Next month, more than 1,000 bonds worth over $300 billion will vanish from the Bloomberg Barclays U.S. Aggregate Index.

Their disappearance reflects market dynamics that tend to benefit active fixed income managers with robust research processes while putting passive investment managers at a disadvantage.

Passive managers who track the bond benchmark will have to sell these bonds when the issuer disappears from the benchmark – even though their fundamental value may not immediately change. Selling, of course, tends to depress prices. And this can create opportunities for active investment managers to potentially buy at more attractive prices.

These securities will exit the index because of a rule change: From 1 April 2017, Treasury, government-related and corporate bonds will need a minimum outstanding market value of $300 million, up from $250 million, to be included in the index. The fundamental value of these bonds may not change, but passive, rules-based investors will be forced to sell without regard to fundamentals.

Index ins and outs

A similar scenario unfolded about a year ago when plunging prices for oil and other commodities prompted ratings agencies to downgrade to junk more than $100 billion worth of bonds issued by natural resource producers.

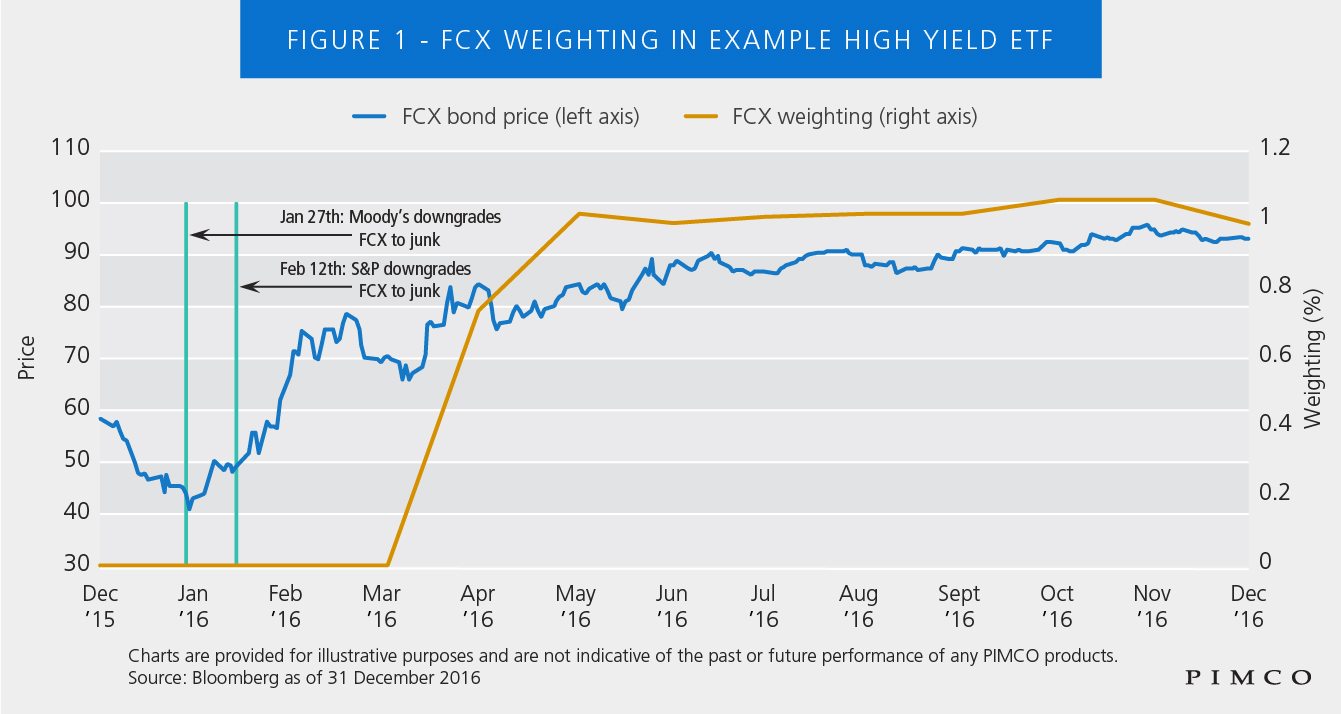

Bonds of copper mining giant Freeport-McMoRan Inc. (FCX), for instance, were downgraded to junk in January and February of 2016. The bonds quickly recovered, and became nearly 1% of the high yield market.

Passive bond managers lost out – twice. Investment grade indexers had to sell. And by way of example, it took a few months for a leading passive high yield ETF to accumulate enough bonds to fully replicate the bonds’ representation in the market-capitalization-weighted high yield index it tracked. The example ETF needed until the end of April to fully build its position in Freeport’s bonds – by which time the securities had more than doubled in price from the lows touched after Moody’s downgrade (see Figure 1).

Independent ratings

Changes in index composition represent a source of alpha potential for active managers. It’s a further reason why we see value in a robust bottom-up and top-down research process.

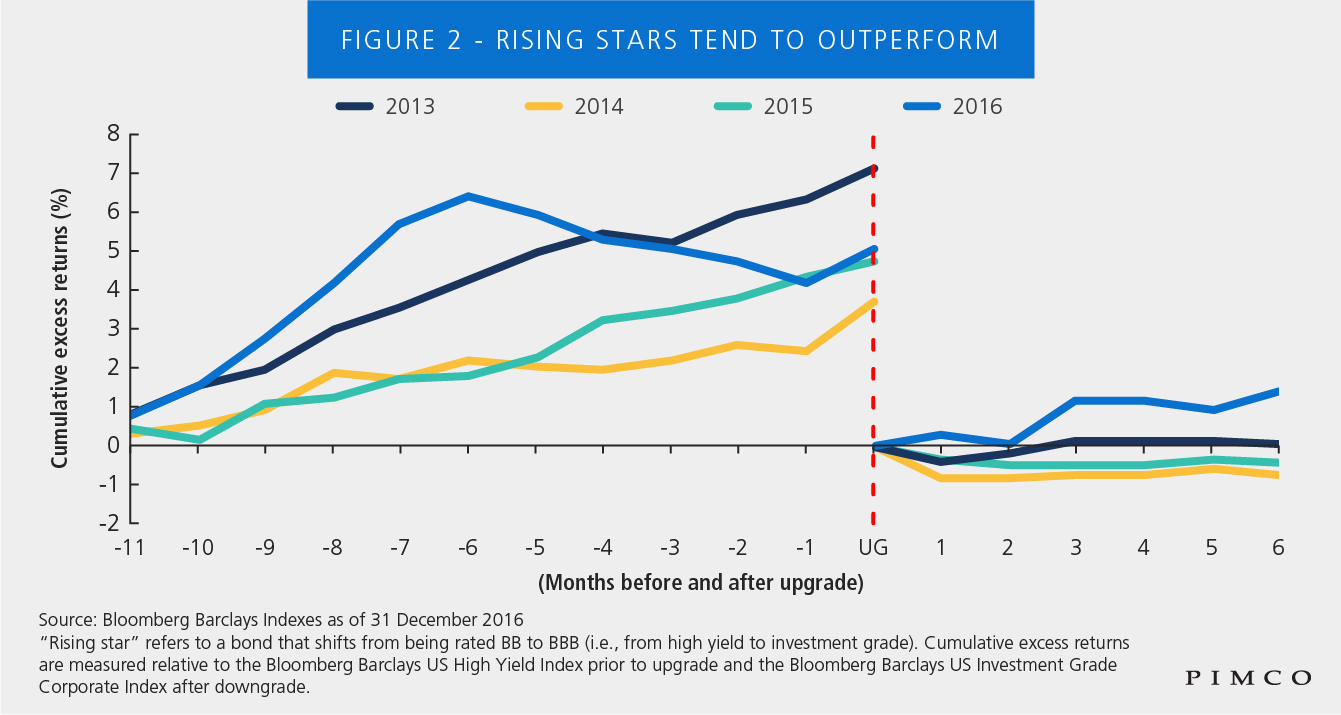

A major goal of research is the identification of rising stars (bonds whose ratings may increase to investment grade) and fallen angels (investment grade bonds whose ratings may fall to high yield). By correctly anticipating changes in major agencies’ ratings, active managers have the potential to benefit.

Research by Bloomberg Barclays Indices, in fact, shows that rising stars tend to appreciate several months before a ratings increase – gains that can elude passive managers (see Figure 2). Conversely, prices of “fallen angels” tend to fall well before the ratings-agency downgrade occurs, and they tend to continue to fall as passive managers sell bonds they are no longer permitted, for index-related reasons, to hold. These are losses active managers can potentially avoid.

Bonds are different

Alas, despite its potential benefits, equity research remains far more common than credit research, for which building large teams presents significant challenges.

The scale of the bond market is a major reason. PIMCO tracks over 44,000 issues in credit markets – including high yield, investment grade, bank loans, emerging market sovereigns, municipals and securitized bonds. At the end of 2016, in contrast, the MSCI All Country World Index listed 14,447 equities, covering 99% of the global equity opportunity set.

Ratings agencies may provide the broadest coverage of fixed income securities, but their credit reports are designed chiefly to assess relative risk, not to inform investment decisions. Moreover, agencies have tended to adopt mechanistic, rules-based methodologies. These may enhance consistency and transparency, but they often fall short in projecting risks that may be critical to bond investors.

This helps explain why about 60% of PIMCO’s independent ratings differed from the average of ratings issued by major ratings agencies at the end of 2016.

PIMCO had more than 50 credit analysts around the world at the end of last year. They research industries, meet company management, perform relative-value analysis and create detailed, company-specific assessments filtered through the lens of our macroeconomic forecasts.

Next month, when passive index investment managers become forced sellers of more than 1,000 bonds worth over $300 billion, active managers will be ready.

Christian Stracke is global head of credit research at PIMCO.

DISCLOSURES

References to specific securities and their issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold such securities. PIMCO products and strategies may or may not include the securities referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

Management risk is the risk that the investment techniques and risk analyses applied by the active investment manager will not produce the desired results, and that certain policies or developments may affect the investment techniques available to investment manager in connection with managing the strategy. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. All investments contain risk and may lose value. Investors should consult their investment professional prior to making an investment decision.

© PIMCO

© PIMCO

Read more commentaries by PIMCO