SUMMARY

- Think of the increases in the fed funds rate not as the beginning of an interest rate tightening cycle, but as the beginning of a process to remove a substantial amount of monetary policy accommodation.

- This “removal of accommodation” cycle still has a ways to go. The real (inflation-adjusted) effective fed funds rate is still negative, and accommodative, and likely will remain so until the nominal rate reaches 2%. The Fed’s latest dot plot suggests that won’t happen until year-end 2018.

- At least three challenges could complicate the Fed’s efforts to remove accommodation. First, crucial details on how the Fed will shrink its $4.5 trillion balance sheet remain unresolved. Second, policymakers face the ever-present threat of a financial, political or geopolitical event somewhere in the world that disrupts trade flows, risk appetite, financial markets and exchange rates. Third, the composition of the Fed Board of Governors is likely to change significantly by next year.

It’s now officially a “rate hike cycle,” said the pundits after the Federal Reserve’s March increase in the federal funds rate – the second hike in three months, and the third overall since December 2015 (which was the first increase in the policy rate in nine and a half years!). Whatever the talking heads may call it, it is more useful for investors to think of these increases in the fed funds rate not as the beginning of an interest rate tightening cycle in the U.S., but rather as the beginning of a process to remove what is at present ‒ and will for some time continue to be ‒ a substantial amount of monetary policy accommodation sloshing through the global financial system.

The extent of that accommodation can be quantified in a few ways. In the U.S., the effective federal funds rate (a nominal interest rate), at roughly 0.9% following the March hike, still falls well short of the Fed’s preferred measure of inflation (Personal Consumption Expenditures or PCE), which is running at a headline rate of 1.9%. In other words, the real (inflation-adjusted) effective fed funds rate remains negative, and accommodative. Fed officials appear to be in broad agreement that r*, the equilibrium (neither accommodative nor restrictive) neutral real policy rate consistent with full employment and the Fed’s 2% PCE inflation target, is at present around 0%. (At PIMCO, we recognized early on that the neutral rate had moved lower than its historical average; we introduced this concept of The New Neutral in 2014.) This 0% rate for r* would imply that the (nominal) fed funds policy rate will remain – by definition – “accommodative” until it reaches 2%.

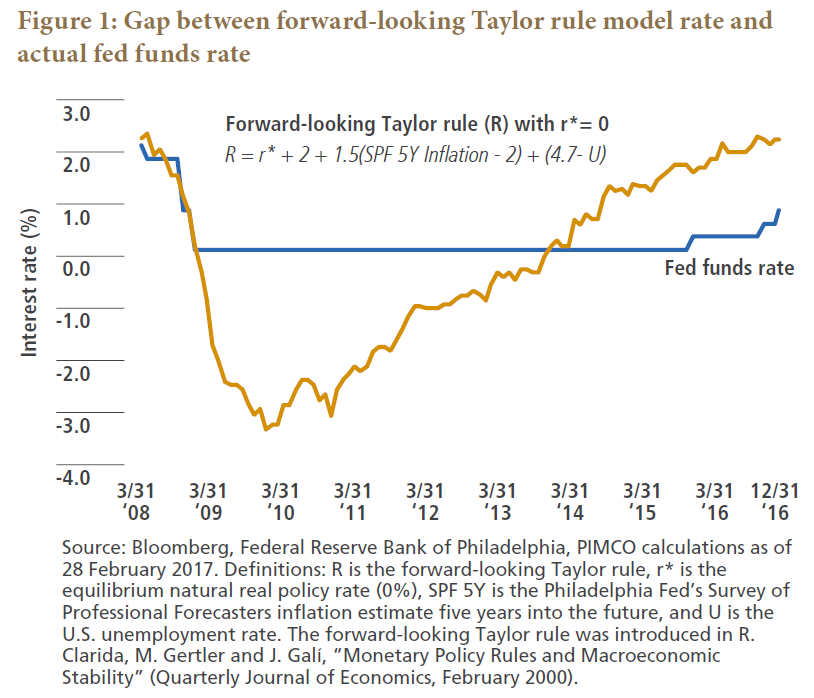

The forward-looking Taylor rule illustrates this concept – see Figure 1. The Taylor rule is an interest rate forecasting model that helps guide how a central bank policy rate should respond to actual versus targeted levels of inflation and unemployment; a forward-looking Taylor rule is one variation that emphasizes longer-term inflation forecasts and tends to imply a slower, more gradual tightening process. Still, with r* at 0%, the theoretical forward-looking Taylor rule policy rate remains well above the actual fed funds policy rate (even after the so-called rate hike cycle has begun) – and the gap between them is accommodation.

And when might the policy rate reach 2%? The Fed, via the median of the projections depicted in the most recent dot plot, doesn’t forecast getting the fed funds rate to 2% until year-end 2018. So this “removal of accommodation” cycle – which I admit is a mouthful of nine syllables, so how about calling it “ROA” instead – still has a ways to go. Initial market reaction to the policy rate hikes – with stocks higher, credit spreads tighter and the dollar weaker – was consistent with this interpretation that the Fed intends a gradual path toward normalization. Call it a dovish ROA.