SUMMARY

- In 2013, U.S. Treasury yields rose dramatically after then-Fed Chairman Ben Bernanke suggested the central bank might begin reducing its pace of monthly asset purchases. The so-called taper tantrum affected markets globally.

- Today, the Fed is openly discussing plans to begin shrinking its balance sheet in 2017 – yet Treasury yields remain stable.

- We see two explanations for this striking disparity in the market’s response. First, unlike in 2013, both the Fed and market participants accept the New Neutral for U.S. monetary policy. Second, the Fed plans to continue buying duration and convexity risk for at least a year after balance sheet normalization begins.

Recent communications from the Federal Reserve suggest it is likely to begin shrinking (“normalizing”) its balance sheet this year. U.S. Treasury markets have responded with what amounts to a collective yawn. Why? And could this change?

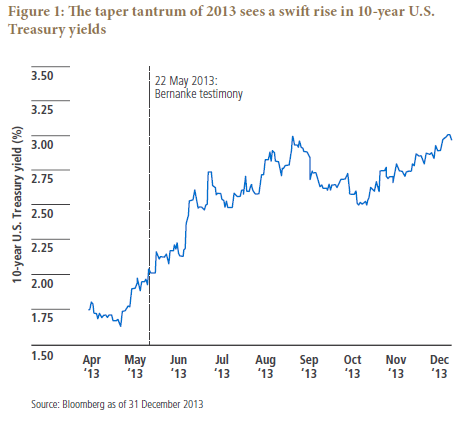

Contrast this with the turmoil that engulfed bond markets four years ago after then-Fed Chairman Ben Bernanke, in testimony before the Joint Economic Committee on 22 May 2013, made reference to the possibility that the Fed at some point would re-evaluate the third round of its asset purchase program, in place since September 2012. Bernanke suggested that at some future date, the Fed could consider reducing the program’s pace of purchasing $45 billion of U.S. Treasuries and $40 billion of mortgage-backed securities (MBS) each month. He commented, “If we see continued improvement [in the labor market outlook] and we have confidence that that is going to be sustained, then we could in the next few meetings, take a step down in our pace of purchases.” He went on to caution that this was “dependent on the data. … If the recovery were to falter, if inflation were to fall further and we felt that the current level of monetary accommodation was still appropriate, then we would delay that process.”

But there’s little doubt where most investors focused their attention. Following Bernanke’s testimony, the market reaction – dubbed the “taper tantrum” by the financial press – was swift and sharp. The yield on the 10-year Treasury note (see Figure 1) rose from 1.94% the day before the testimony in May 2013 to 3.04% percent at the end of December 2013 (two weeks after the actual tapering program was announced after the December Fed meeting). And the sell-off was not confined to the U.S., with global bond yields rising in tandem with the Treasury market.

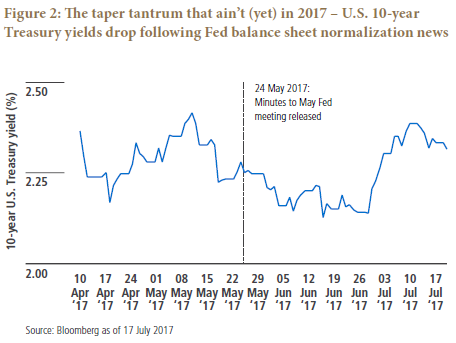

How times change. On 24 May 2017, almost exactly four years after Bernanke’s market-rattling testimony, the Federal Open Market Committee (FOMC) released the minutes to its May 2017 meeting. The minutes indicated there was broad agreement in the FOMC to commence the process of shrinking the Fed balance sheet sometime later this year and that this process would entail setting pre-announced caps on the maximum amounts of Treasury and MBS securities that would be allowed to roll off or prepay each month. Several weeks later, right after its meeting on 13–14 June, the Fed released an “Addendum to the Policy Normalization Principles and Plans,” which reaffirmed that the FOMC would like to commence the process of balance sheet normalization later in 2017. The addendum revealed that the caps discussed above would be set initially at $4 billion per month for MBS and $6 billion per month for Treasuries, rising gradually over the next 12 months to $20 billion and $30 billion per month, respectively.

The market reaction to this momentous news in monetary policy? Instead of another tantrum, bond yields fell! See Figure 2. In late June, yields did rise somewhat, but they still didn’t reach the levels they touched in the weeks prior to the release of the May meeting minutes and remain well below their 2017 highs (from March).

This raises a question I hear a lot from clients and television hosts: Why wasn’t there a taper tantrum in 2017 – when the Fed signaled that it would start shrinking the balance sheet sometime this year, including details on implementation – when there was certainly a taper tantrum in 2013 after the Fed suggested it might merely begin to slow the rate at which the balance sheet was growing?

As with almost any interesting question involving financial markets and the economy, the honest answer is that there is no single explanation. But in the case of “the taper tantrum that ain’t,” two important factors (which receive less attention than they should) may account for much of the sanguine market reaction to the great quantitative easing (QE) U-turn:

- Unlike in 2013, both the Fed and market participants accept the New Neutral for U.S. monetary policy.

- The Fed plans to continue buying duration and convexity risk for at least a year after balance sheet normalization begins.

Let’s analyze each factor in turn.

The 2013 taper tantrum reflected old neutral thinking

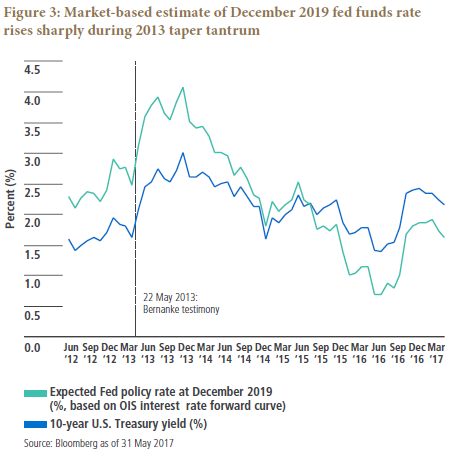

Going into Ben Bernanke’s testimony in May 2013, the OIS (overnight index swap) interest rate forward curve was pricing in an expected Fed policy rate of about 2.5% by year-end 2019. In the months that followed, as shown in Figure 3, the same forward curve had expectations for the December 2019 Fed policy rate reaching higher than 4%. This repricing of the expected fed funds rate hike trajectory during the taper tantrum was greater than the increase in 10-year Treasury yields during the tantrum.

Today, even after four Fed rate hikes and the imminent beginning of balance sheet normalization, market pricing of the expected fed funds rate by December 2019 fluctuates around or slightly below 2%. Thus, one important reason that 2017 is the year of the “taper tantrum that ain’t” is that, in contrast to 2013, the market is pricing in – and the Fed belatedly endorses – a New Neutral for monetary policy (which PIMCO first asserted in 2014) with a neutral fed funds rate much closer to 2% than to the old neutral of 4%. Shrinking the balance sheet is not expected to change that.

The ‘two desserts’ approach to shrinking the Fed balance sheet

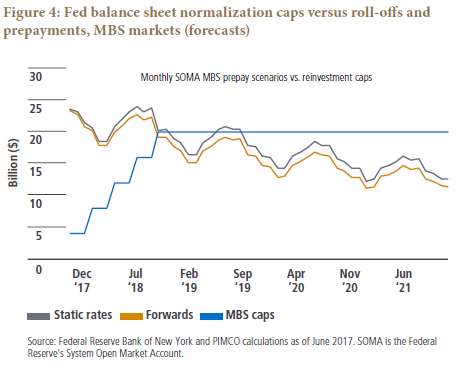

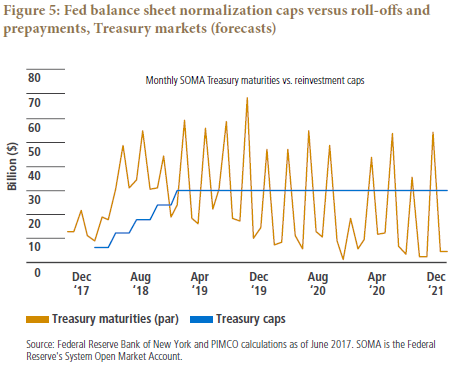

A second reason for the “taper tantrum that ain’t” lurks in the details of the normalization framework. It’s akin to aiming to lose weight by cutting back from three desserts to two desserts at every meal. Under the plan laid out in the Addendum, the Fed will announce caps on the maximum amounts of Treasury and MBS securities that will be allowed to roll off or prepay each month. These caps are likely to be binding for the first nine to 12 months of the program. This means that even as the balance sheet is shrinking, the Fed will still be buying lots of MBS and Treasuries for at least nine to 12 months (see Figures 4 and 5) and thus taking some duration and convexity risk out of the markets. PIMCO projects that after the first year of normalization, the caps on the MBS will cease to bind and the Fed will actually stop buying mortgages. But into the next decade and even after the caps on Treasuries are increased to $30 billion per month, the Fed will still be active in the Treasury market.

Clear sailing ahead, or could balance sheet normalization still jolt markets?

By communicating it believes in a New Neutral for the policy rate and by rolling out a predictable plan for balance sheet normalization that will have the Fed continuing to buy a lot of MBS during the first year as well as Treasuries for even longer, the Fed has avoided a repeat of the taper tantrum so far. Is the coast clear? No. If either of the factors discussed here were to reverse – i.e., a market repricing up to an old neutral for the fed funds rate or a market-unfriendly change in the Fed’s balance sheet normalization framework – another taper tantrum could result.

Moreover, there are other factors that exert a heavy influence on U.S. Treasury yields, in particular the stance of global monetary policies. We pay careful attention to the QE programs and negative rate regimes in the eurozone and Japan as well as the possibility that the Bank of England or the Bank of Canada may tilt toward a rate hike in the months ahead. Recently, markets have begun to price in higher odds of a pivot point in global monetary policies toward a more hawkish stance. If that happens, then another taper tantrum is possible, albeit one that would be triggered by global central banks, not the Fed. Stay tuned!

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL is a trademark of Pacific Investment Management Company LLC in the United States and throughout the world. ©2017, PIMCO.

PIMCO Investments LLC, distributor, 1633 Broadway, New York, NY, 10019 is a company of PIMCO.

© PIMCO

Read more commentaries by PIMCO