For many U.S. equity investors, the last eight years have been great.

Since the lows of the global financial crisis in March 2009, U.S. stocks (proxied by the S&P 500) have returned 270%, or 16.8% annualized, outpacing every other major market over that period. Contributing to that outperformance were highly differentiated returns among asset classes, particularly in the three calendar years following the “taper tantrum” sparked by comments from then-Fed Chairman Ben Bernanke. Starting in 2013 and through 2015, the S&P 500 Index gained 52% cumulatively, whereas core bonds returned 4% (proxied by the Bloomberg Barclays U.S. Aggregate Bond Index) and an equally weighted basket of diversifying assets (see below) actually lost value, returning −12%. In other words, diversifiers lagged U.S. stocks by 64% for the 2013–2015 period.

While that experience was uncomfortable for many diversified investors, the silver lining is that returns come in cycles. Extended outperformance cycles are typically followed by underperformance cycles (and vice versa). As prices get too rich and yields drop too low, investors rotate to other investment options offering higher return potential.

Who’s up next?

Not surprisingly, after a sustained period of return leadership by U.S. stocks, a number of diversifying assets now appear poised for outperformance going forward.

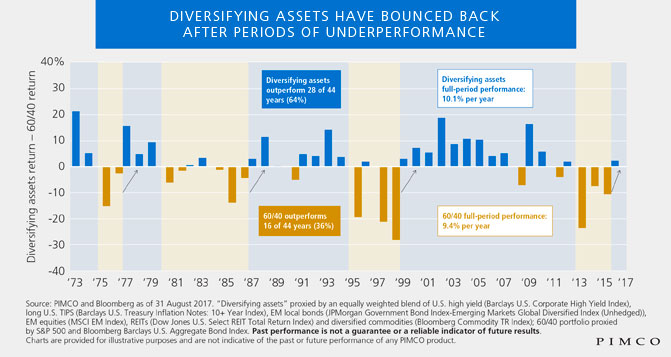

To illustrate this cyclical return pattern, we compared the return of a traditional U.S. 60/40 portfolio (proxied by the S&P 500 and the Bloomberg Barclays U.S. Aggregate Bond Index) to an equally weighted mix of six key diversifiers (Treasury Inflation-Protected Securities (TIPS), commodities, real estate investment trusts (REITs), emerging market (EM) stocks, EM local bonds, and high yield debt) over the past 44 years (see chart).

The pattern? After periods of sustained outperformance by U.S. 60/40 portfolios (largely driven by the 60% in U.S. stocks), the “rubber band” of relative valuations gets stretched too tight, and the diversifiers come bouncing back for a subsequent period of sustained outperformance. (Of course, past performance is never a guarantee or necessarily a reliable indicator of future results, but such patterns can be informative.)

A triple threat for U.S. equities?

In the above chart, two periods in particular stand out. The dot.com–fueled bull market of the late 1990s through early 2000 drove significant outperformance of U.S. 60/40 over diversifiers; this was followed by more than a decade of outperformance by diversifying assets, which made up the shortfall with room to spare. And in 2013–2015, U.S. stocks again drove meaningful outperformance of U.S. 60/40 versus diversifiers before the diversifiers began to rebound in 2016, and we think diversifying assets may still be in the early stages of a sustained outperformance cycle.

Looking at current U.S. equity valuation metrics reinforces this view. The S&P 500 is facing a triple threat: Dividend yields are near historical lows, earnings levels are near historical highs and cyclically adjusted price-to-earnings ratios also appear high by historical standards.

In contrast, many diversifying markets, which have lagged in the recent past, now offer relatively attractive starting prices, yields, and (in our view) forward-looking return potential.

Investment implications

Given fully valued U.S. stock markets, what should investors do? One potential solution is to consider strategies designed to harness the complimentary return potential of diversifying assets.

In our view, the diversifiers are up next.

U.S. investors: Learn more about diversified asset allocation in our recent piece, “Seeking Returns When U.S. Markets Are Fully Valued.”

John Cavalieri is a PIMCO asset allocation strategist.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. REITs are subject to risk, such as poor performance by the manager, adverse changes to tax laws or failure to qualify for tax-free pass-through of income. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

© PIMCO

© PIMCO

Read more commentaries by PIMCO