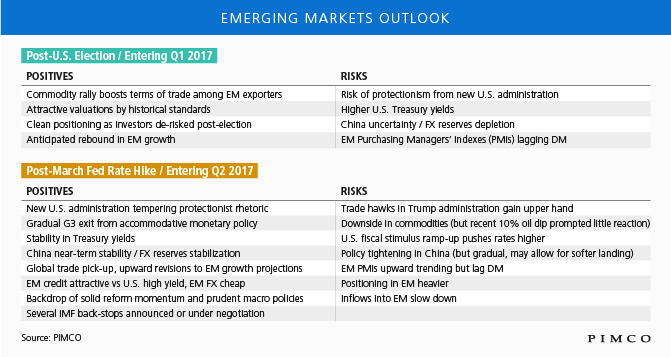

As 2017 progresses and the priorities of the Trump administration take shape, the outlook for emerging markets (EM) has evolved from uncertain to promising.

What has changed so quickly? Several important concerns that weighed on the sector since late last year have subsided, allowing the relatively strong fundamentals in many EM countries to shine and driving an impressive recovery in EM bonds.

Initially, emerging market assets bore the brunt of investors’ fear of protectionist policies after the U.S. election. Now, as the new administration sets its agenda, developed markets (DM) are once again at the epicenter of global worries. Investors are wondering about the likelihood and size of U.S. fiscal stimulus and/or tax cuts. Europe faces a number of imminent political tests: French presidential elections in late April/early May and parliamentary elections in June, German elections in September, Italian elections likely sometime in 2017, and ongoing negotiations over Brexit. Topping that off is uncertainty over the $6 billion in Greek bonds coming due in July.

The Fed factor

Investors were also concerned about the pace of interest rate rises from the Federal Reserve and the impact on EM capital flows. Now, the markets have calmly priced in expectations for three Fed hikes in 2017, including the recent March increase.

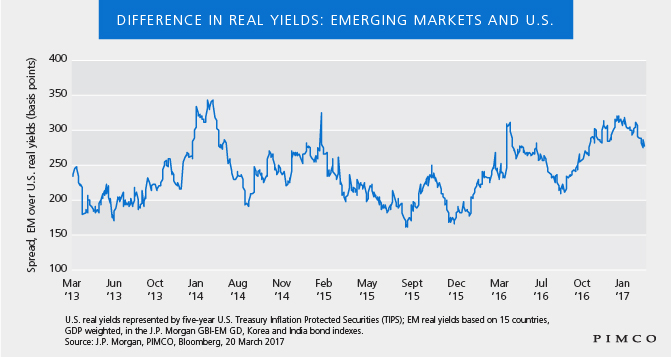

Should the Fed shift to a more hawkish bias next year – and should 10-year U.S. Treasury yields resume their climb – we do not anticipate a material reaction in EM fixed income for several reasons. First, the EM balance-of-payments adjusted (by way of a significant decline in currencies) after the 2013 “taper tantrum,” which served as a dress rehearsal for higher U.S. interest rates. Second, many investors reduced positions in rate-sensitive long-term bonds and shifted to a defensive stance on duration in the second half of 2016, when U.S. yields rose 100 basis points. And finally, EM debt is likely to be less sensitive to higher rates in developed markets given the yawning differential in real rates (see chart), a stark contrast to the “taper tantrum” era. Going forward, we expect DM real yields to be capped by low potential growth and persistently high debt burdens.

Different story in commodities

Finally, the fear that lower commodity prices could hurt EM exporters was diffused when the March dip in oil prices caused merely a hiccup in EM debt markets. We believe the reaction (or lack thereof) has to do with the cause of the sell-off: Unlike 2014–2015, when a commodity price plunge was led by demand destruction, the recent downward pressure on oil prices was prompted by a mild supply shock. Should oil prices fall further, the extent of the sell-off is expected to be contained by solid world demand, especially as global growth improves.