Rising concerns about the longevity of central bank accommodation briefly broke the tenuous calm in markets. The ECB’s inaction, the Fed’s indication of a potential rate increase later this year and the BOJ’s “comprehensive review” injected anxiety and volatility into relatively calm markets as investors grew concerned that seemingly perpetual central bank support may not be quite so permanent.

The fundamental backdrop continued to point to muted growth as central banks held the spotlight. Data in the U.S. were softer relative to expectations while business and consumption indicators in the U.K. and the eurozone continued to be positive.

Markets stumbled early in the month before recovering. Volatility rose in early September alongside rising yields amid investor concern about a change in the dovish stance of central banks. Yields came back down and risk assets recovered as the Fed once again lowered its estimate of the long-term neutral rate and the BOJ reaffirmed its commitment to easy policy.

In the world

BOJ THROWS A CURVE BALL A substantial flattening of Japan’s yield curve appears to have forced the BOJ to come to terms with the undesirable effects of negative interest rate policy (NIRP) and massive Japanese Government Bond purchases. In announcing changes to the BOJ’s framework in September, Governor Kuroda acknowledged the difficulties that financial intermediaries, insurance companies and pension funds have faced recently due to NIRP and the flatter curve. Going forward, the BOJ will seek “an appropriate yield curve” through enhanced flexibility of purchases and a 0% target for the 10-year rate. Furthermore, in an attempt to re-anchor inflation expectations, Kuroda committed to an overshoot of the BOJ’s 2% inflation objective. While the curve has steepened in September, inflation remains far from target, underscoring a major challenge ahead for the BOJ.

Central bank (in)action and rising concerns about the longevity of accommodative monetary policy briefly broke the tenuous calm that had characterized markets for much of the third quarter. The ECB kept its policy unchanged, but ECB President Draghi caused tension among investors by stating that the ECB had not discussed extending QE; days later, he also commented on the future role that fiscal policy could play in lifting growth and inflation. The Fed also voted to keep policy on hold, though three members dissented from the decision in a sign that a rate increase was possible soon. Market expectations for a rate hike before the end of the year rose as the Fed statement acknowledged that “the case for an increase in the funds rate has strengthened.” Combined, these events suggested a gradual shift away from the dovish stance of the last several months and fueled investor anxiety about seemingly perpetual support being not quite so permanent. The BOJ’s looming “comprehensive review” had also added to the trepidation, though its outcome reaffirmed the BOJ’s commitment to its policy goals and helped ease some investor concerns. Still, the BOJ’s latest twist in its decades-long fight against deflation shifted the framework toward yield curve control, with a stated target of 0% for the 10-year yield until inflation exceeds the 2% target. While such an arrangement isn’t completely new, it is a novel twist that could allow the BOJ to eventually move away from targeting a specific annual base-money increase and even tacitly taper its purchases.

While central bank action kept the market’s focus, economic fundamentals remained mostly tepid. Data in the U.S. skewed a bit more negative than in past months as job gains fell short of expectations and manufacturing slumped. Weak new orders and production, along with a drop in employment, sent the ISM manufacturing index into contractionary territory for the first time in six months. Europe, on the other hand, showed signs of modest resiliency, despite ECB inaction, as retail sales across the region provided evidence of a strengthening consumer base. Positive signs also emerged in the U.K., where a bounce in business sentiment suggested a strong rebound after the Brexit vote, even as lingering uncertainty about the timing and eventual form of the U.K.’s forthcoming exit from the trade union loomed large.

Markets stumbled early in the month before recovering. Market volatility rose early in the month following the ECB’s decision not to expand policy as anxiety grew over whether the Fed and BOJ would follow suit. In a move that evoked memories of the “taper tantrum” of 2013, global bond yields faced a sell-off as investors feared a swift rise in interest rates. Those fears, though, were ultimately short-lived as yields (and volatility) fell following the Fed and BOJ meetings. Despite the Fed being hawkish near term in signaling a move in December, a further reduction in the “blue dots” over the next few years conveyed an even more dovish tilt longer term. The BOJ’s “curve ball” ‒ and acknowledgment of the potential pitfalls of low long-term yields ‒ helped lift banking and insurance stocks in Japan, which had been under dual pressure from negative interest rates and the significant yield curve flattening that had transpired for much of the year. Most other risk assets recovered from the mid-month swoon to end largely unchanged. Also notable in the month was the 4% rise in oil prices following another highly anticipated OPEC meeting that resulted in a preliminary agreement to cut output, though many investors questioned its staying power. With continued low-rate policy and higher energy prices, most emerging markets gained.

In the markets

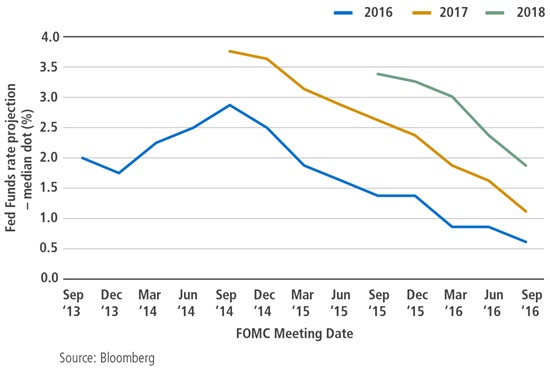

GOING DOWN (SWINGING) Despite mixed signals from Fed officials leading up to the September meeting, the FOMC ultimately left interest rates unchanged for the sixth straight time. The committee did, however, provide updated economic projections and the so-called dot plot, which signals the Fed’s outlook for the path of policy rates. As the chart shows, committee members once again collectively lowered their predictions for where the policy rate will be in the coming years. In fact, the Fed has consistently revised their forward guidance lower over the last several years, as it has reacted to slower-than-expected growth, tighter financial conditions and external shocks. This one-directional trend is likely a reason why market-implied expectations for policy rates remain well below those of the Fed’s own projections – it also suggests the Fed’s credibility may be at question.

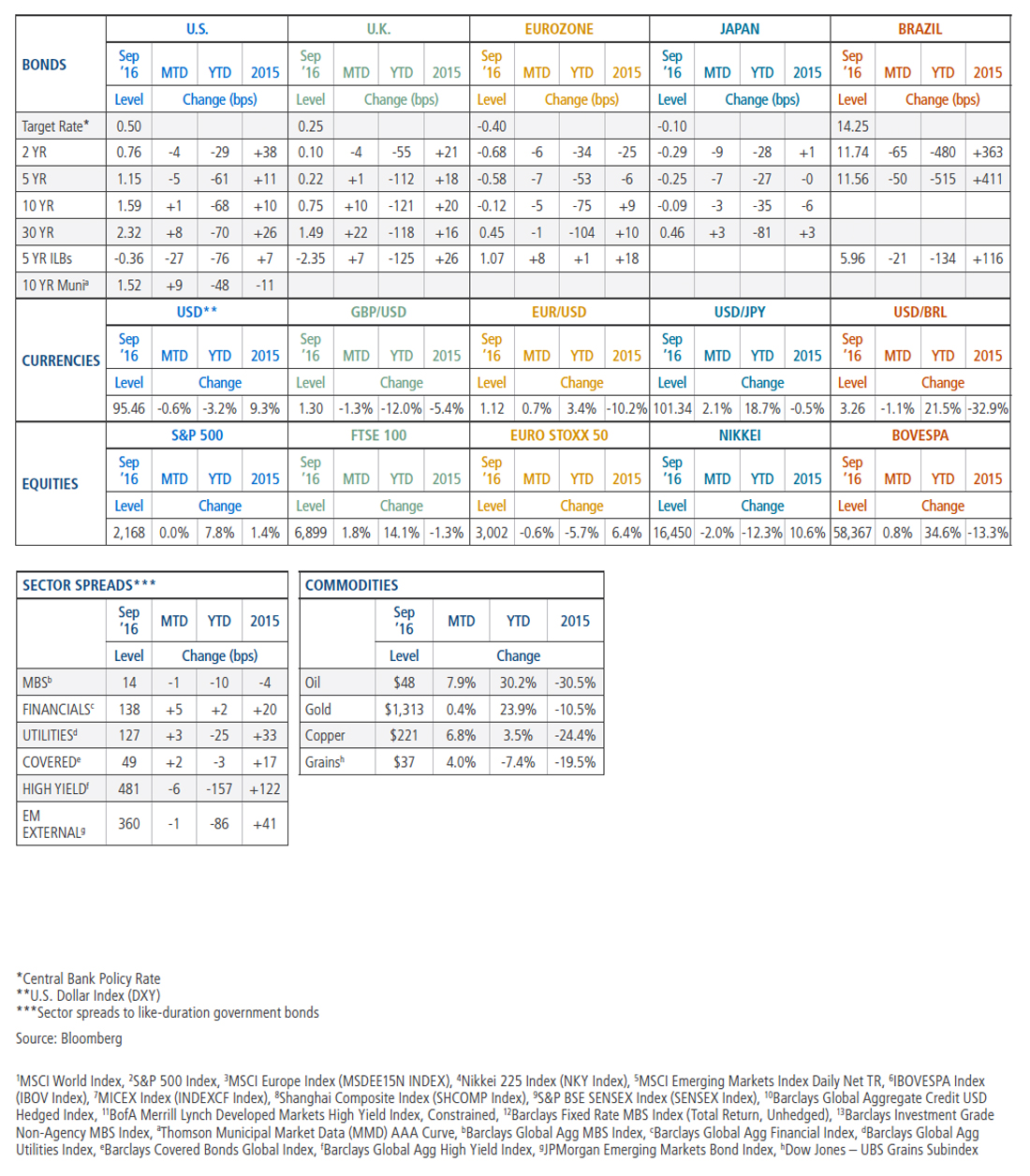

EQUITIES Developed market equities1 returned 0.5% during the month, as rising correlations between stocks and bonds made headlines. U.S. equities2 ended the month flat after early losses were recouped into month-end as central banks reaffirmed accommodative policies. European equities3 also ended the month flat as heightened volatility emanating from the financial sector weighed on returns. Japanese equities4 fell -2.0% amid a strengthening yen and shifts in the BOJ’s monetary policy framework.

In emerging markets5, improving external and internal conditions for many EM economies continued to drive risk-on sentiment, and equities rose 1.3%. Brazilian stocks6 extended their rally into their fourth consecutive month of gains, returning 0.8% amid higher commodity prices. The continued rebound in oil prices also benefitted Russian equities7, which advanced 0.5%. Chinese equities8 fell -2.5%, while Indian equities9 returned -2.0% after the military reported it had engaged militant camps in Pakistan.

DEVELOPED MARKET DEBT Developed market yields jumped higher early in the month after the ECB declined to expand its purchasing program, spurring investor anxiety that central banks might be pulling back from easy policy. Ten-year German bund yields rose nearly 20 bps to a high of -0.04% in the days following the announcement. However, after the Fed and the BOJ renewed their commitments to low-rate policy and continued easing, fears of a swift rise in global interest rates subsided, along with the brief global bond selloff. Over the month, developed market yield curves generally steepened as front-end rates moved lower on expectations for continued central bank accommodation. The spread differential between two-year and 10-year rates in the U.S. widened 6 bps, while two-year Japanese yields fell nearly 10 bps, and 30-year rates edged slightly higher.

INFLATION-LINKED DEBT Global inflation-linked bond (ILB) returns were mixed across countries, while talk of an oil production cut from OPEC late in the month helped lift inflation expectations across major markets. U.S. TIPS advanced for the month, outpacing nominal Treasuries, with the breakeven inflation rate (BEI) boosted by higher energy prices, a firmer CPI print in August and a slightly dovish tilt to the Fed’s statement. In the U.K., index-linked gilts continued to outperform nominal gilts by a significant margin. Breakeven levels were supported by continued weakness in the pound as well as strong demand from domestic investors. In Europe, core-country ILBs outpaced those from the periphery over the month after the ECB downplayed the negative impact of Brexit and left stimulus measures unchanged.

CREDIT Global investment grade credit spreads10 widened marginally in September, as risk-on sentiment abated somewhat due in part to idiosyncratic concerns and weakness in the banking sector late in the month. Nonetheless, strong demand from global investors for high quality, income-producing assets, continued to be generally supportive of credit spreads.

Risk appetite eased in early September only to resume mid-month, driving global high yield bond yields11 to 16-month lows amid easing global macro concerns, an improving backdrop for commodities and accommodative central banks. Total returns for global high yield bonds were positive for the eighth consecutive month, up 0.4% for September and 13.6% year-to-date.

EMERGING MARKET Emerging market (EM) debt assets posted positive returns as commodity prices rallied, the Fed remained on hold, and improving fundamentals drove another strong month of inflows into the asset class. Spreads over U.S. Treasuries for external debt narrowed, EM local bond yields fell and currencies strengthened against the U.S. dollar. Stronger exports helped narrow the current account deficit in South Africa, where external and local currency debt both outperformed and the currency rallied on continued capital inflows. Inflation dynamics continued to moderate in Asia and Latin America, as central banks in Indonesia and Brazil left rates on hold while indicating a dovish tilt. Following OPEC’s surprise announcement of potential production cuts, oil prices rallied and lifted the returns of exporters like Venezuela, Colombia and Russia.

MORTGAGE-BACKED SECURITIES Agency MBS12 returned 0.28% and outperformed like-duration Treasuries by 19 bps, bringing year-to-date excess returns to 30 bps. Fifteen-year MBS outperformed 30-year MBS, while Ginnie Mae MBS underperformed conventional MBS amid heavy new supply. Within conventional MBS, higher coupon outperformed lower coupon securities. Strong investor demand has benefited agency MBS, and going forward, refinancing and new supply pressure should ease. Non-agency MBS prices increased, and spreads tightened amid continued favorable market technicals and stable residential real estate fundamentals; home prices were up 5.1% year-over-year in July (the most recent data available). Non-agency commercial MBS13 returned -0.50% and underperformed like-duration Treasuries by 65 bps, though fundamentals remained stable, with commercial property values up 7.7% year-over-year in July.

MUNICIPAL BONDS Persistent demand was not sufficient to keep pace with heightened supply, and municipal bonds posted negative returns during the month, underperforming Treasuries. Primary market supply of $38.3 billion was a record for the month of September, with year-over-year gains in both refunding and new issuance. Supply pressures were only somewhat offset by continued positive retail demand. Municipal mutual funds recorded a 52nd consecutive week of net inflows, although outflows from U.S. tax-efficient money market funds pressured short-term yields. Puerto Rico’s rolling defaults continued, and restructuring efforts moved forward as the federal control board awaited the first Territorial Fiscal Plan from the island’s current administration.

CURRENCIES The U.S. dollar was generally weaker in September as the Fed kept rates unchanged, maintaining a more dovish monetary policy stance. The ECB also kept rates on hold, while the BOJ introduced a new monetary framework targeting the yield curve. In the wake of these moves, the Japanese yen and euro both strengthened. Other G10 central banks also kept rates unchanged during the month, providing support for the currencies of Australia, New Zealand and Scandinavia. The British pound was weaker as EU officials made it clear that the U.K. could not cherry-pick the benefits of the single market in Brexit negotiations. In emerging markets, political uncertainty in the U.S. weighed on the Mexican peso, while stronger exports and capital inflows strengthened the South African rand.

COMMODITIES Commodities posted a broad-based rally for the month. Crude oil prices found some support in Department of Energy data that showed meaningful inventory draws early in the month. OPEC’s announcement of a potential agreement to curtail production also created a bullish sentiment for oil. However, the burden of proof is on OPEC – many implementation questions remain unanswered. In the natural gas market, warm weather, which drove cooling demand all summer, delayed the start of the winter heating season, and hurt prices toward month-end. In agriculture, sugar was the top performer as the market is expecting a shortfall next year, in part affirmed by UNICA (the Brazilian Sugarcane Industry Association) cutting yield estimates. Prices for corn, wheat and soybeans were also up, recouping a small share of their late summer losses; strong demand supported the complex and offset some of the anticipated excess supply in new crop estimates. Base metals posted strong returns, supported by better-than-expected data out of China. Prices for precious metals were also higher, led by silver, which was largely a technical move.

Outlook

PIMCO expects global growth to pick up slightly from around 2.5% this year to 2.5%‒3.0% in 2017, with inflation remaining below target in most major developed market economies. Our baseline forecast is for a continuous global expansion, mostly supportive monetary and fiscal policies and broadly range-bound markets. However, we are concerned about risks that lurk beneath the surface, especially with asset prices that in many cases appear stretched, and periods of relative calm in the markets are likely to be punctuated by bouts of volatility and uncertainty brought on by the “cause” of the moment. The most relevant swing factors for our cyclical outlook are productivity, which drives the supply side of the economy and thus potential output growth; policy, the main determinant of aggregate demand; and politics, the main noneconomic source of uncertainty and volatility.

In the U.S., we see growth returning to 2%‒2.5% in 2017, following the soft patch earlier this year. We expect an end to the inventory correction and a revival of business investment amid robust consumer spending. A rise in headline CPI inflation to 2%‒2.5% next year will likely allow a data-dependent Federal Reserve to raise interest rates two or three times between now and year-end 2017.

For the eurozone, growth momentum should remain broadly unchanged at 1%‒1.5% in 2017, which is above potential output growth of at most 1%. Yet, with inflation unlikely to make much progress toward the European Central Bank’s (ECB) “below but close to 2%” objective, we expect a further round of monetary easing as soon as December, the potential for additional easing next year and a likely extension of quantitative easing beyond March. Our baseline calls for UK growth to slow temporarily into a 0%‒1% range next year as Brexit-related uncertainties damp investment and make consumers more cautious to spend.

In Japan, we expect somewhat higher growth of 0.5%‒1.0% in 2017, supported by significant fiscal stimulus. As fiscal policy turns expansionary, monetary policy may gain more traction, especially now that the Bank of Japan (BOJ) has recalibrated its easing program with a view to minimizing the negative side effects on the financial sector. Still, we expect the quest for 2% inflation to remain elusive in 2017.

Our base case for China is a further gradual slowdown in growth to 5.75%‒6.25% in 2017 from 6.4% this year. The hard landing in the industrial complex – which is what matters most for global trade and commodities – has already happened in recent years, and with an orderly depreciation in the currency, China is not likely to throw a wrench into the wheels of the global economy.

Better prospects for the emerging markets (EM) are a key feature of our 2017 forecast. We expect aggregate GDP growth in EM to accelerate from about 4.5% this year to 4.75%‒5.25% next year. External conditions for many EM economies have improved due to the stabilization of commodity prices and the U.S. dollar. Internal conditions are also more conducive to growth: Inflation has likely peaked, giving central banks room to ease; several countries are making progress on structural reforms; and deep recessions in Brazil and Russia should give way to modest recoveries, removing a major drag on aggregate EM growth.

In Sight

QUE ONDA, PESO?

Mexico’s peso has been one of the worst performing currencies globally this year despite the country’s generally sound monetary and fiscal frameworks, ample liquidity and high real yields. Recent market headlines have linked heightened volatility in the currency to rising uncertainty in the U.S. presidential election, but that may not tell the full story. So what’s up with the peso? A closer inspection of the underlying economic fundamentals reveals more than just political noise weighing on the currency. Mexico’s current account deficit has deteriorated as declines in oil prices and production have hurt the country’s largest export sector. While higher growth in the U.S. has helped boost remittances from locals working abroad, these and other portfolio flows are a more volatile source of deficit financing and therefore lend little added support to the peso. However, there are tentative signs that the weaker currency is starting to narrow the trade balance as total exports have perked up. The central bank also recently hiked interest rates in an effort to arrest the peso decline, prevent a spike in inflation and anchor inflation expectations. A cheap currency is not always sufficient to attract capital inflows, but the fundamental catalysts for a turnaround are beginning to emerge.

Appendix

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk and liquidity risk. The value of most bonds and bond strategies is impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign denominatedand/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax; a strategy concentrating in a single or limited number of states is subject to greater risk of adverse economic conditions and regulatory changes. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation- Protected Securities (TIPS) are ILBs issued by the U.S. government. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.