ROADMAP

-

In the world: A recap of world events, including an update on global growth trends, major political developments and changes to policies that drive financial markets.

-

In the markets: A quick review of performance by asset class, including global equities, commodities, currencies, and both developed and emerging market bonds.

-

Outlook: The latest update to PIMCO’s outlook for global growth, including where we are most optimistic and the risks we are watching on the cyclical horizon.

-

In sight: A close look at a significant development over the past month and our take on its implications for investors.

Divisions in the U.S. House of Representatives signaled some deterioration in the political scene in Washington, while Brussels found firmer footing. In the U.S., highly anticipated agenda items were put in question by the cancelation of a healthcare vote, while Europe’s lurch toward populism stalled in Dutch elections.

Economic data indicated positive growth momentum globally.Fundamental data including Purchasing Managers’ Indices (PMIs) in the U.S., Europe and emerging markets all indicated steady global growth. In the U.S., both growth and inflation trends gave the Fed an opportunity to continue on its path to policy normalization.

International markets outperformed as the post-election rally in the U.S. paused. Equity markets globally advanced while U.S. markets lost some steam. Of note, U.S. rates were largely unchanged despite the Fed’s rate hike.

In the world

The political scene in Washington appeared to deteriorate, while Brussels found firmer footing. Divisions among U.S. congressional Republicans threw a wrench in the Trump Administration’s plans as the proposed American Health Care Act (AHCA) was pulled from the House floor in the eleventh hour after it became apparent that there weren’t enough votes to secure its passage. The misstep put the post-U.S. election rally on shakier ground as some investors grew concerned about the administration’s ability to advance other ambitious agenda items, such as tax reform and infrastructure spending – expectations for which had contributed to investor confidence. In contrast, Europe’s political unity appeared stronger, as Geert Wilders’ Freedom Party failed to persuade enough voters to support its more extreme anti-Muslim and anti-EU positions in the Dutch parliamentary elections. That, combined with a debate performance by Emmanuel Macron that tempered populist candidate Marine Le Pen’s chances of victory in the French presidential election, signaled more stability for the Continent’s political structure than previously thought. Still, the U.K.’s official notification of its intention to withdraw from the EU – clearing the way for negotiations to take place – was a reminder that meaningful political risk persists in the region.

Fundamental data from across the world pointed toward positive momentum in global growth. Manufacturing PMIs (Purchasing Managers’ Indices) in the U.S., Europe and across emerging markets (EM) continued to indicate a broad-based expansion as trade remained well supported. Flash releases for PMIs in the eurozone reached near six-year highs. Strong gains in employment, accelerating growth in new orders and firming price pressures all underpinned the strong PMI figures and indicated solid growth momentum in the region. Economic data releases in the U.S. also underscored positive trends in its domestic economy. Nonfarm payrolls showed that 235,000 jobs were added in February and growth in average hourly earnings crept up to 2.8% as the trend in wage and job growth continued apace. Meanwhile, the headline U.S. consumer price index accelerated 2.7%, reaching the highest level in five years. With both steady growth and inflation trends providing tailwinds, the Fed opportunistically hiked rates against a relatively calm backdrop in financial markets. Following the Fed’s move, the People’s Bank of China raised short-term repo rates in a move intended to tighten financial conditions. This was the most recent example of policymakers focusing on stability in financial markets ahead of the 19th National Party Congress to be held later this year.

International markets outperformed as the post-election rally in the U.S. paused. The MSCI All Country World Index (ex-U.S.) rose over 2.5%, led by strong performance from Europe and emerging markets, while the S&P 500 was largely unchanged. The U.S. post-election rally took a breather as the Republicans’ failure to bring the AHCA to a successful vote raised concerns over the party’s ability to unite around other important legislation in their pro-growth agenda. Reversals in equity market trends that had been prevalent in the wake of the U.S. election also underscored this waning political optimism: Over the quarter, growth outperformed value (9% vs. 3%), and large caps outpaced small caps (6% vs. 2%)i. Meanwhile, oil prices slumped 5% in response to record-high U.S. inventory levels and doubts about OPEC’s commitment to recently announced production cuts. This contributed to a widening in high yield spreads for the first time since June of last year. U.S. rates were little changed despite the Fed tightening policy rates by 25 basis points (bps). Policymakers’ reiteration of a gradual pace for future hikes kept 10-year yields flat in the U.S., while equivalent yields rose 12 bps in Germany amid the region’s improved risk sentiment.

Looking Up

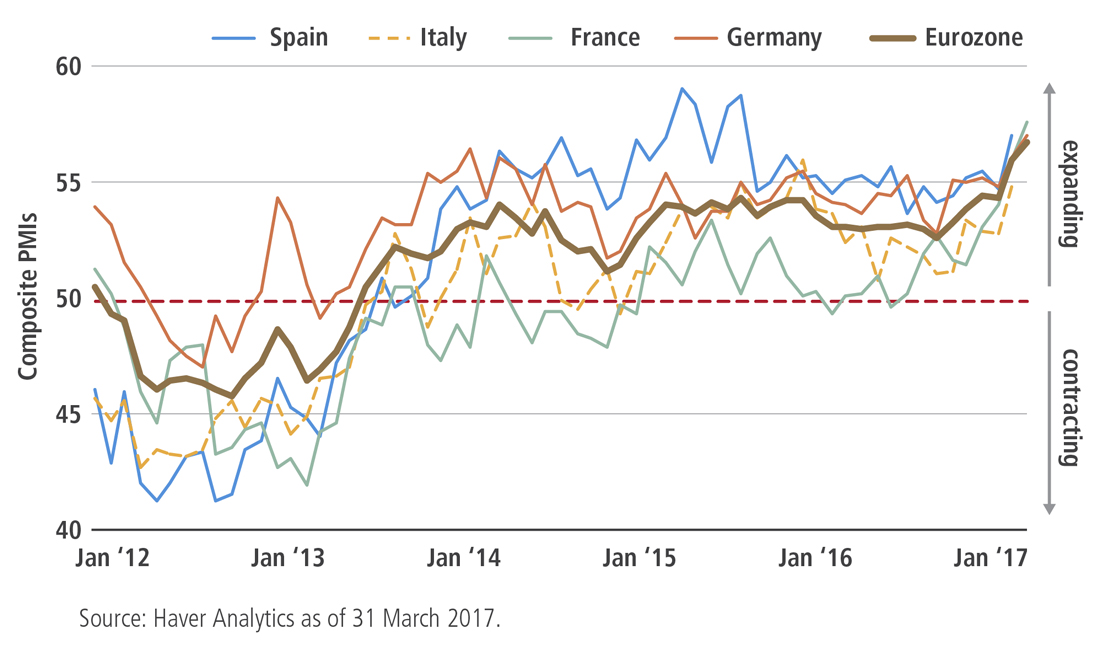

Eurozone growth momentum accelerated in March, underscored by a clear uptick in Eurozone Purchasing Managers’ Indices (PMIs) across various countries. The increase in PMIs was broad based, with all of the underlying components improving. Business activity expectations rose to the highest level since July 2012. Service sector job creation was at the strongest level since October 2007, and factory payrolls improved at a pace not seen since April 2011. Inflows of new work and backlogs both grew at the fastest rates since April 2011, highlighting the strength in eurozone demand. All in all, growth trends were robust despite the uncertainty still persisting amid a busy political calendar.

In the markets

A Continental Divide

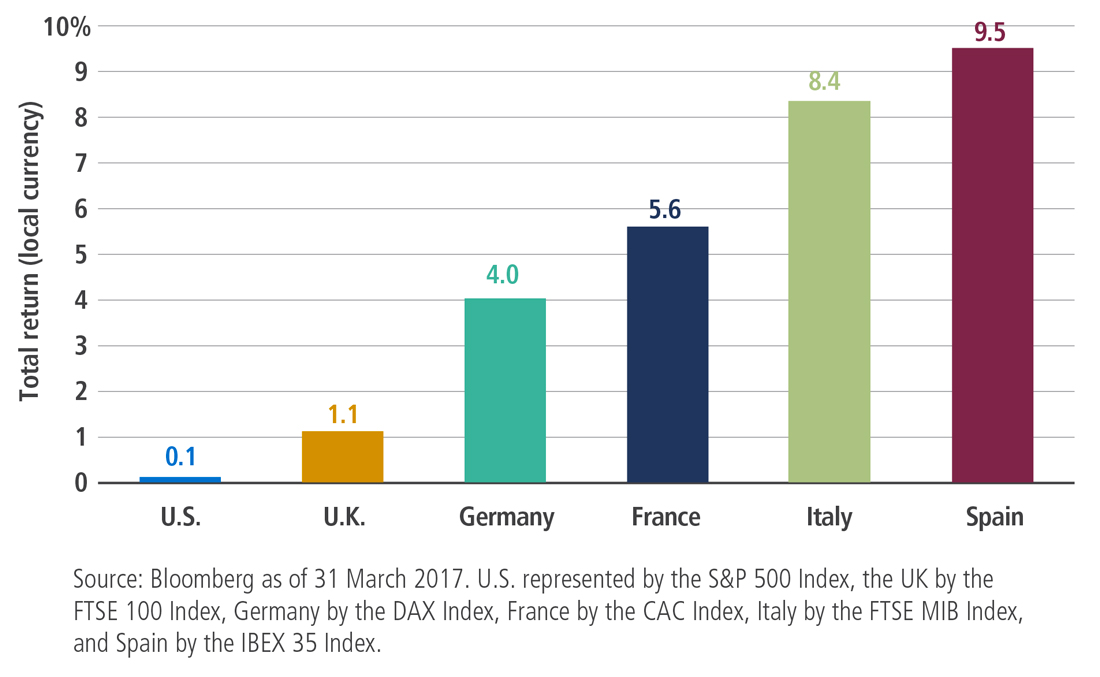

European stocks outperformed their U.S. counterparts in March as political risk in the region subsided somewhat and shifted across the Atlantic. The U.S. “reflation trade” appeared to lose steam as markets reevaluated whether the Trump administration would still be able to deliver on its pro-growth agenda. After the cancelation of the health care vote, the prospects for an overhaul of the U.S. tax code (and subsequent legislation) appeared even more challenging. And in contrast with the political divisions in U.S., the Dutch election outcome suggested some moderation in nationalist/anti-EU sentiment in Europe. This tempering in political risks along with solid growth momentum all contributed to the Continent’s outperformance.

EQUITIES

Developed market stocks1 returned 1.1% during the month, with different results across the major regions. U.S. equities2 ended the month flat, returning 0.1% as investors questioned the ability of the Trump administration to pass pro-growth reform, while stocks in Europe 3 returned a healthy 3.3%, shrugging off near-term political risks in favor of positive economic data. Japanese equities4 fell 0.5% on a stronger yen.In emerging markets

In emerging markets5, stocks benefited from relatively stable global market conditions and a strong technical backdrop, returning 2.5%. Brazilian stocks6 fell 2.5% as commodity prices fell and new and ongoing corruption investigations raised concerns over the government’s ability to pass fiscal and structural reform. Chinese stocks7 fell 0.6% and volatility was muted. Indian equities8 rose 3.2% after an overwhelming victory in state elections by the ruling Bharatiya Janata Party reaffirmed Prime Minister Narendra Modi’s reformist agenda. Russian equities9 fell 2.0% amid a slump in crude oil prices.

DEVELOPED MARKET DEBT

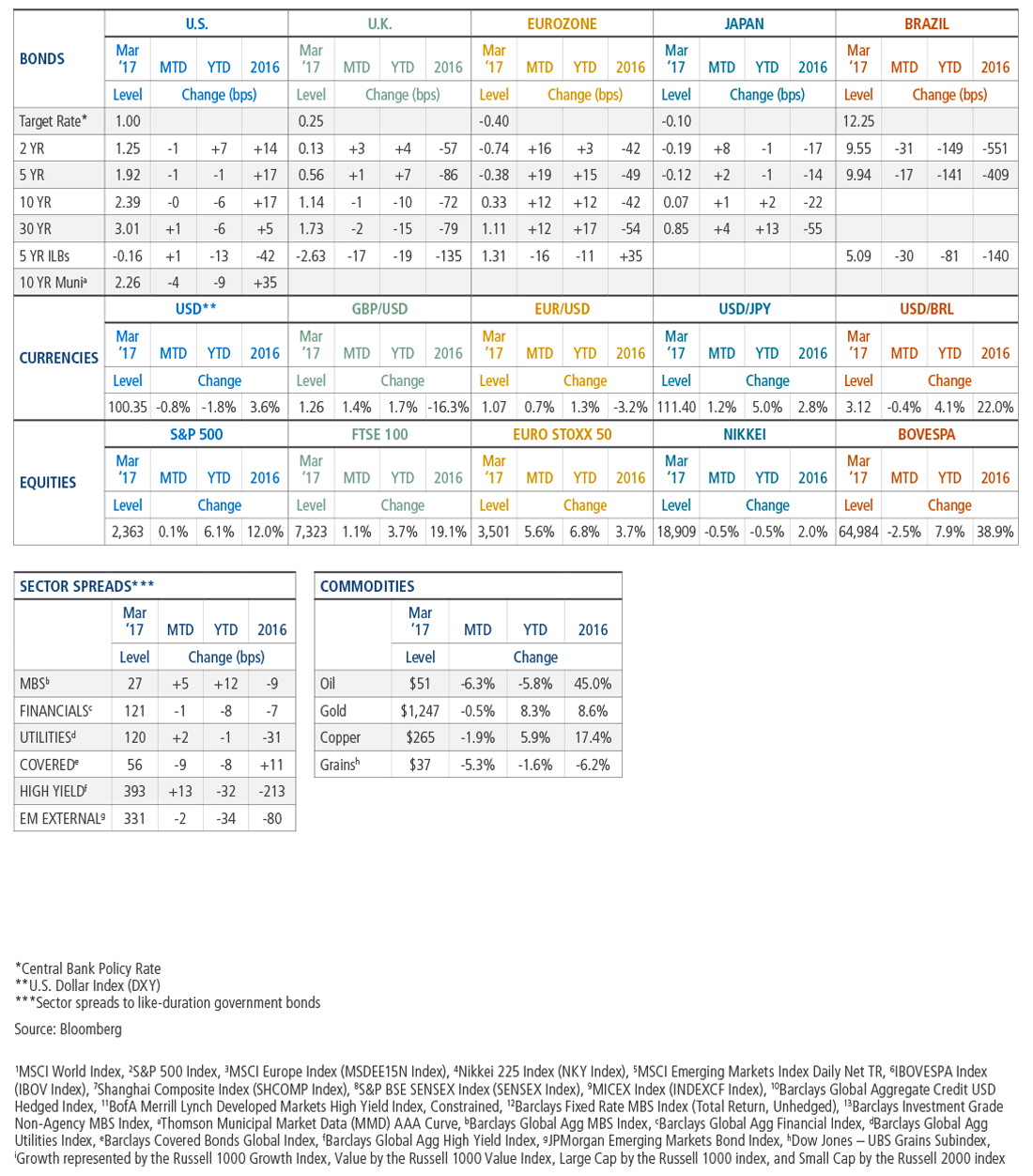

As widely anticipated, the Federal Reserve hiked the U.S. policy rate 25 bps at its March meeting, but the lack of any change to its “blue dots” surprised investors, who had expected that the Fed might signal a faster pace of rate increases. In reaction to the “dovish” hike, U.S. two-year Treasury yields retraced their mid-month move higher to end the month largely unchanged. In Europe, the European Central Bank’s (ECB) upward revision to its inflation forecast, along with encouraging economic data – including a jump in the flash eurozone composite PMI to 56.7 – lifted risk sentiment and sent German 10-year yields 12 bps higher. Concerns over rising populist sentiment eased when the Dutch populist party secured fewer seats in Parliament than expected; French 10-year bond spreads over German bunds tightened 4 bps ahead of France’s election in April.

INFLATION-LINKED DEBT

Global inflation-linked bonds (ILBs) were down modestly in March, underperforming comparable nominal bonds as bullish momentum in breakeven inflation rates waned. In the U.S., Treasury Inflation-Protected Securities (TIPS) and nominal Treasuries moved broadly in line over the course of the month; a strong inflation accrual for TIPS was offset by oil-induced weakness in breakeven inflation rates. U.K. index-linked gilts modestly outperformed their nominal counterparts, posting positive returns overall after better-than-expected retail and consumer inflation figures released mid-month. In Europe, ILBs persistently lagged nominal bonds: Breakeven rates reversed course from February and weakened in response to softer oil markets. Within emerging markets, Brazilian rates rallied and the inflation-expectations curve flattened as the markets perceived the central bank as more dovish.

CREDIT

Global investment grade credit10 returns were mostly flat in March: Overall, spreads tightened 1 bp as global government yields fell. For the quarter, spreads tightened in spite of record supply, due to strong investor demand for high grade retail funds and exchange-traded funds (ETFs) as well as low volatility and improved earnings expectations amid dollar weakness.

Global high yield bond11 prices collapsed but then recovered as U.S. Treasuries rallied, oil prices bottomed out, stocks turned and both supply and outflows subsided. Spreads widened by over 50 bps through mid-month and then compressed by nearly 20 bps by month-end, and the global high yield market returned -0.1% in March.

EMERGING MARKET DEBT

EM debt posted another month of positive returns in March, exhibiting stability in the face of a Fed rate hike and lower commodity prices. Spreads on external debt tightened and index yields on local currency debt fell as investment flows into the asset class continued apace. EM currencies continued to appreciate against the U.S. dollar, showing resilience to weaker crude oil prices, which fell sharply before recouping some losses near the end of the month. The Mexican peso continued to rally when the central bank hiked interest rates for the fourth time since the U.S. presidential election. South African debt and the rand sold off following the surprise removal of the finance minister, which reintroduced political uncertainty ahead of critical reviews by the rating agencies.

MORTGAGE-BACKED SECURITIES

Agency mortgage-backed securities (MBS)12 returned 0.03% and outperformed like-duration Treasuries by 4 bps. Mortgage prices fell significantly early in the month before rebounding mid-month following the dovish interpretation of the Fed meeting. Overall, conventional MBS outperformed Ginnie Mae MBS, 15-year MBS marginally underperformed 30-year MBS, and lower coupon conventional MBS outperformed higher coupon conventional MBS. Supply remained robust, although gross issuance declined slightly and prepayments fell by 19%. Non-agency MBS prices were moderately higher, and their spreads relative to swap rates tightened. Non-agency commercial MBS13 returned -0.06% and underperformed like-duration Treasuries by 10 bps.

MUNICIPAL BONDS

Municipals posted positive returns in March, driven primarily by coupon income. The muni bond yield curve flattened: The front end moved higher after the Fed rate hike while long-end yields were relatively steady. Flows into municipal mutual funds remained positive, and new issue supply picked up modestly.

Puerto Rico’s federal oversight board approved the governor’s fiscal plan that outlines deep haircuts for bondholders, driving the island’s general obligation securities to record lows. Hospital bonds outperformed as congressional attempts to repeal the Affordable Care Act (ACA) failed. Looking forward, investors awaited clarity on the potential for tax reform and infrastructure spending, but the likelihood of sweeping policy changes appeared low.

CURRENCIES

The “dovish” rate hike from the Fed and the failure of the U.S. healthcare reform bill in Congress pushed down the U.S. dollar against most currencies in March. The stalled healthcare reform effort cast doubt on the widely anticipated fiscal expansion that has fueled dollar strength since the U.S. election. The British pound ended the month as the best performer in the G10 basket despite elevated volatility during numerous revisions to the Article 50 bill in Parliament ahead of the formal Brexit trigger later in the month. (For details, see this month’s "In Sight".) In Europe, the electoral defeat of the populist party in the Netherlands and sagging polling numbers for far-right presidential candidate Marine Le Pen in France boosted the euro. A narrower bond yield differential between Japan and the U.S. helped strengthen the Japanese yen. In emerging markets, the South African rand fell more than 2% following the surprise removal of the finance minister.

COMMODITIES

Commodity prices broadly slumped in March, and returns ended in negative territory across sectors. Oil prices weighed on returns in the energy sector, with prices dipping lower in response to record-high U.S. inventories and new doubts about OPEC’s commitment to production cuts. In contrast, natural gas rallied amid support from colder weather. Within the agriculture sector, sugar prices dropped sharply on the prospect of more Brazilian supplies and waning enthusiasm for India’s plan to waive its import tax temporarily. Gold prices fell sharply on rising rate fears early in the month before recovering in the wake of the Fed meeting, where Chair Janet Yellen reiterated the Fed’s intent to only gradually remove accommodation. Nickel was the laggard within base metals, while aluminum prices ended the month up slightly.

Outlook

PIMCO expects the nearly eight-year-old global economic expansion will strengthen and broaden over the coming year, driving global GDP growth to 2.75%–3.25% from 2.6% in 2016 and boosting CPI inflation to 2.25%–2.75%. Our outlook reflects several positive factors: generally supportive fiscal policies (or expectations of them) in most developed market economies and easier financial conditions since the start of the year, along with more positive animal spirits (as indicated by consumer and business confidence data) and a rebound in global trade in recent months.

In the U.S., we see growth above-trend at 2%‒2.5% in 2017 as business investment recovers, particularly in the energy sector, and consumer spending is supported by a further decline in unemployment, higher consumer confidence and expectations of personal income tax cuts in 2018. We forecast core inflation to hover sideways this year at 2.0%–2.5%, but expect that the Fed will feel encouraged by above-trend growth to raise interest rates two more times during 2017, on top of the March rate hike.

For the eurozone, we now expect growth will rise to a range of 1.5%‒2.0% in 2017, revised higher from our forecast in December to reflect the stronger momentum into this year. While political uncertainty remains elevated ahead of crucial elections in France, Germany and potentially Italy, both fiscal policy and monetary policy are expansionary, and the recovery in global trade growth supports exports and investment. We anticipate core inflation at just below 1%, making little headway toward the ECB’s “below but close to 2%” objective. We also expect the ECB to continue buying bonds at the recently announced reduced pace of €60 billion per month through December 2017, before tapering and eventually ending its purchases from early next year.

In the U.K., we expect growth to stay in the range of 1.75%–2.25%(above market consensus) despite Brexit, reflecting robust momentum, higher government spending and a positive contribution from net trade on the back of the 15% drop in the pound in 2016. We forecast CPI inflation to exceed the Bank of England’s 2% target but expect that the bank will keep policy rates unchanged this year.

Japan’s fiscal stimulus and a weaker yen should propel GDP growth to 0.75%‒1.25% in 2017 while inflation remains significantly below the 2% target. The Bank of Japan is likely to keep targeting the overnight rate at -0.1% and the 10-year bond yield at 0% and thus continue its standing invitation to the government to engage in additional fiscal expansion, which we expect to happen later this year.

China’s public sector credit bubble and private sector capital outflows will likely remain under control, and we expect growth to slow to a 6%‒6.5% band in 2017 as policymakers prioritize financial stability over economic stimulus ahead of the 19th National Party Congress in the fourth quarter. Any trade war with the U.S. will likely involve words rather than action, and we expect the yuan to depreciate gradually by 4%–5% against the U.S. dollar.

In emerging markets, we expect moderate growth will return to Brazil and Russia as their deep recessions end. With inflation dropping, both countries’ central banks could cut rates multiple times. Mexico’s Banxico is expected to tighten policy further, following the Fed’s lead, and growth should slow to 1.25%‒1.75% as a result.

In sight

You only leave once

UK Prime Minister Theresa May formally triggered the country’s departure from the European Union with a letter to the president of the European Council in late March, expressing a desire for the UK to remain a close ally while restoring “national self-determination.”

Some big issues remain in question, however. The UK expects to work out any new trading arrangements concurrent with negotiations over its exit bill, while the EU maintains that the exit bill should be settled first. Neither side appears willing to offer early room for compromise, and time is already short. Although the full negotiating period is two years, if there is no clarity after one year, businesses will likely assume a reversion to World Trade Organization (WTO) trade rules and start to enact plans accordingly. Given imminent French and German elections, the crucial negotiating period will be late 2017 and early 2018. With this limited time frame and little indication of compromise so far, the likelihood of a “hard Brexit” is high.

During negotiations, the pound sterling is likely to remain the most sensitive asset, while 10-year UK gilt yields already encapsulate at- or below-trend growth for several years.

Appendix

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk and liquidity risk. The value of most bonds and bond strategies is impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax; a strategy concentrating in a single or limited number of states is subject to greater risk of adverse economic conditions and regulatory changes. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation- Protected Securities (TIPS) are ILBs issued by the U.S. government. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

©2017, PIMCO.

CMR2017-0411-262067

© PIMCO

Read more commentaries by PIMCO