SUMMARY

- The ghost of the infamous “taper tantrum” of 2013 haunted markets in October as rates increased across much of the developed world.

- The global economy continued to muddle along as inflation pressures built.

- Higher interest rates, a stronger dollar and heightened election uncertainty combined to spook markets.

The ghost of the infamous “taper tantrum” of 2013 haunted markets in October as rates increased across much of the developed world. Sovereign yields moved higher globally in a marked departure from the declining trend prevalent for much of the year. Firming inflation data along with concerns about the longevity of central bank support pressured rates higher.

The global economy continued to muddle along as inflation pressures built. Preliminary GDP growth estimates for the U.S. showed a revival from softer growth in the first half of the year, though some underlying trends tempered optimism. Still, solid growth and employment figures coupled with firming inflation data helped inflation expectations move higher.

Higher interest rates, a stronger dollar and heightened election uncertainty combined to spook markets. Rates rose and the dollar strengthened, while risk assets broadly were mixed as indications of a tighter U.S. presidential race weighed on risk sentiment toward the end of the month.

TWIST OF FATE

After falling for much of the year, long-term rates across major developed markets seemed to bottom at the end of Q3 and then moved higher in October. Rising inflation expectations on the back of solid growth trends in the U.S. contributed to higher yields, as did the growing perception that seemingly endless central bank support may not actually be permanent: Fed minutes indicated the FOMC may be keen to raise rates later this year, the BOJ acknowledged the potentially detrimental effects of excessive yield curve flattening, and rumors circulated that the ECB may taper its bond purchases. All in all, it was a remarkable twist of fate that central banks contributed to rates moving higher just months after helping drive them to all-time record lows.

The ghost of the infamous “taper tantrum” of 2013 haunted markets in October as rates increased across much of the developed world.

Sovereign yields moved higher through the month, marking a reversal from the trend evident for much of the year. In the U.S., rates rose the most since February 2015 and the second most since the tantrum. Firming inflation and inflation expectations, along with growing anxiety about a tilt away from central bank accommodation, contributed to the move higher in rates. All three major central banks added to market jitters about the longevity of policy support. The Federal Reserve minutes released during the month indicated higher rates were warranted “fairly soon,” and the market-implied probability of a rate hike in December crept upward from 59% to 71%. Across the Atlantic, the European Central Bank (ECB) kept policy largely unchanged, but rumors of potential tapering pressured yields higher, even after President Draghi sought to dismiss those concerns. Even the Bank of Japan (BOJ) ‒ a month after adjusting its policy framework towardyield curve targeting ‒ added to the mix by suggesting that the current pace of Japanese government bond purchases may not be necessary in the future and “excessive flattening” of yield curves was not desirable. Ultimately, central banks appeared to be confronting the limitations of extended monetary policy support even as investors grew wary about what those tweaks could mean for a market clearly reliant on it.

The global economy continued to muddle along as inflation pressures built. The U.S. expanded at a rate of 2.9% during the third quarter, making up for below-trend growth in the first half of the year. However, a meaningful miss in underlying consumption tempered the encouraging headline number. The GDP improvement, along with sound job gains and Fed chair Janet Yellen’s comments that running a “high pressure economy” may be appropriate, helped drive rising inflation expectations in the U.S. An even sharper jump occurred in U.K. breakeven inflation rates, driven by further weakening in the British pound amid divisive rhetoric between U.K. and EU leaders about the impending Brexit negotiations. China concerns abated somewhat as GDP held steady at an annual rate of 6.7%. Elsewhere in emerging markets, a flurry of activity made global headlines: Saudi Arabia unveiled the largest-ever debt sale by a developing country with a $17.5 billion bond offering, an effort to lessen its dependence on oil revenues; a peace deal with Colombia’s largest rebel group was unexpectedly struck down in an outcome reminiscent of the surprise Brexit victory; and the King of Thailand’s death incited investor concern over the country’s political stability.

Higher interest rates, a stronger dollar and heightened election uncertainty combined to spook markets. Firming inflation expectations and rising odds of a December rate hike in the U.S. drove rates and the U.S. dollar higher. Globally, rates also moved higher, bouncing the most in the UK, where 10-year yields rose 50 bps on inflation concerns from a weaker pound. Though it recovered from a brief “flash crash” on 7 October, the pound still fell more than 5% in October to become the worst-performing developed market currency. Risk assets were mixed as indications of a tighter U.S. presidential race weighed on risk sentiment toward the end of the month. While U.S. equity markets were slightly down on the month, growth in Q3 earnings provided a bright spot relative to the past four quarters. But with the political calendar adding uncertainty and central banks less able to dampen shocks, investors were left to wonder if the developing concerns were more than just an apparition.

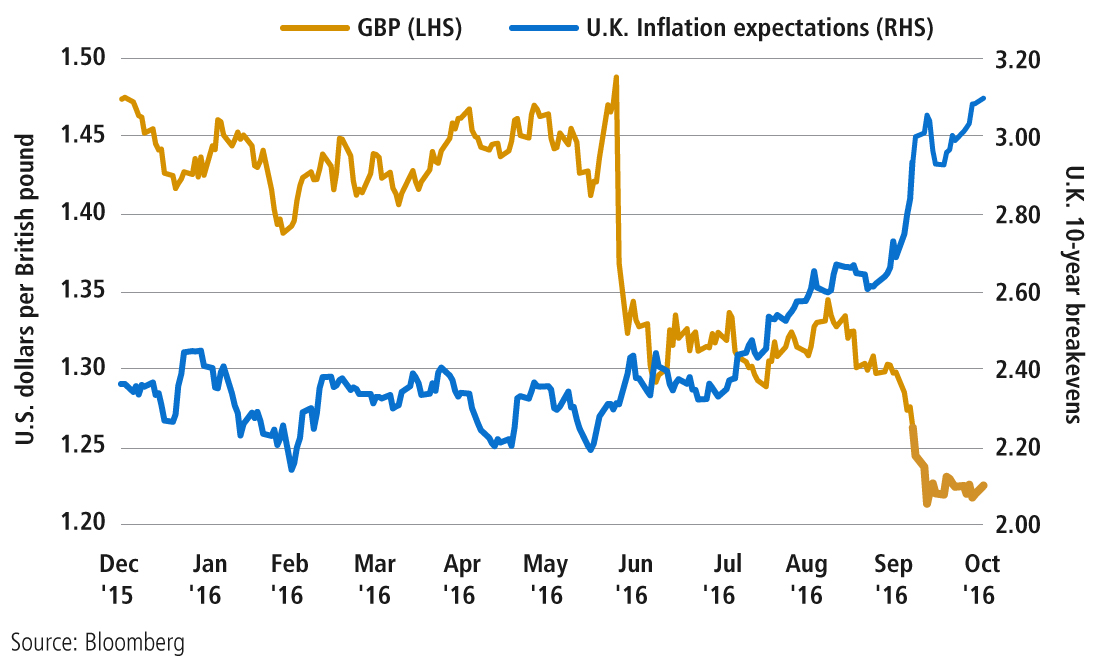

DROP IN POUND(S) WEIGHS ON BOE

As Asian markets opened amid thin liquidity on 6 October, the pound sterling plummeted during two minutes of chaotic trading, briefly touching its lowest level against the U.S. dollar in more than 30 years. October’s “flash crash” underscored a challenging year for the pound, which remains the world’s worst performing major currency against the dollar. Its steady decline since June’s “Brexit” referendum has precipitated a pick-up in inflation expectations to more than 3%, as a weaker currency makes imports more expensive. Bank of England Governor Mark Carney has said he will “undoubtedly” consider the pound’s depreciation as the committee meets next month, suggesting that it may temper the bank’s ability to ease policy further.

EQUITIES

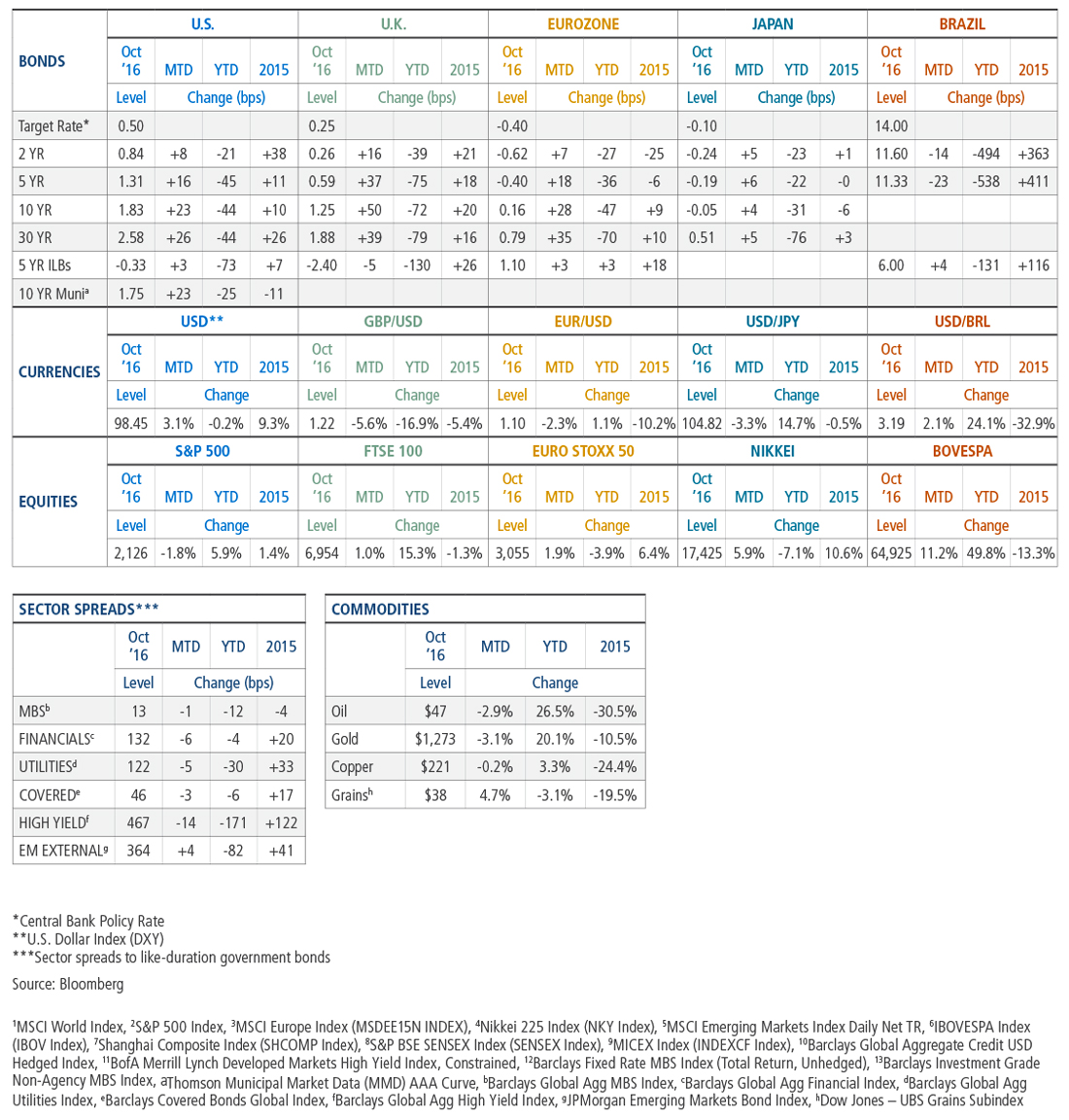

Developed market equities1 fell -1.9% during the month as a stronger U.S. dollar weighed on returns outside the U.S., and election uncertainty caused U.S. equities2 to post their worst monthly return (-1.8%) since January. Stocks in Europe3 ended the month down, returning -0.8% after a challenging start to the earnings season. Japanese equities4, buoyed by a weaker yen, continued to rally into the fourth quarter, hitting a six-month high and returning 5.9%.

In emerging markets5, stocks ended the month in slightly positive territory, returning 0.2%. In Brazil, stocks6 climbed to a four-year high, returning 11.2% amid strength in cyclicals and monetary easing by the Central Bank of Brazil. Chinese equities7 gained 3.2% while Indian equities8 rose 0.3% amid mixed corporate earnings. In Russia, losses from lower oil prices were offset by optimism around multi-billion-dollar deals struck with India in both the energy and defense sectors, and equities9 advanced 0.8%.

DEVELOPED MARKET DEBT

Developed market yields across the curve jumped higher, reversing this year’s flattening trend with inflation expectations rising and the odds growing of monetary policy divergence between the Fed and the rest of the developed world. In the U.S., the Fed continued to signal a desire to tighten policy before the end of the year and market-implied probabilities of a December hike rose north of 70%. In response, 10-year yields rose 23 bps, widening the differential over two-year yields by 15 bps and steepening the yield curve. Yields globally followed suit, with the largest move in the UK, where the yield on the 10-year gilt soared 50 bps as a weaker pound stoked inflation concerns.

INFLATION-LINKED DEBT

Global inflation-linked bonds (ILBs) declined across most markets in October, as global interest rates ascended. ILBs generally fared well relative to their nominal counterparts, as inflation expectations continued to gain upward momentum. U.S. TIPS notably outperformed comparable U.S. Treasuries for the month. Breakeven inflation (BEI) rates in the U.S. rallied sharply on an early-month bounce in energy prices, a higher-than-expected headline CPI reading and strong retail inflows. In the UK, index-linked gilts continued to outpace nominal gilts by a wide margin as the pound fell further, and pension fund flows helped push 30-year BEI to the widest level since early 2014. In Europe, core-country ILBs outpaced those from the periphery, and breakeven rates drifted higher across countries.

CREDIT

Global investment grade (IG) credit spreads10 tightened 4 bps in October as global government bond yields rose. Global IG credit posted a total return of -0.8% in October, bringing total returns to +7.2% year-to-date given the overall strong demand for stable income.

Global high-yield bond yields11 declined to a 16-month low in October and then rose amid weaker oil prices, renewed ETF outflows and the general climb in government bond yields. Spreads compressed by 13 bps as the increase in government rates outpaced the slight uptick in speculative grade bond yields. Global high yield bonds experienced their ninth consecutive month of positive total returns and gained 0.4%.

EMERGING MARKET DEBT

EM debt assets cooled off in October and posted negative returns as developed market yields moved higher and commodity prices fell. Spreads over U.S. Treasuries for external debt widened, EM local yields rose and currencies generally weakened against the U.S. dollar. In Latin America, an unexpected rejection by voters of Colombia’s landmark peace deal caused the country’s external and local debt to underperform, while in Brazil, inflation continued to moderate, allowing the central bank to deliver a much-anticipated rate cut. Across the EM universe, oil exporters generally underperformed as doubts arose concerning the previously announced OPEC production cut agreement. Of note, Saudi Arabia came to the bond market amid overwhelming investor interest, underscoring continued capital flows into the asset class.

MORTGAGE-BACKED SECURITES

Agency MBS12 returned -0.26% but outperformed like-duration Treasuries by 2 bps, bringing year-to-date returns over Treasuries to 31 bps. Fifteen-year MBS outperformed 30-year MBS, and Ginnie Mae MBS outperformed conventional MBS. Within conventional MBS, higher coupons fared better than lower coupons, and the 4.5% was the best-performing liquid coupon. Prepayments have yet to slow materially, declining just 6%, but the average weekly refinancing index level fell 9%. Monthly issuance of agency MBS pass-throughs also declined 8%. Non-agency MBS continued to benefit from favorable market technicals and the gradual recovery in housing fundamentals, and prices and spreads were flat to modestly improved. Non-agency CMBS13 returned -0.83%, but outperformed like-duration Treasuries by 4 bps. Real estate prices continued to climb: The seasonally adjusted S&P/Case-Shiller 20 City Home Price Index was up 0.2% and the Moody’s/RCA Commercial Property Price Index rose 1.1% for the month of August (the most recent data).

MUNICIPAL BONDS

Municipals posted negative returns amid rising rates, increased supply and lower demand. States and municipalities rushed to issue a record $53 billion of debt before the upcoming elections and a potential Fed rate hike later this year. Weekly municipal mutual fund flows turned negative for the first time in over a year. As new money market fund regulations became effective 14 October, outflows continued from tax-exempt money market funds, and the SIFMA Municipal Swap Index spiked to 87 bps, the highest level since 2008. On the credit front, Puerto Rico continued its restructuring efforts as the governor presented the federal oversight board with a fiscal plan showing a 10-year cumulative financing gap of $59 billion absent any type of reform.

CURRENCIES

Persistent U.S. dollar strength dominated global currency performance during the month of October. The greenback posted gains across all G10 pairs, with the Japanese yen and the Scandinavian currencies the most notable laggards. The British pound experienced a brief but dramatic “flash crash” and was the weakest performer globally amid continued uncertainty surrounding Brexit. Among EM currencies, the Mexican peso ended the month stronger, but remained susceptible to political headlines from the U.S. election. The Chinese yuan was formally added to the IMF’s Special Drawing Rights (SDR) basket at the beginning of the month, but the offshore currency reached the weakest level on record as a stronger dollar gave China’s policymakers space to devalue the currency more assertively.

COMMODITIES

Commodity indexes posted flat to slightly negative returns in October. The more diversified Bloomberg index outperformed indexes with higher energy weightings (CSCB and GSCI) as that sector was down for the month. Crude oil prices were fairly strong early in the month, but lost ground as Libyan and Nigerian production edged higher and the U.S. rig count grew. In addition, Saudi crude oil exports were reported to hit their highs for the year, which was bearish for prices. Natural gas faced lack of demand due to warm weather. In agriculture, prices generally rose on supply concerns: Wheat was supported by weather stalling the Canadian harvest and expectations of fewer acres for the U.S. winter crop; corn gained on lower crop yield expectations; and soybeans rose on concern around South American planting and strong exports to China. Precious metals were down, with gold pressured by higher real yields, but notable gains in aluminum and zinc drove positive returns in industrial metals.

1MSCI World Index,

2S&P 500 Index,

3MSCI Europe Index (MSDEE15N INDEX),

4Nikkei 225 Index (NKY Index),

5MSCI Emerging Markets Index Daily Net TR,

6IBOVESPA Index (IBOV Index),

7Shanghai Composite Index (SHCOMP Index),

8S&P BSE SENSEX Index (SENSEX Index),

9MICEX Index (INDEXCF Index),

10Barclays Global Aggregate Credit USD Hedged Index,

11BofA Merrill Lynch Developed Markets High Yield Index, Constrained,

12Barclays Fixed Rate MBS Index (Total Return, Unhedged),

13Barclays Investment Grade Non-Agency MBS Index

PIMCO expects global growth to pick up slightly from around 2.5% this year to 2.5%‒3.0% in 2017, with inflation remaining below target in most major developed market economies. Our baseline forecast is for a continuous global expansion, mostly supportive monetary and fiscal policies and broadly range-bound markets. However, we are concerned about risks that lurk beneath the surface, especially with asset prices that in many cases appear stretched, and periods of relative calm in the markets are likely to be punctuated by bouts of volatility and uncertainty brought on by the “cause” of the moment. The most relevant swing factors for our cyclical outlook are productivity, which drives the supply side of the economy and thus potential output growth; policy, the main determinant of aggregate demand; and politics, the main non-economic source of uncertainty and volatility.

In the U.S., we see growth returning to 2%‒2.5% in 2017, following the soft patch earlier this year. We expect an end to the inventory correction and a revival of business investment amid robust consumer spending. A rise in headline CPI inflation to 2%‒2.5% next year will likely allow a data-dependent Federal Reserve to raise interest rates two or three times between now and year-end 2017.

For the eurozone, growth momentum should remain broadly unchanged at 1%‒1.5% in 2017, which is above potential output growth of at most 1%. Yet, with inflation unlikely to make much progress toward the European Central Bank’s (ECB) “below but close to 2%” objective, we expect a further round of monetary easing as soon as December, the potential for additional easing next year and a likely extension of quantitative easing beyond March. Our baseline calls for UK growth to slow temporarily into a 0%‒1% range next year as Brexit-related uncertainties damp investment and make consumers more cautious to spend.

In Japan, we expect somewhat higher growth of 0.5%‒1.0% in 2017, supported by significant fiscal stimulus. As fiscal policy turns expansionary, monetary policy may gain more traction, especially now that the Bank of Japan (BOJ) has recalibrated its easing program with a view to minimizing the negative side effects on the financial sector. Still, we expect the quest for 2% inflation to remain elusive in 2017.

Our base case for China is a further gradual slowdown in growth to 5.75%‒6.25% in 2017 from 6.4% this year. The hard landing in the industrial complex – which is what matters most for global trade and commodities – has already happened in recent years, and with an orderly depreciation in the currency, China is not likely to throw a wrench into the wheels of the global economy, though the consequences of credit-fueled stimulus bear watching.

Better prospects for the emerging markets (EM) are a key feature of our 2017 forecast. We expect aggregate GDP growth in EM to accelerate from about 4.5% this year to 4.75%‒5.25% next year. External conditions for many EM economies have improved due to the stabilization of commodity prices and the U.S. dollar. Internal conditions are also more conducive to growth: Inflation has likely peaked, giving central banks room to ease; several countries are making progress on structural reforms; and deep recessions in Brazil and Russia should give way to modest recoveries, removing a major drag on aggregate EM growth.

RENZI'S INFERNO

Like Britons last June, Italians face a consequential referendum in early December: Among the proposals is one to reform the constitution to abolish the Senate’s legislative power, leaving the lower house (Chamber of Deputies) as the key legislative body. Prime Minister Matteo Renzi’s pledge to resign if the reform fails has made the vote highly politicized, and the polls suggest it is too close to call.

A “yes” vote would likely be better for markets: It would clear a path for needed reforms, streamline the political system and ensure a clear winner in the next general election. Renzi would probably stay in power through the end of the legislative term in 2018, when he could face a close contest against Beppe Grillo’s anti-establishment Five Star Movement (M5S). A “no” vote could mean Renzi’s resignation, though not necessarily new elections being called ‒ the Senate would retain power and probably deliver a hung parliament. This muddle-through scenario would likely hurt Grillo’s chances of winning a future election, but would also damage Italy’s long-term growth prospects and potentially jeopardize recapitalization plans for Italian banks.