The changing demographics of the municipal bond market in recent years, coupled with their reliable tax-free-income stream, has made munis a compelling core allocation for today’s fixed-income investors.

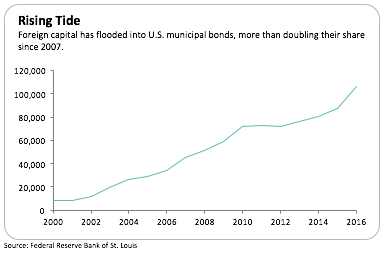

Munis were once a sleepy corner of the bond market where retail investors held mostly illiquid issues. But times have changed. Today, a flood of institutional and foreign investors are using munis to shore up their balance sheets, which has vastly improved liquidity, says Ozan Volkan, portfolio manager for Oppenheimer Investment Advisers.

While the Federal Reserve is committed to tightening monetary policy, he expects a measured and orderly rise in interest rates. That means the current tightening cycle is unlikely to mirror past periods of rising rates in its pace and increments—good news for muni bondholders

In an interview, Volkan explains why he believes the Fed rate hikes are far less perilous than investors think and how President Trump’s proposed tax reform won’t undercut the benefit of owning munis. For more on where municipal bonds fit in a portfolio, how monetary and public policy will influence his outlook and why he favors general obligation bonds with a favorable pension funding profile, read on.

1. What are the chief benefits of including municipal bonds in an investor’s portfolio?

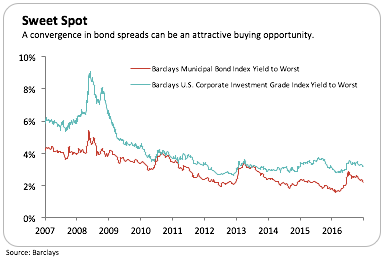

Municipal bonds provide tax-free income and high taxable-equivalent yields. Historically, munis have exhibited lower volatility and lower default rates than other bonds. On average, munis have also exhibited higher credit quality than corporate bonds and mortgages (Source: Moody’s U.S. Municipal Bonds Defaults and Recoveries 1970-2015.) In the municipal bond market, the deterioration of credit fundamentals and distressed debt situations—such as bankruptcies and restructurings—tend to unfold gradually with a lot of warning signs. Further, many muni bonds could be considered socially conscious investments, in that the projects they finance provide essential public services such as education, hospitals, housing, public transportation, clean water, sewers, bridges and tunnels.

2. What positive changes in the municipal bond market have you observed?

Historically, municipal bonds have been less liquid and owned mostly by retail investors (Source: SEC Report on Municipal Securities July 2012.) A high number of issues and smaller par amounts outstanding caused wider bid/offer spreads. However, a lot has changed in the last decade. The proliferation of SMAs and strong interest from crossover buyers—banks, insurers, money market funds, ETFs and even foreign investors—has vastly improved liquidity. We believe this “institutionalization” of the muni market will only accelerate with more banks treating munis as high-quality liquid assets on their balance sheets. Further, the perceived safety and attractive yields of U.S. munis have beckoned foreign investors who can’t find comparable yields in their home countries. What had been a domestic asset class due to the tax exemption has gone global.

3. How do you expect municipal bonds to perform in a rising rate environment? What about a new tax regime?

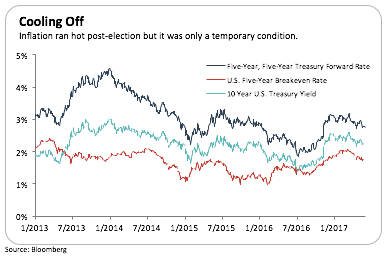

The Fed’s tightening cycle seems to be different than the previous ones we’ve seen in that rates are rising gradually. That’s not only evident in the Fed’s dovish remarks, but also in the technical indicators we follow. Measures of future expected inflation reveal that the post-election spike in rates was largely an overreaction to President Trump’s victory. Treasury forward rates and term premiums, the additional yield bond investors seek in exchange for holding a long-term bond in place of short-term bonds, have dropped. Also, after reaching a record number of shorts post-election, speculator positioning in Treasury futures shifted to neutral in May.

We believe municipal bonds are well-positioned to endure the changing interest-rate environment. As long as these dynamics play out gradually, all market participants should welcome a small but slow run-up in yield. Like many asset classes, the performance of municipal bonds will depend on President Trump’s fiscal policies, particularly tax reform. There have been periods when the highest marginal tax bracket was much lower than it is today but municipal bonds were more richly valued. Regardless of the extent of tax reform, we think investors will still deeply value tax exemption. And munis are the only asset class that provides tax-free income.