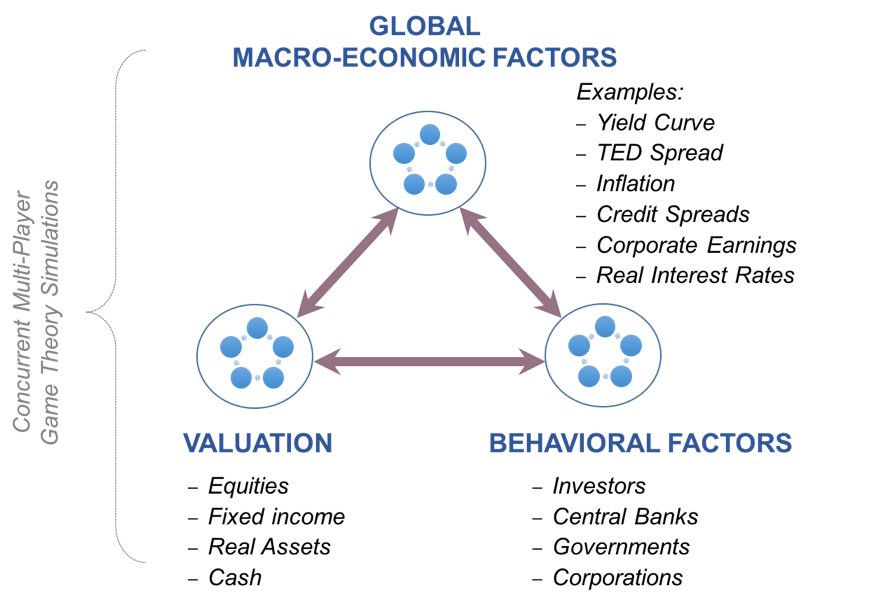

A computer-based mathematical model has been created that captures the key causal relationships and time delays impacting the global capital markets, including a series of global macro-economic relationships, behavioral relationships and valuation metrics, producing a set of projected risk-adjusted returns for each global asset class. The projected risk-adjusted returns are used to create globally diversified portfolios seeking to generate the highest return given a targeted level of risk (defined not only by variance or standard deviation but also by maximum drawdown under extreme adverse conditions), dynamically adapting to changing global macro-economic conditions.

Fig. 4. 3EDGE Global Capital Market Model

To perform the gap analyses between central banks’ stated goals and current economic conditions, the specific mandates for each central bank have been identified. Central bank decision-making has been characterized to have three possible outcomes: 1) maintain current monetary policy (i.e. no change in target interest rate and/or quantitative easing); 2) tighten monetary policy (i.e. raise target interest rate and/or remove quantitative easing); and 3) ease monetary policy (i.e. lower target interest rate and/or add to quantitative easing). In sequential fashion, each central bank assesses its own gap and makes the policy decision that seeks to narrow its gap, typically in small one-quarter percent increments if action is warranted. The targets (inflation, unemployment rate, economic growth) in turn are impacted by the previous decisions of other central banks as well as a multitude of other macro-economic and behavioral causal relationships. Knowing the state of economic conditions at each point in time plus understanding each central bank’s specific mandate allows central bank behavior to be modeled through time.

Fig. 5. Dynamic impact of monetary policy decisions for each Central Bank.

Fig. 6. Impact of monetary policy decisions on domestic equity market values. Highlighting denotes direct impact of Central Bank policy decisions on short-term Treasury yields.

Implementation

With the aid of a mathematical model incorporating a multi-player game-theoretic approach as described in this paper, 3EDGE Asset Management launched its series of portfolio strategies on January 1, 2016. Two weeks prior to launch, the Federal Reserve Board (Fed) for the first time in a decade raised its target Fed Funds Rate by ¼%. In addition, the Fed telegraphed four additional rate hikes in 2016. Furthermore, its change in monetary policy diverged from all other major central banks, as all others continued to promote highly stimulative monetary policies. A static analysis of the impact of a ¼% rate hike from a very low level (0.25%) may have concluded that the market impact of such a small hike would be marginal. However, by applying the game-theoretic approach described above to modeling the impact of the Fed’s December 2015 rate hike, the risk-adjusted projected return of the U.S. equity market produced by the model’s analysis fell below all other major asset classes.

The U.S. stock market declined more sharply (-10.3%) during the first six weeks of calendar year 2016 than during the first six weeks of any other calendar year over the last several decades. The combination of a divergent monetary policy coupled with the expectation of four additional rate hikes in 2016 propelled the U.S. Dollar higher, causing great concern in China and other emerging markets. Consequently, China was unable to maintain its currency peg to the U.S. Dollar, leading to market uncertainty as to how far its Yuan might fall, thereby risking global economic instability. As the U.S. Dollar rose sharply in value, emerging markets suffered, as a significant portion of emerging market debt is denominated in U.S. Dollars, causing emerging market borrowers to repay their debts in an appreciating (more expensive) currency.

As the year 2016 unfolded, the Fed reassessed its policy given the adverse market reaction and “blinked”, announcing that it no longer planned an additional four rate hikes during the year. The U.S. Dollar abruptly reversed course, dropping sharply in value. While this was a major relief for China’s central bank (People’s Bank of China) and other emerging markets, it was unwelcome news for both the European Central Bank (ECB) and the Bank of Japan (BOJ). The ECB and the BOJ had been applying extraordinary monetary stimulus in attempt to reflate their respective economies by facilitating the weakening of their respective currency values, hoping to deliver an advantage to their country’s exporters, thereby helping their countries grow their way out of their chronic debt problems. In each case, the ECB and the BOJ reacted to the decline in the value of the U.S. Dollar caused by the backtracking of Fed policy. The ECB sent its already negative target interest rate more deeply into negative territory, while the BOJ set its target rate to be negative, contrary to a previously announced statement that it would not consider negative interest rates. The negative rates proved to be counterproductive however, as negative rates adversely impact banking profitability, making it more difficult to reflate an economy with a weakened banking system.

Given the changing global macro-economic conditions (influenced by the actions and reactions of the world’s central banks from late 2015 through early 2016), two asset classes, emerging market equities and gold, benefited from the changing conditions. Both asset classes had underperformed for several years, and while these asset classes had become undervalued by several metrics, their recoveries continued to be stalled by the rising U.S. Dollar. After the Fed blinked, the falling U.S. Dollar acted as a positive catalyst, which in turn resulted in projected risk-adjusted returns indicating a recovery in gold and emerging market equities.

A consequence of the extraordinary monetary stimulus since the Financial Crisis of 2008 is that we now believe investors may be faced with a lower-return world going forward. Central banks applied unprecedented stimulus by using quantitative easing as a mechanism for purchasing trillions of dollars’ worth of bonds, hoping that by elevating asset prices, animal spirits and the wealth effect would lead to a recovery in economic growth. While the central banks were successful in raising asset prices, their economies did not grow in a commensurate way. Therefore, the central banks may have effectively robbed investment returns from the future into the present, creating a lower-return world for investors. Fortunately, markets typically don’t move in a linear fashion, meaning that a lower-return world does not necessarily imply that all asset classes are doomed to achieve a low return each year for the next several years. As components of a nonlinear dynamic system, markets tend to fluctuate in cycles between states of undervaluation and overvaluation. Additionally, asset class cycles tend not to fluctuate in perfect phase with one another particularly across asset categories (equities vs. fixed income vs. real assets vs. cash). Therefore, our strategy for achieving attractive returns in a lower-return world without increasing risk is to employ our global capital market model to identify asset classes / market indices which are not only in the undervalued phase of their cycle but also where the catalysts (macro-economic and behavioral causal relationships) have turned positive.

Conclusion

To understand how the unprecedented monetary stimulus introduced by central banks since the Financial Crisis of 2008 has affected and distorted global capital market prices, a multi-player game-theoretic approach to modeling the global capital markets has been created. Because conventional game-theoretic approaches focus on finding equilibrium solutions, a System Dynamics framework was employed to capture the real-world behavior of a sequentially dynamic multi-player game whereby the game’s competitive arena, the global capital markets, typically fluctuate between undervaluation and overvaluation in a perpetual state of disequilibrium while the players (central banks) achieve no finite payoff but rather incrementally seek to narrow the gap between their stated goals / mandates and their current economic conditions. The resulting global capital market model has been employed to help manage a set of portfolio strategies since January 1, 2016 with promising results, an encouraging approach requiring further investigation.

Additional Notes and Disclosures:

1) This material is neither an offer to sell nor a solicitation of an offer to buy and securities. The information provided in this white paper is not intended to provide personal investment advice and does not take into account the unique investment objectives and financial situation of the reader. Investors should only seek investment advice from their individual financial adviser. Investments including common stocks, fixed income, commodities and ETFs etc. involve the risk of loss that investors should be prepared to bear. 3EDGE’s investment strategies employ varying levels of risk which may be substantial and there can be no assurance that an investment in a 3EDGE strategy will be successful. Past performance may not be indicative of future results.

2) Information is current as of July 10, 2017.

3) Asset classes and the provisional weightings in 3EDGE’s portfolios may change at any time without notice subject to our discretion.

4) All opinions expressed in this white paper are the current opinions of Mr. Cucchiaro as of July 10, 2017. Cucchiaro’s opinions may change based on changing economic and market conditions.

5) Our portfolio risk management process is designed with the goal of monitoring and managing risk, but should not be confused with and does not imply low risk or the ability to control risk.

6) There are risks associated with any investment approach, and portfolios have their own set of risks to be aware of. First, there are the risks associated with the long-term core strategic holdings for each of the strategies. The more aggressive the strategy, the more likely the portfolio will contain larger weights in riskier asset classes, such as equities. Second, there are distinct risks associated with portfolios’ shorter-term dynamic allocations, which can result in more concentration of the portfolio towards a certain asset class or classes. This introduces the risk that we could be on the wrong side of a tactical over- or under-weight, thus resulting in a drag on overall performance.

APPENDIX

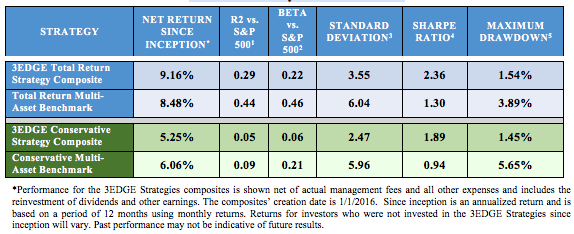

3EDGE Total Return Strategy and 3EDGE Conservative Strategy (“3EDGE Strategies)

Risk/Return Analysis as of 6/30/2017

BENCHMARK COMPOSITION AND DISCLOSURES:

- Total Return Multi-Asset Benchmark: 45% MSCI ACWI, 45% Citigroup CWGBI, 10% BCOMTR

- Conservative Multi-Asset Benchmark: 20% MSCI ACWI, 70% Citigroup CWGBI, 10% BCOMTR

- 3EDGE Asset Management’s investment objective is to seek to earn attractive risk-adjusted returns over full market cycles. We do not actively seek to outperform any specific benchmark index on a relative basis. Nonetheless, we have established the Total Return Multi-Asset Benchmark and Conservative Multi-Asset Benchmark (“Benchmarks”) for the 3EDGE Total Return Strategy and 3EDGE Conservative Strategy respectively. The 3EDGE Strategies are not index funds and their portfolio holdings, country exposure, portfolio characteristics and performance will differ from that of the Benchmarks. The Benchmarks are simply a baseline against which we monitor the 3EDGE strategies. They are intended to represent a passive, global, multi-asset class portfolio with similar risk characteristics to the corresponding 3EDGE Strategy. The Benchmarks have not been selected as specific benchmarks to compare to the performance of the 3EDGE Strategies, but have been provided to allow for comparison of the performance of the 3EDGE Strategies to that of well-known and widely recognized indices. The Indices used in the Benchmark are represented by total return prices. Indexes are unmanaged and therefore do not include fees and expenses typically associated with investments in managed accounts. One cannot invest directly in an index. Benchmark Data Source: Bloomberg.

RISK/RETURN ANALYSIS:

RISK MEASURES:

- R2 is a measure of the portfolio’s correlation with a given benchmark. Calculated as realized values vs. S&P 500.

- Beta is a measure of the volatility of the portfolio in comparison to the market as a whole. Calculated as realized values vs. S&P 500.

- Standard Deviation measures the degree of variation of investment returns around the mean (or average) return and is calculated as the square root of the variance.

- Sharpe Ratio is typically calculated as annualized excess returns divided by annualized volatility. It is a measure of investment return per unit of volatility experienced by the investment within a given investment horizon.

- Maximum Drawdown is a measure of risk that captures the worst cumulative peak-to-trough decline of an investment or portfolio from any month-end data point to any other month-end data point. It shows in percentage terms how much money an investment portfolio would have lost before returning to its breakeven point.

DEFINITIONS:

- The Morgan Stanley Capital International All Country World Index (MSCI ACWI) GR is designed to provide a broad measure of equity market performance throughout the world. Maintained by Morgan Stanley Capital International, it captures large and mid-cap representation across 23 developed and 23 emerging market countries, covering approximately 85% of the global investable equity opportunity set.

- The Citigroup World Government Bond Index (CWGBI) is a broad benchmark providing exposure to the global sovereign fixed income market. It measures the performance of fixed-rate, local currency, investment-grade sovereign bonds comprising sovereign debt from over 20 countries, denominated in a variety of currencies.

- The Bloomberg Commodity Index (BCOM) is a broadly diversified commodity price index tracking prices of futures contracts on physical commodities on the commodity markets. The Bloomberg Commodity Index Total Return (BCOMTR) reflects the BCOM on a “total return” basis, combining the BCOM returns with the returns on cash collateral invested in 13 week U.S. Treasury Bills.

3EDGE ASSET MANAGEMENT, LP (“3EDGE”) DISCLOSURE PRESENTATION

TOTAL RETURN STRATEGY COMPOSITE

*Composite dispersion is shown annually and/or there are fewer than 5 accounts in the composite for the entire year.

The three-year annualized ex-post standard deviation of the composite and/or benchmark is not presented because 36 monthly returns are not available. It will be presented beginning 2018.

Total Return Strategy Composite: The investment objective of the 3EDGE Total Return Strategy is to generate long-term capital appreciation and attractive risk-adjusted returns over full market cycles. It is rebalanced on a model-driven basis. It is globally diversified and seeks to generate moderate, equity-like returns but with less risk than traditional equity portfolios. The Strategy may be appropriate for investors who are more focused on longer-term capital appreciation and those who have a longer-term time horizon in mind of greater than 3 years. There are no fixed limitations on the exposure to any particular asset class in this Strategy and no fixed limitations on holdings in any particular country. However, under normal conditions the Strategy will hold a higher percentage of U.S. securities than non-U.S. securities (up to 100% of the Strategy). Composite creation date is 1/1/2016.

The benchmark is 45% Citigroup World Government Bond Index CWGBI/ 45% Morgan Stanley Capital International All Country World Index MSCI ACWI GR / 10% Bloomberg Commodity Total Return Index BCOMTR. The benchmark is rebalanced on a monthly basis and its returns are gross of withholding taxes.

CONSERVATIVE STRATEGY COMPOSITE

*Composite dispersion is shown annually and/or there are fewer than 5 accounts in the composite for the entire year.

The three-year annualized ex-post standard deviation of the composite and/or benchmark is not presented because 36 monthly returns are not available. It will be presented beginning 2018.

Conservative Strategy Composite: The investment objective of the 3EDGE Conservative Strategy is to focus more on preservation of capital and management of volatility, while still seeking to generate attractive risk-adjusted returns over full market cycles. It is rebalanced on a model-driven basis. The Strategy is globally diversified and may be appropriate for investors who are more risk averse, who may rely on it for current income or are investing with a relatively shorter time horizon of 1 to 3 years. Along with interest and dividends from some holdings, the Strategy will also rely on capital appreciation as a component of total returns, for example from sale of appreciated stock. The Strategy also seeks a long-term rate of return that, where possible, stays ahead of the rate of inflation. There are no fixed limitations on the exposure to any particular asset class and no fixed limitations on holdings in any particular country. However, under normal conditions the Strategy will hold a higher percentage of U.S. securities than non-U.S. securities (up to 100% of the portfolio). Composite creation date is 1/1/2016.

The benchmark is 70% Citigroup World Government Bond Index CWGBI / 20% Morgan Stanley Capital International All Country World Index MSCI ACWI GR / 10% Bloomberg Commodity Total Return Index BCOMTR. The benchmark is rebalanced on a monthly basis and its returns are gross of withholding taxes.

3EDGE Asset Management, LP is an investment management firm focusing on a global, multi-asset investment strategy that seeks to blend scientific methodology with sound judgment and practical experience. Headquartered in Boston, the firm provides investment management services to both private clients and institutional investors.

3EDGE claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. 3EDGE has been independently verified for the periods 1/1/2016 through 3/31/2017. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and (2) the firm’s policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. The Total Return Strategy Composite and the Conservative Strategy Composite have been examined for the periods 1/1/2016 through 03/31/2017. The verification and performance examination reports are available upon request.

The firm’s list of composite descriptions is available upon request.

The U.S. Dollar is the currency used to express performance. Returns are presented gross and net of management fees and include the reinvestment of all income. Net of fee performance was calculated using actual management fees. In some instances, net of fee performance has been also reduced by the adviser’s fees where 3EDGE is the sub-adviser. The annual composite dispersion presented is an asset-weighted standard deviation calculated for the accounts in the composite the entire year. Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request. Composite performance is presented gross of foreign withholding taxes on dividends, interest income and capital gains. Past performance is not indicative of future results.

The investment management fee schedule for the composite is 0.80% on the first $1 million, 0.70% on the next $4 million, 0.60% on the next $45 million and 0.50% on the amount over $50 million. Actual investment advisory fees

1 Johnson, M. “Are macro investors suffering because of ‘pseudo-science’?” Financial Times, 10 July 2017.

© 3EDGE Asset Management

Read more commentaries by 3EDGE Asset Management

BENCHMARK COMPOSITION AND DISCLOSURES:

BENCHMARK COMPOSITION AND DISCLOSURES: