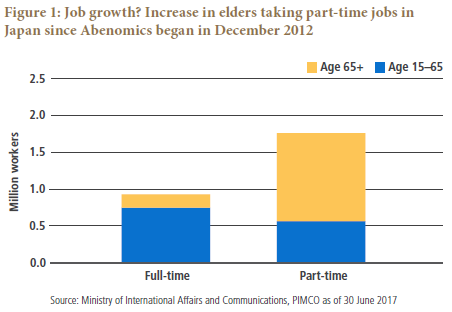

First, longevity has spurred retirees to return to the job market as part-time workers, who tend to accept wage cuts or lower-wage jobs in exchange for flexible work hours (see Figure 1); this is weighing on aggregate wage growth despite job growth. At the same time, increasing life expectancy coupled with the poor outlook for social security seems to be incentivizing even younger workers to accept little or no wage growth in return for job security rather than demanding wage increases or taking the risk of switching to higher-wage jobs. The preference for job security is probably a supply-side impediment to labor mobility, while labor law restrictions on discharges (layoffs) play a demand-side role.

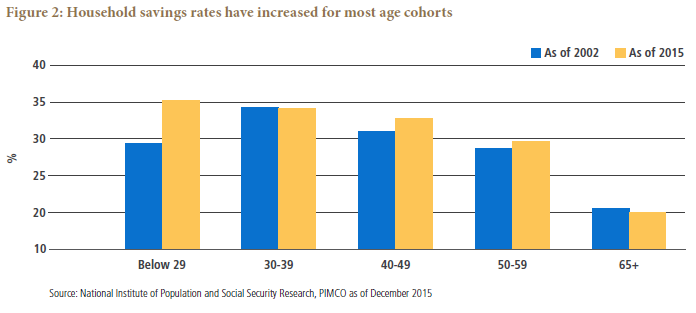

Second, longevity, together with the poor outlook for social security, has encouraged precautionary saving. The household savings rate has increased over the last decade or so among most age cohorts, particularly the youngest (age 29 and below), as shown in Figure 2. The younger generation is a growing minority in an aging society, and its members are aware that their social security benefits will most likely be lower than their contributions over their lifetime.

Third, cohort effects are cementing expectations for zero inflation (or even deflation) over time. With no inflation over the last two-and-a-half decades, many Japanese now have no experience with inflation. This is important because, as the BOJ admitted in its self-assessment last September, the private sector’s inflation expectation is “adaptive” – influenced by past deflation and the current zero-inflation experience – rather than “rational” (that is, anchored by a target like the BOJ’s).

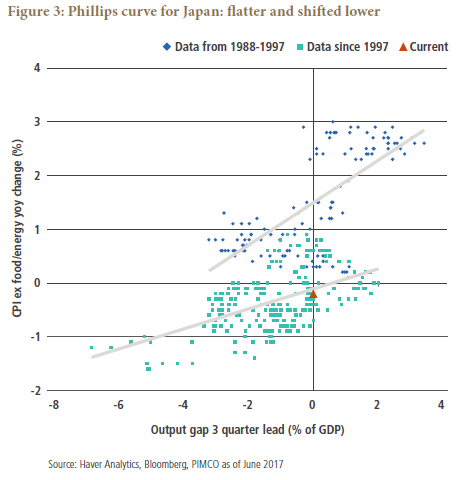

Although demographic factors in general can be inflationary or deflationary, as they affect both aggregate supply and demand in the economy, net-net in Japan, they probably are structural deflationary forces. As Figure 3 shows, the Phillips curve, which aims to explain the relationship between an economy’s output gap and inflation, has dramatically flattened and shifted lower over the last decade or so. Older workers accepting wage cuts or low-paying jobs as part-time workers helps explain the flattening of the Phillips curve. Labor immobility is another factor. The demographic cohort effects that weigh on inflation expectations explain (if not fully) the downward shift of the Phillips curve. And as precautionary saving rises even among younger generations, the efficacy of monetary easing via lower interest rates has been reduced.

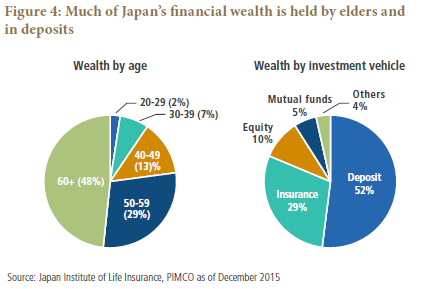

Demographic trends cast doubt on the BOJ’s 2% inflation target not only economically, but also politically. Inflation in general erodes the purchasing power of savers, and in Japan, the older generation would be the most affected: About half of household financial wealth in Japan is held by people 60 years or older and in bank deposits (see Figure 4). This older cohort is the most influential politically in Japan, where about two-thirds of the voters in the last general election were 50 years or older. An episode in 2015 was a clear illustration: As the CPI excluding the tax hike effect rose 1.5% (due mostly to the weak currency and resulting rise in import prices), politicians started to verbally intervene in the currency markets by voicing concerns about retirees’ purchasing power.

INCREASINGLY ‘FISCAL DOMINANT’ POLICY

The BOJ’s conclusion that inflation expectations are adaptive (rather than rational) is reasonable but ironic. Modern macroeconomic theory assumes rational expectations, and this has been a fundamental basis for the BOJ’s aggressive monetary easing under Kuroda. Having hit its policy limit, the BOJ cannot meet its legal mandate of price stability in the future unless a new economic theory emerges or the government cooperates.

Ideally, the government should deliver sound supply-side reforms. The social security system could be reformed such that younger generations would feel more confident, with less punitive inter-generational wealth transfers. Labor regulations could also be amended to achieve mobility and hence better allocation of resources. However, these long-term positive reforms can be negative for the economy in the short term and therefore are unlikely to be delivered now that Prime Minister Abe’s political capital has eroded.

In reality, therefore, fiscal policy or another demand-side policy will likely emerge in coordination with monetary policy going forward. The BOJ’s yield curve control (where the bank targets the very front end, or interest on excess reserves, and the 10-year points on the yield curve) is a smart measure to incentivize politicians to open up the fiscal wallet: The BOJ is standing by to finance any new government debt at super-low yields. The government signaled that it may be preparing for monetary-financed fiscal stimulus in June when it added a reduction of the government debt-to-GDP ratio as a supplementary measure for fiscal consolidation. Focusing on debt-to-GDP instead of the existing measure of primary budget balance would give the government more flexibility in using fiscal policy while the BOJ is keeping government bond yields artificially low.

To what extent Japan’s policy will shift from monetary to fiscal dominance (“helicopter money”) is unclear at this stage, but at least the direction seems clear: The BOJ will no longer take the lead on policy. In an economic downturn, fiscal stimulus would likely be the preferred policy response, while the BOJ would assist by keeping rates low. In any future attempts at policy exit, the BOJ would likely move slowly in order to assist the government’s debt management amid Japan’s mounting debt. Doing so would be consistent with the central bank’s other mandate, financial system stability.

YIELD CURVE CONTROL TO BE ADJUSTED

The BOJ’s yield curve control is a smart measure designed to extend policy longevity. However, it too cannot be continued for too long without some adjustment, in our view.

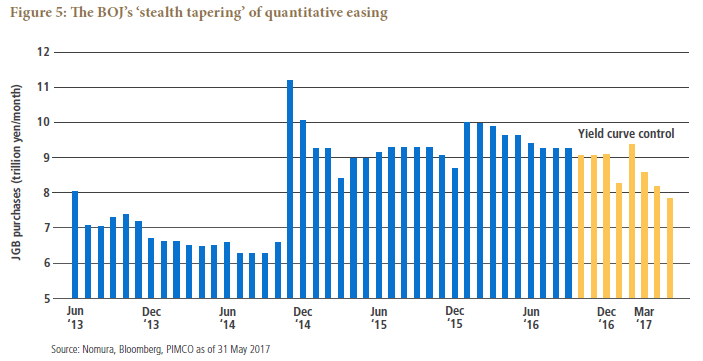

To be fair, yield curve control has been operationally working as intended. Both very front-end and 10-year yields have been well controlled around their targets. The BOJ’s monthly purchase of Japanese government bonds (JGBs) has declined since yield curve control began, allowing the BOJ to do what we call “stealth tapering” of its quantitative easing program (see Figure 5). The BOJ can control the yield curve with smaller JGB purchases today, as it has absorbed a large amount of duration risk from the market already.

The operational success of yield curve control aside, we doubt that the current targets for the yield curve are appropriate. The BOJ admitted in its self-assessment last year that there are side effects to lowering yields and flattening the yield curve to extreme levels, particularly for financial institutions. We would argue that the economy would probably be better off with a steeper, not flatter, yield curve given the structural precautionary saving among households.

POLICY OUTLOOK AND INVESTMENT IMPLICATIONS

To conclude, no matter who is the next BOJ governor, we think the BOJ will take a back seat on policy, look for opportunities to adjust its yield-curve targets higher, and become more flexible on the 2% inflation target. Any adjustment process will be gradual and unlikely to start until the CPI is rising by 1%, so BOJ liquidity should continue to provide marginal support for global markets. Yet it is important to avoid being complacent; any adjustment to the 10-year yield target would be unprecedented and therefore may not be a smooth operation.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

©2017, PIMCO.

© PIMCO

Read more commentaries by PIMCO