Floating Rate Nature of Bank Loans

The floating rate coupons offered by bank loans are based on a yield spread over Libor, and they adjust every one to three months. It is important to know that the majority of bank loans outstanding have Libor “floors,” so the coupon only begins to increase once Libor exceeds a minimum “floor” rate (on average, this floor rate is 1%). Given Libor’s low level today, bank loans may not provide a significant increase in income relative to high yield bonds, but they may provide limited downside when bond prices fall and meaningful upside once Libor exceeds floor rates. This is why the loan market has historically exhibited strong performance during periods of rising rates.

Leveraging the opportunity

Given the strong performance across fixed income markets in 2016 to date, investors seeking to enhance returns are faced with a dilemma: Are they best served by going down in credit quality, moving down the liquidity spectrum to capture “liquidity premiums,” or adding moderate levels of leverage?

While PIMCO believes there are meaningful benefits to moving down the liquidity spectrum into opportunistic assets, such as real estate and credit-related opportunities, many investors are unwilling to sacrifice meaningful amounts of liquidity. From this perspective, a moderately leveraged approach to bank loans can present an attractive option. With the benefits of structural seniority, limited interest rate risk and attractive financing levels, modestly leveraged bank loan strategies have the potential to help achieve attractive yields in the current environment, without sacrificing a material amount of liquidity or significantly increasing volatility.

At current levels, financing costs to apply leverage to high quality bank loans are historically low. While there are several ways to apply leverage to bank loans, total return swaps can be cost effective and efficient, and also allow active managers to hand-pick credits and selectively tailor leverage to match the individual credit risk of each bank loan. (For context, current costs on total return swaps on bank loans are roughly Libor plus 100 bps‒125 bps.) We believe the most prudent approach includes the flexibility to actively manage exposure between bank loans and high yield bonds, overall leverage levels and security selection within the bank loan and high yield market.

Our approach is typically to lever higher-quality, lower-volatility bank loans that can mitigate mark-to-market volatility during risk-off market environments and reduce the risk of loss when default rates increase across corporate credit assets. It should also be noted that these moderately leveraged portfolios are generally not compatible with daily liquidity portfolios, and typically work best within a monthly liquidity format.

Where can a leveraged bank loan strategy fit in a portfolio?

Leveraged bank loan strategies can play a variety of roles in a portfolio:

-

Return enhancement versus traditional bank loans. Given low absolute yield levels across credit markets, applying leverage to select, higher-quality bank loans can provide a potential boost to returns over traditional bank loan strategies, without applying leverage to an entire bank loan portfolio.

-

De-risking tool versus equities. As many investors reduce their return expectations for equities, credit can provide an attractive alternative with lower volatility. Leveraged bank loans can help produce attractive yield potential, while keeping volatility well below that of traditional equity indexes.

-

Substitute for CLO (collateralized loan obligation) debt.Demand for CLO debt has been robust in recent years even amid historically high issuance. While the CLO may be the most well-known type of leveraged loan portfolio and can offer attractive returns over time, there may be drawbacks for more liquidity-constrained investors, including lack of liquidity in the secondary market, price volatility based on weak secondary market technicals and a long lock-up of capital.

-

Alternative to high yield bonds. Leveraged bank loans can be a compelling complement to or substitute for high yield bonds, specifically short-dated high yield bonds. Applying moderate leverage to a senior secured asset can potentially provide similar returns, with superior downside cushion in weaker credit market environments.

The risks in leveraged bank loans

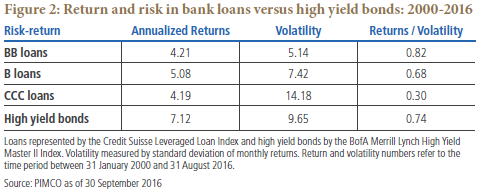

While bank loans can provide a greater cushion within the leveraged credit universe, the bank loan sector in general can be volatile at times and has had cycles of aggressive underwriting. Applying moderate leverage to the sector can potentially enhance returns during periods of low volatility, but it can magnify downside risks during periods of elevated volatility or defaults (see Figure 2). Against this backdrop, in our view, active management of leverage, security selection and overall credit exposure is critical to navigating full market cycles.

Moderate leverage in bank loans: a credit tool

As many investors struggle to achieve their return targets in the current environment, tools for enhancing returns often include moving out on the liquidity spectrum and going down in credit quality. Moderately leveraged bank loan strategies can allow investors to maintain a fair degree of liquidity and improve return potential without going down in credit quality. In addition, their senior secured nature and floating rate coupon structures mean bank loans can potentially offer a downside cushion to a bond portfolio in weaker credit environments and rising interest rate environments. Applying leverage entails risk, but it can serve as a useful tool when applied prudently to higher-quality credits.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Bank loans are often less liquid than other types of debt instruments and general market and financial conditions may affect the prepayment of bank loans, as such the prepayments cannot be predicted with accuracy. There is no assurance that the liquidation of any collateral from a secured bank loan would satisfy the borrower’s obligation, or that such collateral could be liquidated. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Collateralized Loan Obligations (CLOs) may involve a high degree of risk and are intended for sale to qualified investors only. Investors may lose some or all of the investment and there may be periods where no cash flow distributions are received. CLOs are exposed to risks such as credit, default, liquidity, management, volatility, interest rate and credit risk. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

The Credit Suisse Leveraged Loan Index is designed to mirror the investable universe of the $U.S.-denominated leveraged loan market. The index inception is January 1992. The index frequency is monthly. New loans are added to the index on their issuance date if they qualify according to the following criteria: Loans must be rated “5B” or lower; only funded term loans are included; the tenor must be at least one year; and the Issuers must be domiciled in developed countries (Issuers from developing countries are excluded). Fallen angels are added to the index subject to the new loan criteria. The BofA Merrill Lynch High Yield Master II Index is an unmanaged index consisting of U.S. dollar denominated bonds that are rated BB1/BB+ or lower, but not currently in default.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. It is not possible to invest directly in an unmanaged index. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

©2016, PIMCO.

© PIMCO

Read more commentaries by PIMCO